Nvidia earnings: trading the 8% move the options market is pricing

How bullish, neutral and bearish traders can use defined-risk option spreads around one of the market’s biggest earnings events

Key takeaways

- Nvidia reports earnings on 20 May after the US market close, and the options market is already pricing a large post-earnings move.

- Based on the May 22 expiry option chain, the market is currently implying an approximate move of around 8% in either direction.

- Traders often use the expected move as a framework for selecting strikes and structuring trades.

- Implied volatility is elevated into the event, which means post-earnings IV crush can significantly impact option prices.

- This article explores three educational example strategies based on three different outlooks: bullish, neutral and bearish.

Nvidia earnings are no longer just another company update. The company has become one of the central pillars of the AI infrastructure trade, meaning its results often influence sentiment across semiconductors, mega-cap technology stocks and the broader Nasdaq.

The latest official results explain why expectations remain high. Nvidia’s Q4 FY26 revenue rose 73% year-on-year to USD 68.1 billion, while Data Center revenue rose 75% to USD 62.3 billion. Management also guided for Q1 FY27 revenue of approximately USD 78.0 billion, plus or minus 2%.

For traders, however, the key question is often not simply whether Nvidia beats or misses expectations.

The more important question is whether the stock moves more or less than what the options market is already pricing in.

What is the expected move?

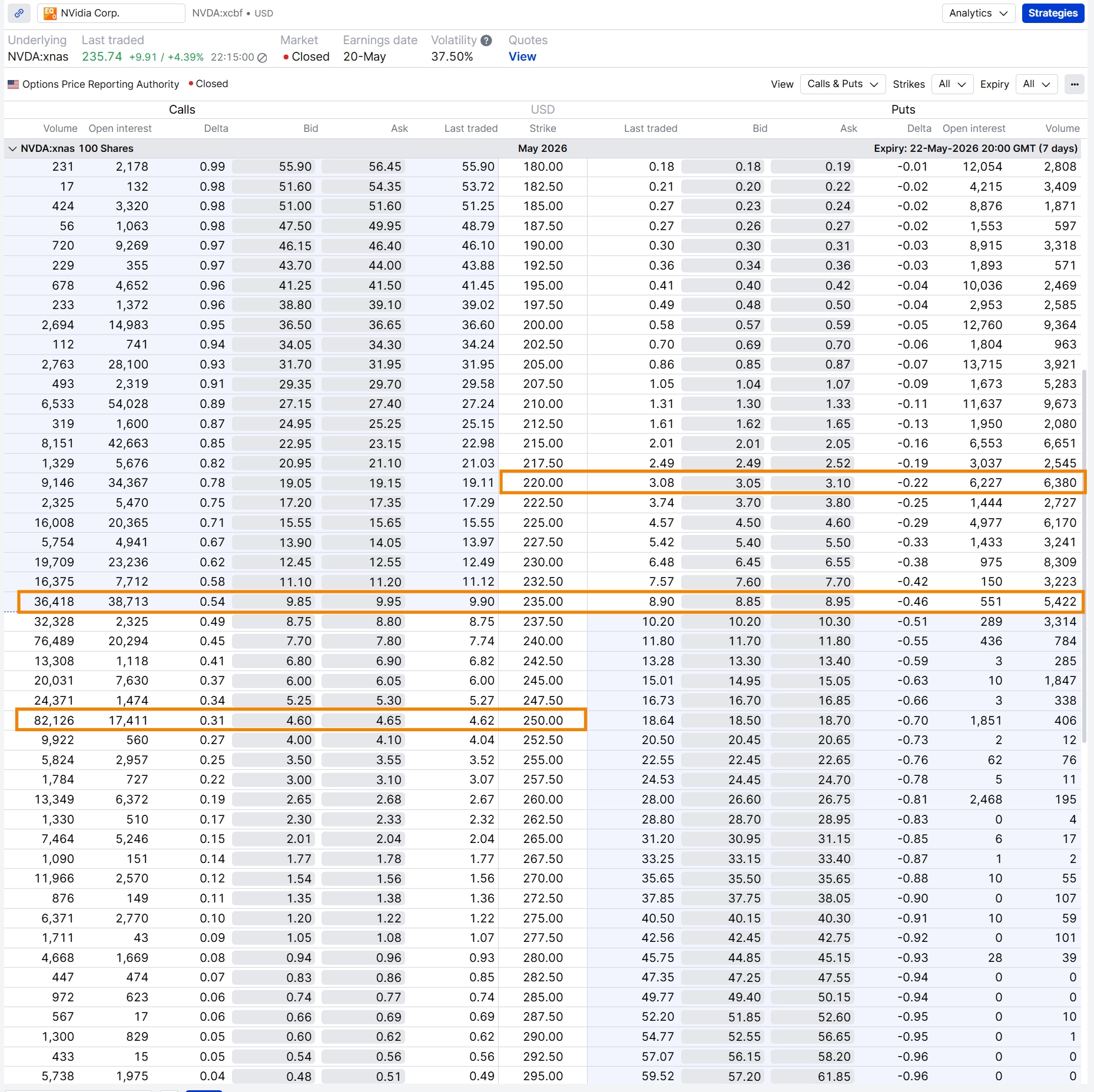

One of the simplest ways traders estimate the market’s implied post-earnings move is by looking at the at-the-money straddle. This involves adding together the premium of the at-the-money call and put for the expiry that captures the earnings event. In the May 22 expiry option chain, the at-the-money 235 call was trading around USD 9.90, while the 235 put traded around USD 8.90.

That produces the following estimate:

Expected move ≈ at-the-money call premium + at-the-money put premium

USD 9.90 + USD 8.90 = USD 18.80

With Nvidia trading around USD 235.74 at the time of observation, the options market was therefore pricing an approximate move of about 8% in either direction. This creates a rough implied range between approximately USD 217 and USD 255.

Importantly, this is not a prediction.

The stock can still move far more or far less than this range. The expected move is simply a reflection of how much movement the options market is pricing into the selected expiry.

For many traders, however, it becomes a useful framework for selecting strikes and comparing possible strategies.

Traders often estimate the expected move using the at-the-money straddle Source: SaxoTrader

Why implied volatility matters around earnings

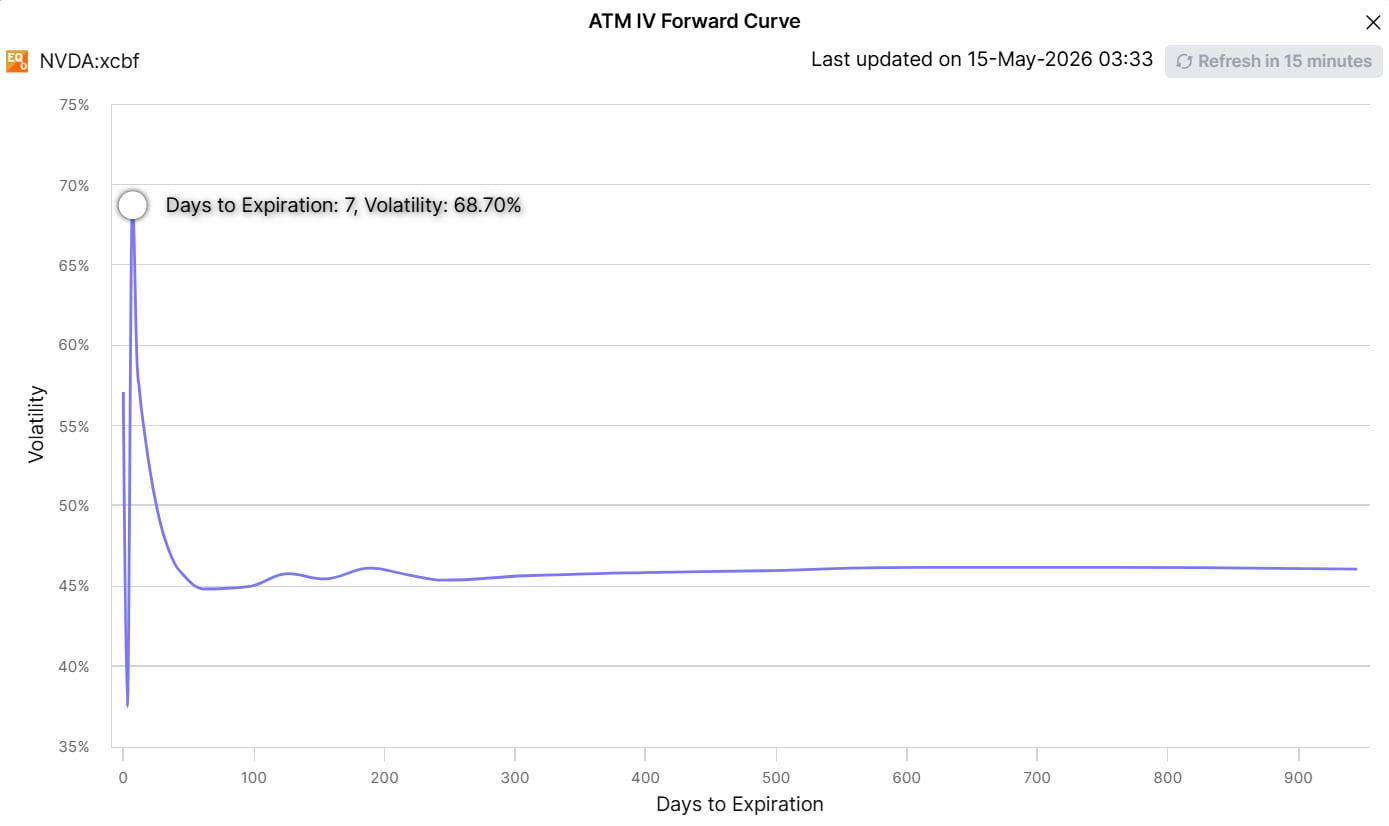

The Nvidia options market is currently pricing elevated implied volatility into the earnings release. That is visible in the implied volatility forward curve, where near-dated expiries trade with significantly higher implied volatility than longer-dated expiries. This happens because traders are willing to pay more for options that capture the earnings event.

Once the earnings announcement has passed, that event premium often disappears quickly. This phenomenon is commonly called the “IV crush”. For long premium strategies such as call spreads and put spreads, this can become a headwind if the stock does not move enough. For short premium strategies such as iron condors, collapsing implied volatility can become a tailwind if the stock remains inside the expected range.

In other words, earnings trades are not only about direction.

The size of the move matters as well.

Near-dated Nvidia options trade with elevated implied volatility ahead of earnings - Source: SaxoTrader

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

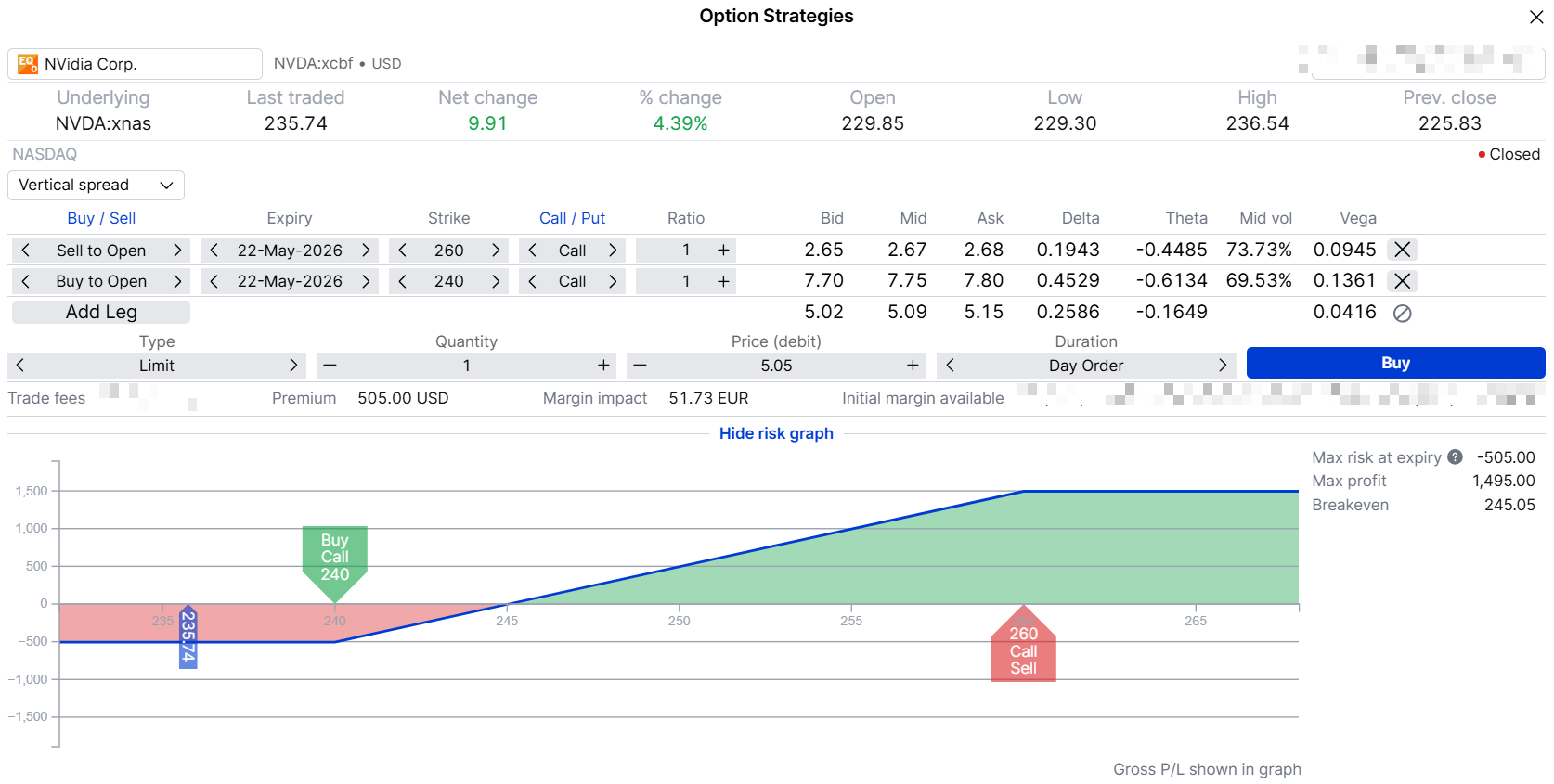

Bullish outlook: bull call spreadA trader with a bullish outlook may believe Nvidia can break above the upper end of the expected move after earnings.

One possible defined-risk strategy is a bull call spread.

Example structure

- Buy 1 May 22 USD 240 call

- Sell 1 May 22 USD 260 call

- Net debit: approximately USD 5.05

- Maximum risk: approximately USD 505

- Maximum profit: approximately USD 1,495

- Break-even at expiry: approximately USD 245.05

The strategy profits if Nvidia rises above the break-even level, while the maximum profit is reached if the stock is at or above USD 260 at expiry.

The short 260 call also helps reduce the upfront cost compared with buying a standalone call option.

That lower cost comes with a trade-off.

While the maximum risk is defined upfront, the upside profit is capped above USD 260.

Strategy insight – defined risk in a high implied volatility environment. Buying options outright can become expensive when implied volatility is elevated. Vertical spreads help reduce that premium cost while keeping the maximum loss limited to the net debit paid at entry. This may make the structure more practical for traders who want directional exposure without committing to the full cost of a standalone option.

This type of structure may appeal to traders who believe Nvidia can continue its strong momentum after earnings, but who still want to limit the capital committed to the trade.

A bull call spread defines both the maximum risk and the maximum profit upfront - Source: SaxoTrader

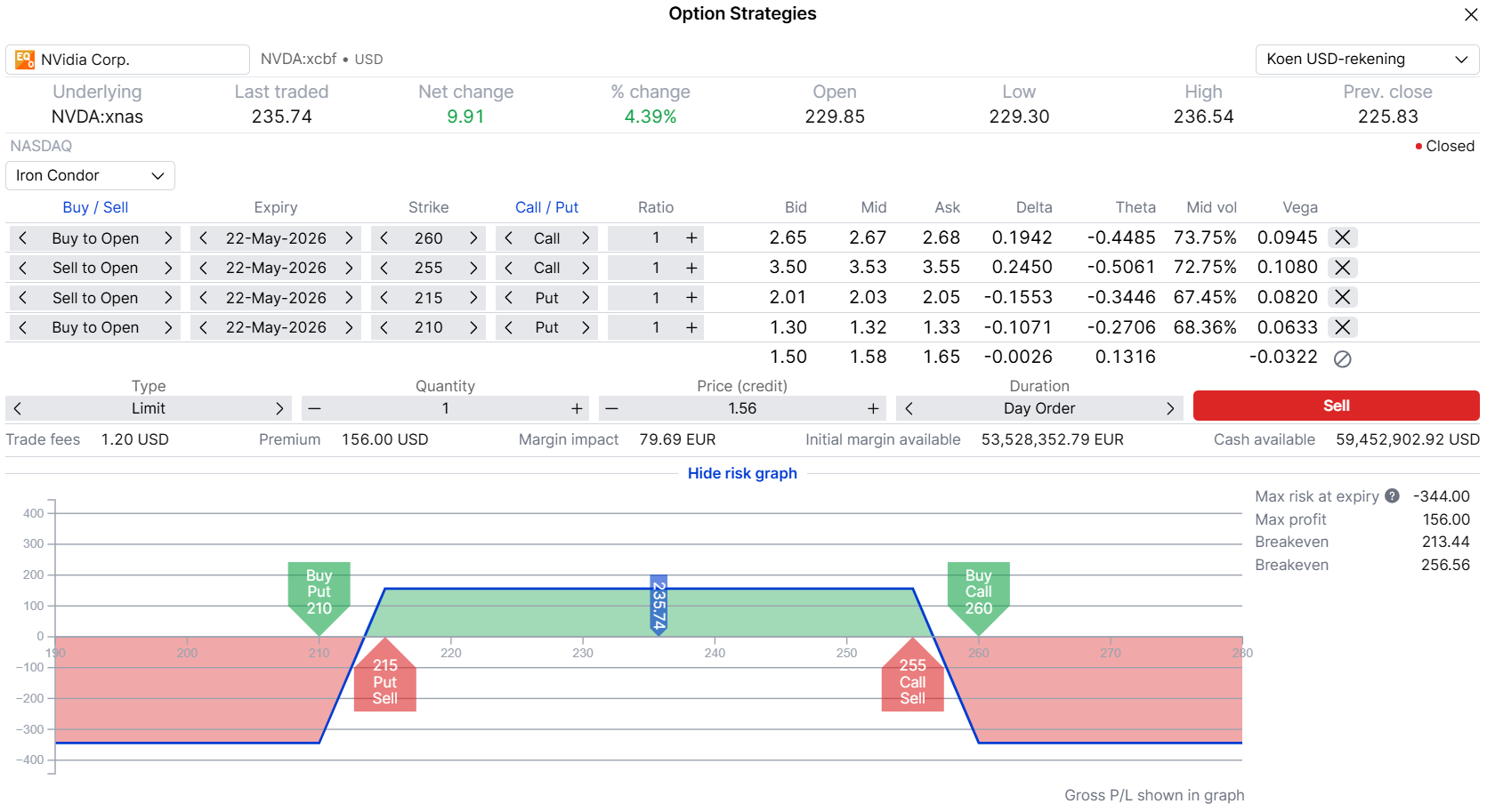

Neutral outlook: iron condor

Not every trader expects a major breakout after earnings.

Some traders instead believe the options market may be overpricing the move.

One possible strategy for that view is the iron condor.

Example structure

- Sell 1 May 22 USD 215 put

- Buy 1 May 22 USD 210 put

- Sell 1 May 22 USD 255 call

- Buy 1 May 22 USD 260 call

- Net credit: approximately USD 1.56

- Maximum profit: approximately USD 156

- Maximum risk: approximately USD 344

- Lower break-even: approximately USD 213.44

- Upper break-even: approximately USD 256.56

The iron condor is a defined-risk short volatility strategy.

The trader receives premium upfront and hopes Nvidia remains broadly within the expected range after earnings.

In this example, the short strikes near USD 215 and USD 255 are positioned close to the lower and upper expected-move levels derived from the option chain.

If Nvidia remains between the short strikes at expiry, the trader keeps the full premium received.

Strategy insight – short volatility and position sizing. Traders should not confuse limited risk with low risk. A sharp earnings surprise can still quickly push the position toward its maximum loss. Iron condors may therefore require active management and careful position sizing, especially during highly volatile earnings periods.

Strategy insight – Some traders prefer to wait until after the earnings release before opening an iron condor. Entering the position shortly after the market opens the next day can significantly reduce the directional “gap risk” associated with the earnings announcement itself, while still allowing the trader to capture some remaining implied volatility premium. The trade-off is that the first 30 minutes after the open are often highly volatile and fast-moving, with wide bid-ask spreads and rapidly changing option prices. This can make it more difficult to obtain the desired entry price or structure the position efficiently.

An iron condor benefits if the post-earnings move remains contained - Source: SaxoTrader

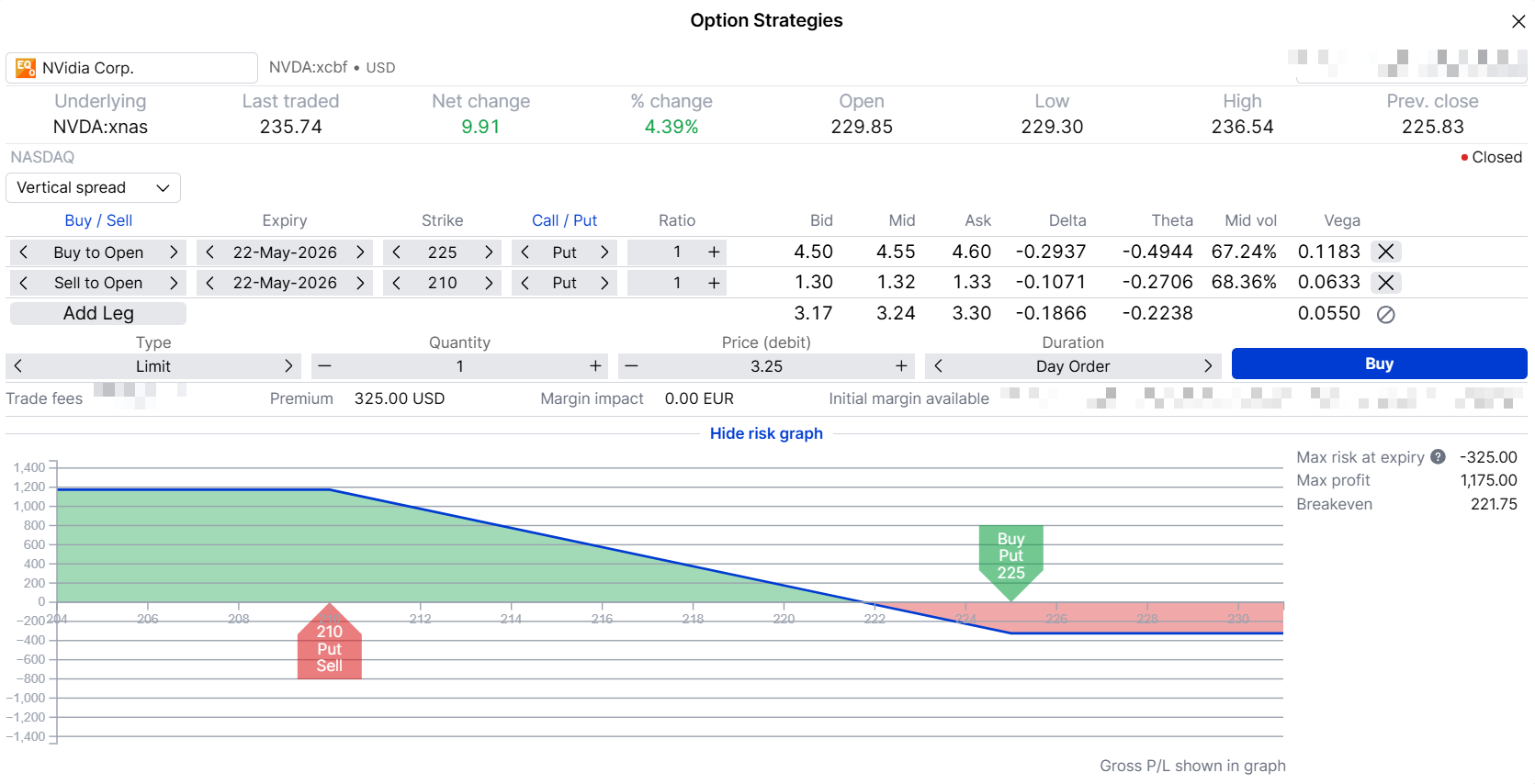

Bearish outlook: bear put spread

A bearish trader may believe expectations have become too optimistic heading into the earnings release.

Another possibility is that Nvidia delivers strong numbers, but still disappoints a market that had expected even more.

One defined-risk bearish strategy is the bear put spread.

Example structure

- Buy 1 May 22 USD 225 put

- Sell 1 May 22 USD 210 put

- Net debit: approximately USD 3.25

- Maximum risk: approximately USD 325

- Maximum profit: approximately USD 1,175

- Break-even at expiry: approximately USD 221.75

The strategy benefits if Nvidia declines after earnings.

Buying the 225 put provides bearish exposure, while selling the 210 put helps reduce the upfront premium paid.

As with the bull call spread, the trader accepts a capped maximum profit in exchange for a lower entry cost.

Strategy insight – the “sell the news” scenario. A bear put spread may appeal to traders who expect weakness after earnings, but who do not want the full premium exposure of buying a standalone put option in a high implied volatility environment. The spread structure reduces the initial debit while still providing meaningful bearish exposure down to USD 210.

A bear put spread provides defined-risk downside exposure - Source: SaxoTrader

A bear put spread provides defined-risk downside exposure - Source: SaxoTrader

Final thoughts

Earnings season often creates some of the largest implied moves of the quarter, and Nvidia remains one of the market’s most closely watched event-driven stocks.

For active investors and explorative traders, the option market can provide more than just speculation.

It can also provide a framework. The expected move helps traders understand how much volatility is already priced into the stock. From there, traders can decide whether they believe Nvidia will outperform that expectation, remain inside it, or break below it.

The three example strategies discussed here reflect those different views.

None of them remove risk.

But each demonstrates how defined-risk option structures can help traders shape their exposure more deliberately around one of the market’s biggest earnings events.