ASML Holding NV (ASML), the Dutch monopoly supplier of EUV lithography systems used to make the most advanced computer chips, reports Q2 2026 results on 15 July, before the market open. Management has raised guidance twice this year, first-quarter results beat the company’s own targets, and consensus expects earnings per share up more than 75% year over year. An unresolved US-China export-control dispute has already moved the stock more than 7% in a single session. (Source: Saxo, Bloomberg.)

The stock has moved more than 7% on the earnings day itself in six of the last eight quarters. (Source: Saxo, Bloomberg, CBOE.) That history keeps implied volatility persistently rich into this kind of print, and it’s why the obvious options trade is often the wrong one. The three views below walk through that reasoning for a bullish, a bearish, and a direction-neutral read.

ASML weekly and daily charts, Euronext Amsterdam listing (EUR). Source: SaxoTrader. Levels shown will differ by the 15 July earnings date and at the time of reading.

ASML weekly and daily charts, Euronext Amsterdam listing (EUR). Source: SaxoTrader. Levels shown will differ by the 15 July earnings date and at the time of reading.

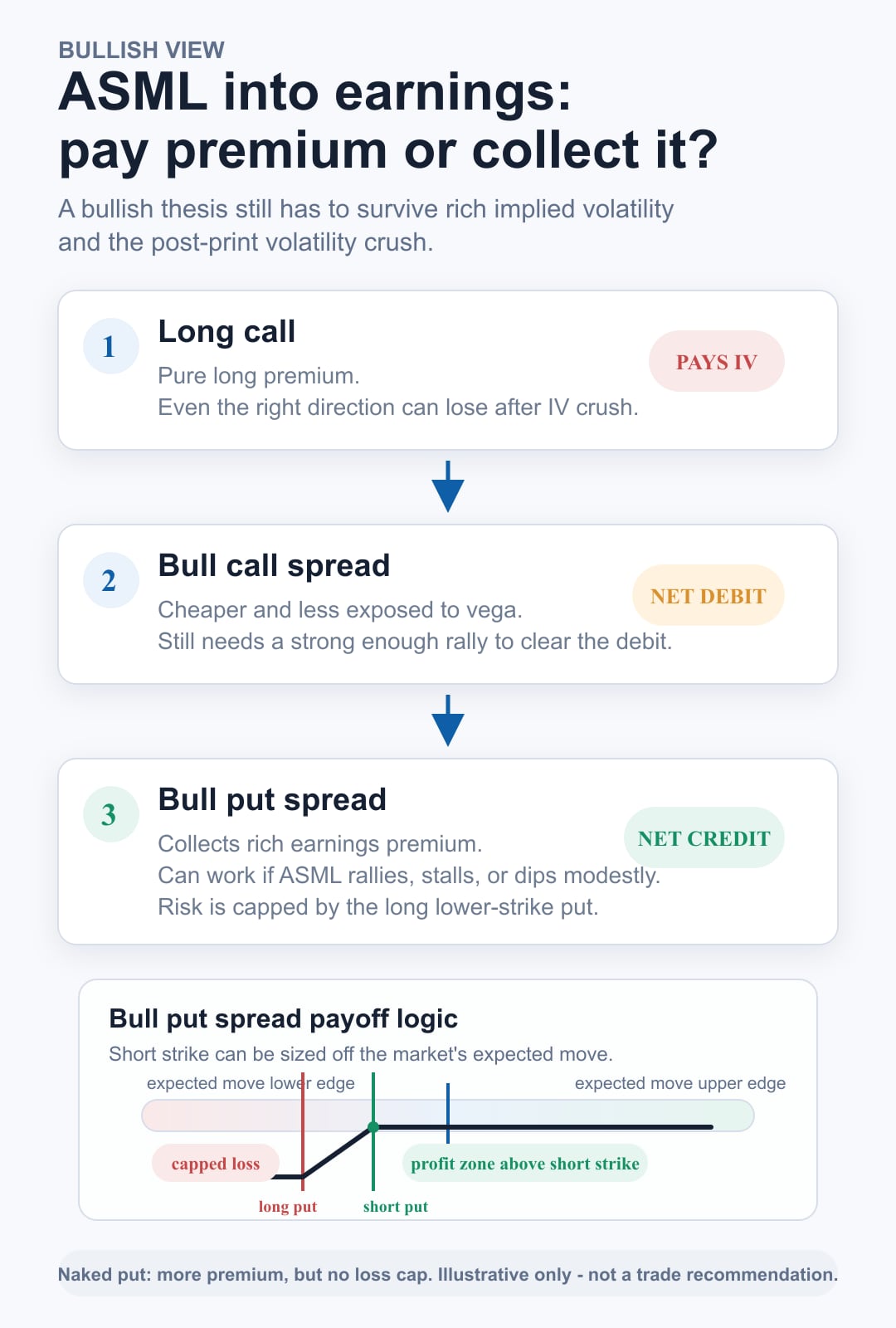

Bullish view

Say a trader expects ASML to shrug off the export-control overhang and rally into the print, on the back of guidance raised twice this year.

The obvious idea is buying a call outright. That’s where the reasoning usually breaks down. Options on a stock with ASML’s earnings history carry rich implied volatility ahead of the print, volatility that typically collapses once the uncertainty resolves. A long call is pure long premium: even getting the direction right can still lose money if the rally falls short of what was already priced in.

The next instinct is a bull call spread, buying a call and selling a further one against it. That’s better and cheaper, with less vega exposure, but it’s still a net debit, still needing the stock to rally far enough to clear the cost and the crush at once.

The reverse of that is a bull put spread: selling an out-of-the-money put and buying a further one to cap the risk. This collects the rich premium instead of paying it, and profits if ASML rallies, sits still, or slips modestly, as long as it holds above the short strike. Maximum loss: the width between the strikes minus the credit collected, larger in dollar terms than the debit spread above would have cost. Illustrative only, not a trade recommendation.

Running that put naked instead would collect even more premium, but removes the loss cap entirely, see the checklist below for why that trade-off matters.

One execution wrinkle worth knowing: the short strike is often sized off the market’s own priced expected move, from the at-the-money straddle, rather than an arbitrary distance. Implied volatility also tends to climb into the print, so an entry too many days ahead leaves a short-vega position exposed before the event happens, which is why entries closer to the print are generally considered better timed.

The bullish walkthrough in one map: from long call, to bull call spread, to the bull put spread. Illustrative only, not a trade recommendation. Source: ©Saxo

The bullish walkthrough in one map: from long call, to bull call spread, to the bull put spread. Illustrative only, not a trade recommendation. Source: ©Saxo

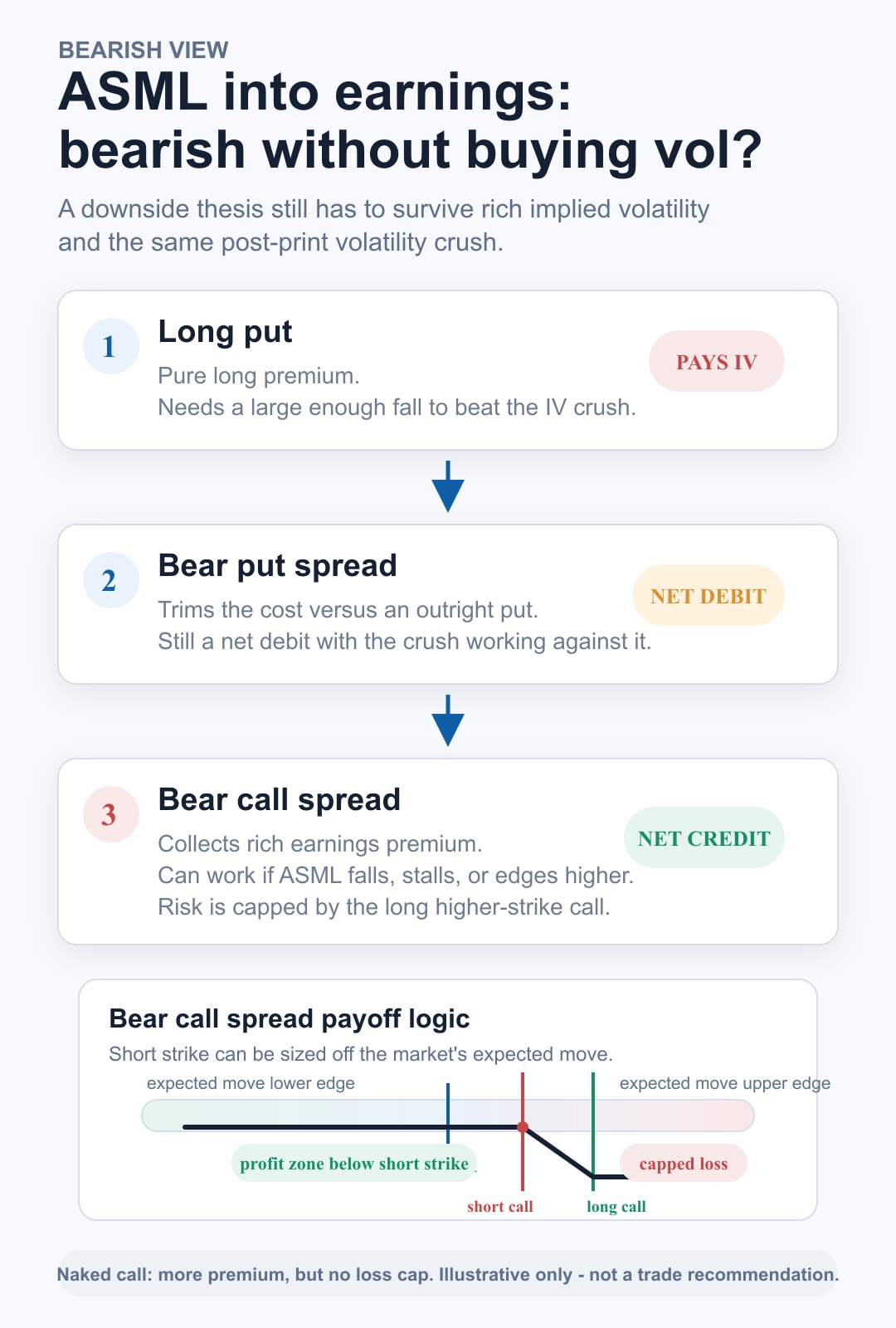

Bearish view

Now the mirror case: the dispute escalates, or guidance disappoints against an already-raised bar.

Buying a put outright has the same problem as buying a call: pure long premium, fighting the same crush, needing a big enough move to work. A bear put spread trims the cost but is still a net debit with the same crush working against both legs.

The reverse is a bear call spread: selling an out-of-the-money call and buying a further one to define the risk. It collects premium instead of paying it, and profits if ASML falls, sits still, or even edges higher, as long as it stays below the short strike. Maximum loss: the width between the strikes minus the credit collected, taken in full if the stock rallies through the higher strike. Illustrative only, not a trade recommendation.

The same trade-off applies here: selling that call naked collects more premium but drops the cap, see the checklist below.

The same execution logic from the bullish view applies in reverse: the short strike is typically sized off the market’s implied move, with entries favoured closer to the print rather than days ahead.

The bearish walkthrough in one map: from long put, to bear put spread, to the bear call spread. Illustrative only, not a trade recommendation.

The bearish walkthrough in one map: from long put, to bear put spread, to the bear call spread. Illustrative only, not a trade recommendation. Source: ©Saxo

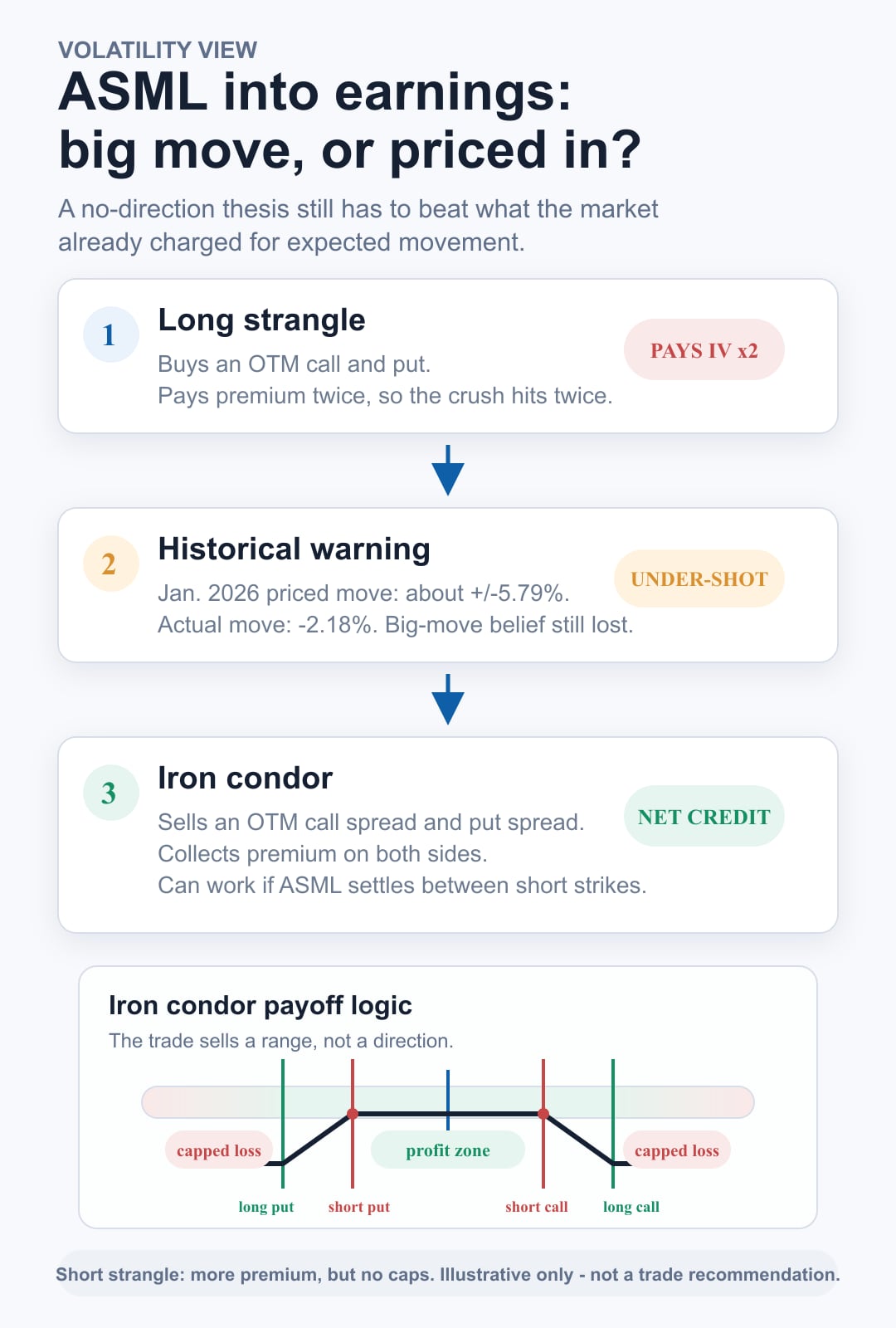

Volatility view

No strong direction, but a trader trusts ASML’s own history of double-digit earnings swings to produce a big move either way. The obvious idea is a long strangle: an out-of-the-money call and put together, betting on size rather than direction.

Same problem here, doubled: buying both sides means paying premium twice, so the crush hits twice. History provides the cautionary tale directly: ahead of the January 2026 report, options priced a move of roughly plus or minus 5.79%, and the stock only moved minus 2.18%. (Source: Saxo, Bloomberg) A trader who correctly believed “this could move a lot” still would have lost money, because the actual move undershot what was already priced.

The reverse is an iron condor: selling an out-of-the-money call spread and an out-of-the-money put spread around the current price. This collects premium on both sides and profits if the stock settles anywhere between the short strikes, benefiting from the same crush that punished the strangle. Maximum loss: the width of either spread minus the total credit collected, taken in full if the stock closes beyond the short strikes on either side. Illustrative only, not a trade recommendation.

Running either side of this naked, as a short strangle, collects more premium on both sides but drops the cap on both, see the checklist below.

One further refinement: rather than holding the condor through the announcement, some traders wait for the first session after the release to open it. By then the number is public and the stock has made its initial move, so the announcement’s delta uncertainty is gone, while much of the volatility crush typically still lies ahead. The trade-off: implied volatility can also collapse fast once the print is out, so the premium still available isn’t guaranteed.

Even with better timing, the strikes would still need to be wide enough. ASML has posted moves beyond minus 16% and minus 12% in past prints. A condor built for a “normal” stock, with short strikes close to the money, is exposed to exactly the kind of outlier ASML has delivered before.

The volatility walkthrough in one map: from long strangle, to iron condor, with the post-earnings entry refinement noted. Illustrative only, not a trade recommendation. Source: ©Saxo

Before placing any of these structures, check:

- Every credit structure above could be run without its long leg, as a naked short put, short call, or short strangle, for more premium collected up front. That would remove the very thing that caps the loss, not the volatility view. At a share price above €1,600, one uncovered short put obligates the seller to buy 100 shares at the strike if assigned, a notional exposure well over €150,000 per contract, with margin required to match. The long leg exists specifically to avoid carrying that exposure.

- ASML options are American-style; every structure above has at least one short leg, which carries early assignment risk.

- The actual strikes, expiry, and entry timing come from the live option chain and expected move on the day, not from anything in this article.

Final thought

Looking across all three views, a pattern emerges: buying premium outright is usually the weakest structure, and the credit version usually captures the edge, provided strikes, timing, and the long leg are never sacrificed for a bigger premium. The actual strikes come from the option chain and expected move visible on the day, not from anything here.

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results. The Author is permitted to wait at least 24 hours from the time of the publication before they trade the instruments themselves. The author does not hold positions in any of the instruments mentioned in this article at the time of publication.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with a view to providing clients with valuable information and insights.

This is marketing material and cannot be considered as investment research. This material has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.