ASML earnings: how to think about the setup before the numbers

ASML reports on 15 April – and the real question is not just direction, but whether the actual move will be larger or smaller than what options are already pricing.

ASML is scheduled to report earnings on 15 April. As one of the most important companies in the semiconductor ecosystem, its results often influence not only the stock itself but also broader sentiment in the sector. Importantly, the reaction is rarely driven by the headline numbers alone. Guidance, order intake, and management commentary typically determine how investors reassess the outlook.

ASML remains in a strong longer-term uptrend, with recent price action consolidating near highs ahead of the earnings release. Source: SaxoTrader

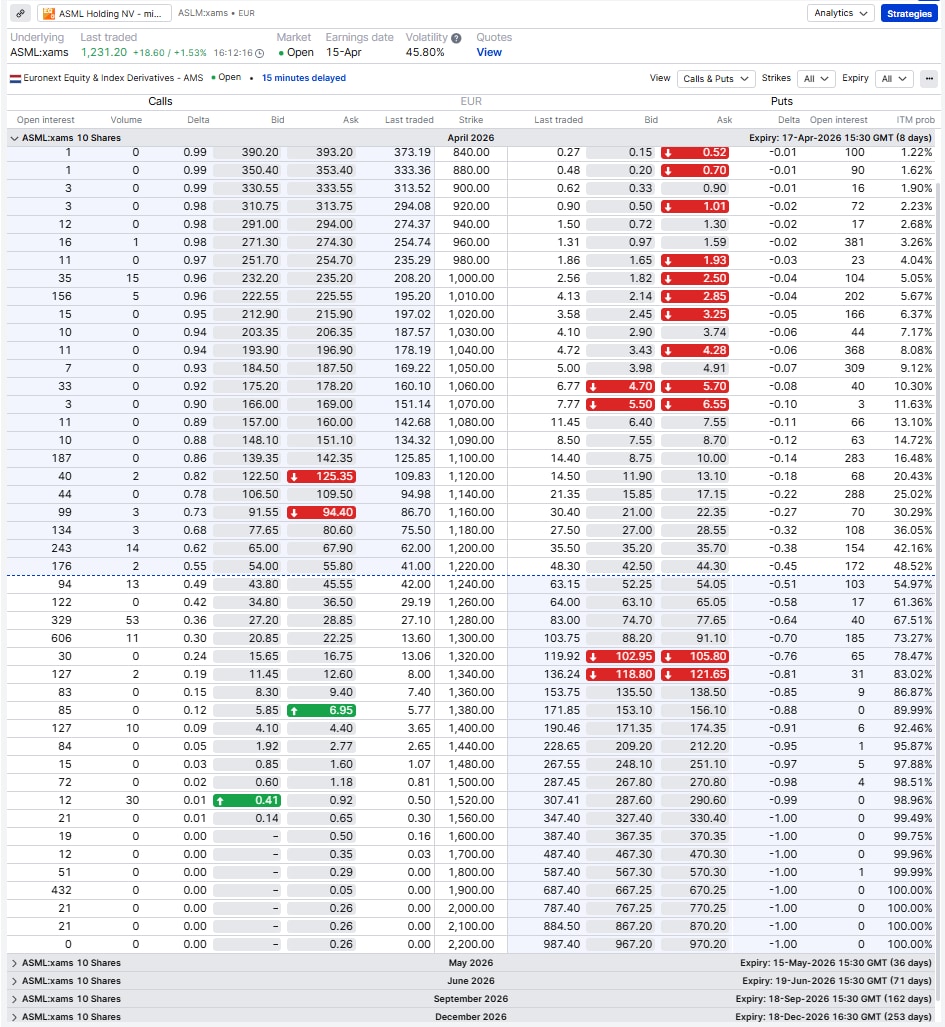

What options are pricing ahead of earnings

Options markets allow us to estimate the size of the move investors are expecting. A common and simple approach is to look at the at-the-money (ATM) call and put prices for the expiry right after earnings, and add them together.

- The call price reflects the market’s expectation of upside risk

- The put price reflects downside risk

- Adding both gives a rough estimate of the total expected move in either direction

From the 17 April expiry:

- ATM call ≈ 43

- ATM put ≈ 44

- Expected move ≈ 87–97 points (~8%)

With ASML trading around 1,220–1,230, this implies a rough range of ~1,130 on the downside to ~1,320 on the upside.

This expected move is not a forecast. It is the market’s pricing of uncertainty.

Options expiring just after earnings show elevated premiums, with the at-the-money call and put implying a move of roughly ±90–100 points. Source: SaxoTrader

Important context: mini-options

The examples below use mini-options, where one contract represents 10 shares instead of the standard 100.

This means:

- A price of 28.0 equals EUR 280 per contract

- All profit and loss figures are expressed per contract

This reduces the absolute capital required, but it is important to be clear: the risk is not smaller in relative terms. The payoff profile is identical to standard options, just scaled down. In other words, mini-options improve accessibility, not risk.

Thinking in scenarios, not predictions

Before looking at strategies, it helps to frame the possible outcomes.

- A strong report and constructive outlook may push the stock higher.

- A decent report with limited surprises may result in a smaller move.

- A weaker outlook may trigger a downside reaction.

The strategies below are not recommendations. They are examples of how different option structures align with different views before the earnings event.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it's crucial to make informed decisions.

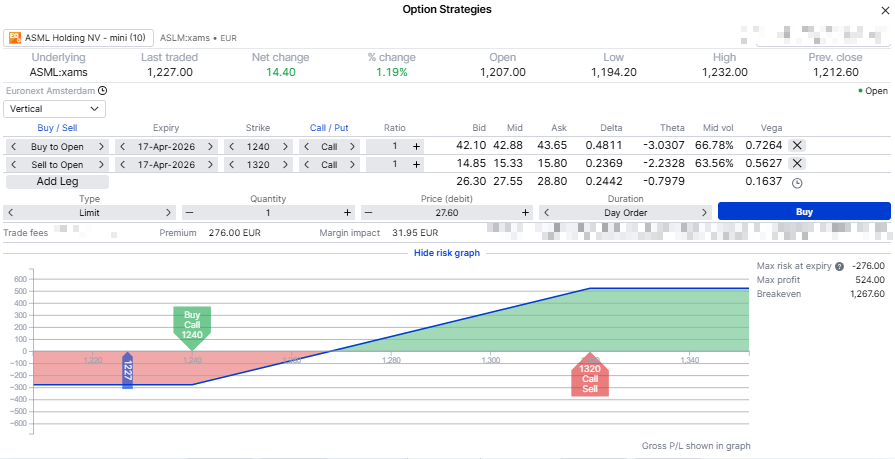

Bullish view: call spread (1240/1320)

A call spread combines buying a call option and selling another at a higher strike.

A bull call spread provides defined-risk upside exposure, with lower cost but capped profit above the short strike. Source: SaxoTrader

- Buy 1240 call / Sell 1320 call

- Entry cost: ~28 points ≈ EUR 280

- Maximum loss: EUR 280

- Maximum profit: ~EUR 520

- Break-even: ~1268

How it works

The long call gains value if the stock rises. The short call offsets part of the cost, but caps the upside. This means you need the stock to move above the break-even level to profit.

Why use it here

It expresses a bullish view, but acknowledges that the move still needs to be meaningful relative to what is priced in.

Key risk

You can be right on direction, but still lose money if the move is too small.

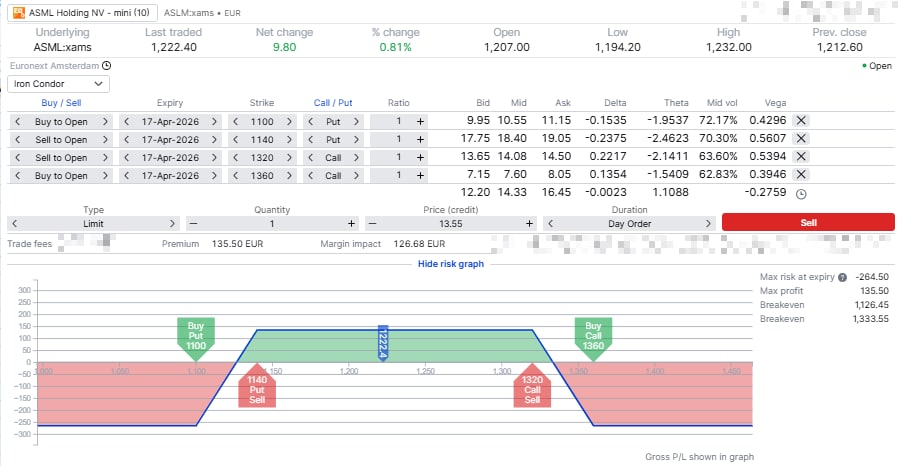

Neutral view: iron condor (1100/1140/1320/1360)

An iron condor combines two credit spreads: a put spread below the market and a call spread above the market.

An iron condor benefits if the post-earnings move stays within a defined range, capturing premium if the move is smaller than expected. Source: SaxoTrader

- Sell 1140 put / Buy 1100 put

- Sell 1320 call / Buy 1360 call

- Entry credit: ~13.5 points ≈ EUR 135 received

- Maximum loss: ~EUR 265

- Break-even range: ~1126 to ~1334

How it works

You receive a premium upfront by selling options. These options lose value over time, especially after earnings when volatility drops. If the stock stays within a defined range, the options expire worthless and you keep the premium.

Why this links to the expected move

The strikes are placed around the implied range (~1,130–1,320). If the actual move is smaller than expected, the trade benefits. If the move is larger, the position starts to lose money.

Key risk

This strategy expresses a view that the market may have overestimated the size of the move.

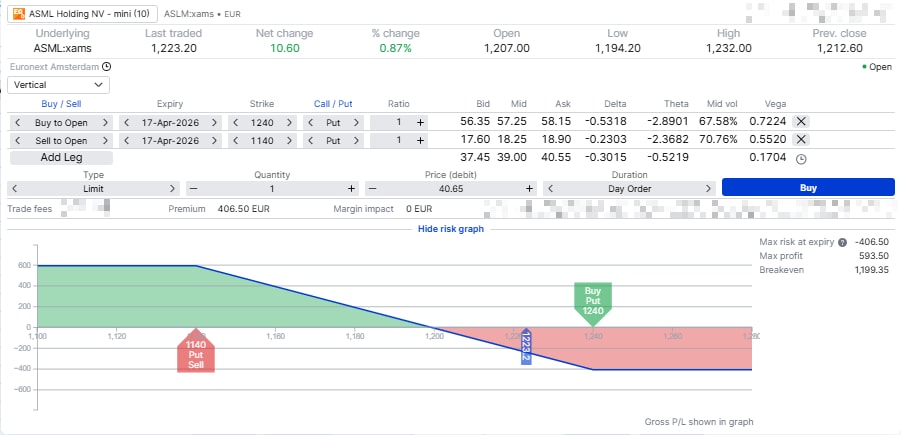

Bearish view: put spread (1240/1140)

A put spread combines buying a put and selling another at a lower strike.

A bear put spread offers defined-risk downside exposure, requiring a sufficient decline to offset the premium paid. Source: SaxoTrader

- Buy 1240 put / Sell 1140 put

- Entry cost: ~40 points ≈ EUR 400

- Maximum loss: ~EUR 400

- Maximum profit: ~EUR 600

- Break-even: ~1200

How it works

The long put gains value if the stock falls. The short put reduces the cost, but caps the downside payoff. The trade becomes profitable if the stock moves below the break-even level.

Why use it here

It expresses a bearish view while keeping risk defined in advance.

Key risk

As with the bullish case, the move needs to be large enough to offset the premium paid.

Managing the position after earnings

Earnings trades do not end when the numbers are released – in many cases, that is when the real decision-making begins. Once the earnings are released, the focus shifts from entering the trade to managing it.

A few practical considerations:

- Act early if the move happens quickly: if the stock makes a strong move in your favour shortly after the release, it can make sense to take profits rather than wait for expiry.

- Be cautious with reversals: earnings reactions can reverse within hours or days, especially after an initial overreaction.

- Volatility drops quickly: option premiums often fall sharply after earnings, which can impact positions even if the direction is correct.

- Have a clear exit plan: decide in advance whether you will hold to expiry or close earlier based on price levels or profit targets.

- Consider taking profits early: a common approach is to take profits around 50% of the maximum potential gain (for both credit and debit structures), rather than waiting for full payoff.

Managing the position is just as important as selecting the right structure.

Why earnings trades can be tricky

Earnings trades often disappoint even when the directional view is correct. This is because options pricing reflects:

- The expected size of the move

- The timing of the move

- The level of uncertainty (volatility)

After earnings:

- The move may be smaller than expected

- Implied volatility typically falls

- Time decay accelerates

As a result, direction alone is not enough.

A simple checklist before placing a trade

Before entering an earnings trade, it can help to ask:

- What move is priced in? Options are implying roughly ±100 points – do you expect a bigger or smaller move?

- Is your view aligned with the structure? For example, are you expecting a strong move (spreads) or a contained move (condor)?

- Does the expiry match your time horizon? These examples use short-dated options right after earnings – if your view is longer-term, this may not be the right expiry.

- What is the maximum loss in EUR? Can you accept losing the full premium paid or risk defined in the structure?

- Is your position size appropriate? Keep the exposure small relative to your overall portfolio – earnings moves can be sharp and unpredictable.

- What is your exit plan? Will you take profits early (e.g. around 50%) or hold to expiry?

Conclusion

ASML earnings are not just about predicting direction. A more robust approach is to define scenarios, understand what the market already expects, and then choose a structure that reflects that view while keeping risk clearly defined.

Around earnings, magnitude and timing often matter more than direction alone.

FAQ

Why use the ATM call + put to estimate the move?

It’s a quick proxy for the straddle price. The call reflects upside risk, the put downside risk. Together they approximate the market-implied move around the event. It’s not a forecast, but a pricing benchmark.

How does IV crush affect these strategies differently?

- Call/put spreads (debit): IV crush hurts the long option, but the short leg offsets part of that effect. You still need a sufficient move.

- Iron condor (credit): IV crush helps, as both short options lose value. The risk is a large move overwhelming that benefit.

How should I choose strikes relative to the expected move?

- Directional (spreads): place break-even inside the implied move so you don’t need an extreme outcome.

- Range (condor): place short strikes around/just outside the implied range to express “move smaller than priced.”

Why include a short (sold) leg in spreads?

Selling a second option serves two purposes: it reduces the entry cost (debit) or increases the credit received, and it defines and limits risk, as the long leg offsets extreme outcomes. The trade-off is that maximum profit is capped at the short strike.

Should I hold to expiry or close early?

Around earnings, many traders prefer to close early if the move happens quickly (e.g., targeting ~50% of max gain). Holding to expiry increases exposure to reversals and decay.

What about assignment risk?

With short options (e.g., condor legs), there is assignment risk, especially if options go in-the-money near expiry. Keep an eye on positions and liquidity. (Mechanics depend on the exchange and contract specifications.)

Why do bid/ask spreads matter so much here?

Short-dated earnings options can have wide spreads. Your actual fill (not the midpoint) can materially change P/L. Use limit orders and be realistic about execution.