Key points:

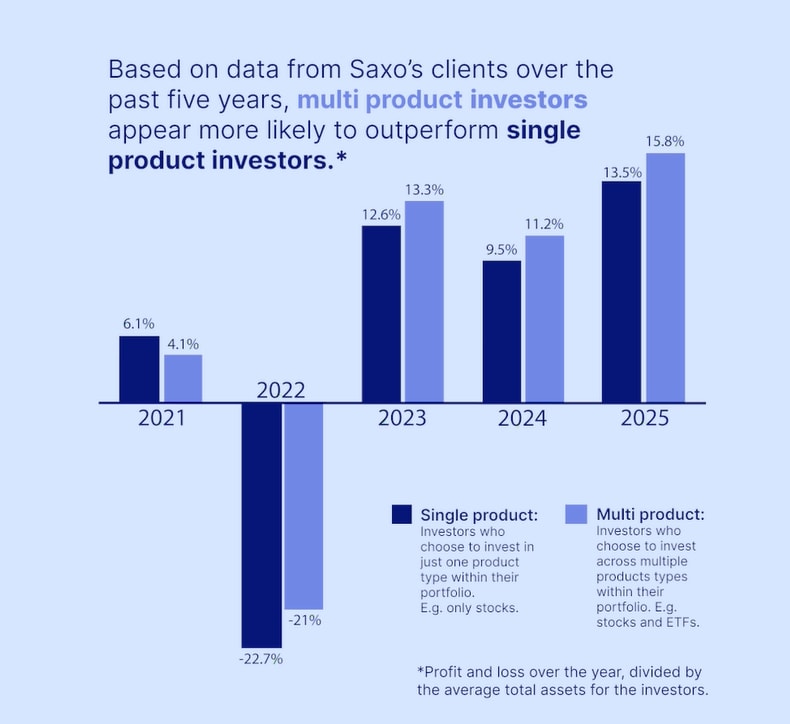

- Over the last five years, Saxo’s client data shows investors who used more than one product type have tended to be more profitable than those using only one.

- A broader toolkit may help by reducing hidden concentration, improving decision-making in drawdowns, and providing more than one way for a portfolio to perform across market regimes.

- Getting started doesn’t require a portfolio overhaul. One small step beyond stocks (ETF, bonds, commodities, or simple collateralised options) can be a practical first move.

An interesting insight

Markets don’t reward the same exposures every quarter. Multi-asset investing is less about chasing returns and more about building a portfolio that can behave through different regimes, especially when drawdowns test decision-making.

Looking at aggregated Saxo client activity over the past five years, clients who used more than one product type were more likely to have higher profitability outcomes than clients who only used one (for example, stocks only).

Note: Past performance is not indicative of future results.

Source: Saxo client data

This is an association, not proof that using multiple products causes better results. Clients who use more instruments may differ in experience, risk management, time horizon, trading frequency, and costs—each of which can influence outcomes.

The practical takeaway is simpler: having more than one tool can give investors more ways to respond to changing market regimes—and may reduce the odds that one “single story” dominates results.

Why this may be happening

1) A smoother ride can improve behaviour

When outcomes are less dominated by one market move, investors are often less likely to panic-sell, overreact, or abandon a plan after a drawdown.

2) Different environments reward different exposures

Stocks don’t lead every quarter. Adding other building blocks (like bonds or commodities) can help when leadership rotates.

3) Less hidden concentration

“Stocks-only” portfolios often drift into concentrated bets (a few mega-caps, one sector, one region). Adding another product type can reduce single-story risk.

4) More consistent habits

ETFs and recurring contributions can encourage steadier investing behaviour. These are often more important than perfect timing.

Myths that keep investors stuck

Myth 1: “Diversification means lower returns.”

Diversification can reduce extremes, both on the highs and lows. For many investors, the bigger benefit is avoiding deep drawdowns and the bad timing decisions they often trigger.

Myth 2: “ETFs are just beginner products.”

ETFs are simply a wrapper. They can express broad markets, quality, dividends, sectors, regions, or themes – all without relying on single-stock outcomes.

Myth 3: “Bonds don’t matter anymore.”

Bonds are less about excitement and more about ballast. They may help cushion equity volatility and provide liquidity when markets are stressed.

Myth 4: “Commodities are only for traders.”

Commodities can be volatile, but they can also diversify portfolios in certain regimes (inflation surprises, supply shocks) when stocks and bonds become correlated.

Myth 5: “Options are leverage.”

Some options strategies are highly leveraged. But collateralised strategies like covered calls and cash-secured puts are often used by long-term investors as portfolio tools (still risky, but not the same as naked options).

If you’re stocks-only: common starting points investors consider

A broader toolkit doesn’t have to mean a full rebuild. The examples below are educational illustrations of how investors sometimes introduce a second return driver or a shock absorber. They’re not investment advice and may not be suitable for everyone.

1) ETFs (spreading single-name risk)

What it does: ETFs can reduce reliance on a handful of stocks by spreading exposure across more companies, sectors, or regions—while still keeping equity exposure.

Simple ways to start (illustrative):

- Broad-market exposure to reduce single-stock concentration

- Quality/dividend tilts to change the risk profile (with different sector/factor exposures)

Reality check: ETFs still carry market risk and can fall materially in a broad selloff.

2) Bonds (potential shock absorber / liquidity sleeve)

What it does: Bonds are often used as ballast and liquidity—particularly when equity volatility rises.

Simple ways to start (illustrative):

- Higher-quality bonds as ballast

- Shorter-duration exposure to reduce rate sensitivity (still not “risk-free”)

Reality check: Bonds can lose money (especially longer duration) and may not hedge equities in every regime.

3) Commodities (real assets for diversification in some regimes)

What it does: Commodities can diversify portfolios in certain macro environments, such as inflation surprises or supply shocks.

Simple ways to start (illustrative):

- Broad commodities exposure for diversification

- A modest allocation to precious metals as a stress diversifier in some regimes

Reality check: Commodities can be highly volatile and may not provide protection when you most want it.

4) Equity Trading Options (ETO) in collateralised structures

Some investors use collateralised option structures to introduce rules—often around income discipline or entry discipline. These strategies still carry meaningful risk and are not suitable for all investors.

Two examples (for information only):

A) Covered call (income-focused)

- What it is: you own the shares and sell a call option against them.

- Why investors use it: to earn option premium; trade-off is capped upside if the stock rises above the strike.

B) Cash-secured put (entry-focused)

- What it is: you sell a put option while setting aside enough cash to buy shares if assigned.

- Why investors use it: to earn premium while waiting to potentially buy at a lower effective price; trade-off is the obligation to buy if the stock falls.

Reality check: Options involve risk and are not suitable for all investors. Covered calls and cash-secured puts can still result in losses, missed upside, early assignment, and outcomes comparable to holding (or being obligated to buy) the underlying shares.

Risks and reality checks

- Not causation: Multi-product clients tended to be more profitable; that doesn’t prove the product mix alone caused it.

- ETFs can fall: Diversification reduces single-name risk, not market risk.

- Bonds can lose money: Especially with rising yields or longer duration.

- Commodities can be very volatile: They can draw down sharply and may not hedge in every environment.

- Options carry significant risk: Covered calls and cash-secured puts can still lead to losses, missed upside, early assignment, and losses comparable to owning the underlying shares (or being obligated to buy them). Options may not be suitable for all investors.

- Behaviour risk is real: Overtrading, panic-selling, or abandoning a plan can overwhelm diversification benefits.

Bottom line

The big takeaway from Saxo’s own client data is simple: portfolios with more than one way to work may be more resilient, and resilience often supports better outcomes.

If you’re stocks-only, you don’t need a complicated overhaul. Common examples investors sometimes explore include: start with an ETF, consider bonds, include a small real-asset diversifier, or use ETO in a simple collateralised way to add structure.