Alphabet after earnings: how a covered call can help investors manage a strong rally

Key takeaways

Alphabet shares have rallied sharply after earnings, leaving some long-term shareholders with a familiar question: should they simply keep holding, take some profit, or use a more structured approach?

For investors who already own at least 100 Alphabet Class A shares, a covered call can be one way to set a disciplined potential selling price while receiving option premium upfront.

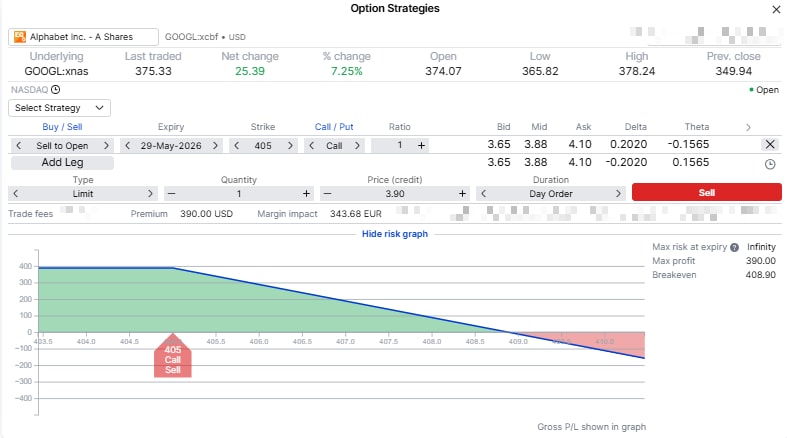

In this example, the investor sells the 29 May 2026 USD 405 call for around USD 3.90 per share. That creates about USD 390 in premium before costs, but it also caps upside above the USD 405 strike price.

A covered call should only be considered by investors who are genuinely comfortable selling their shares at the chosen strike price if the option is exercised.

Alphabet shares have moved sharply higher after earnings, trading well above the 50-day and 200-day moving averages shown in the chart. Source: SaxoTrader

Alphabet has rallied. What now?

Alphabet’s latest earnings update was followed by a strong move in the share price. In the screenshot, GOOGL is trading around USD 376–378 after the rally. The chart also shows the share price well above its short- and long-term moving averages, which underlines how far the move has stretched in a relatively short period.

For a long-term investor, this does not automatically mean the stock has gone too far. A strong company can keep rising. But after a sharp rally, it is reasonable to ask whether the next step should be passive holding or a more deliberate plan.

That is where a covered call can come in.

What is a covered call?

A covered call is an options strategy for investors who already own the underlying shares. In this case, the investor owns 100 Alphabet shares and sells 1 call option against those shares.

A call option gives the buyer the right to buy shares at a fixed price, called the strike price, before or at expiry. When you sell that call, you receive premium upfront. In return, you accept the obligation to sell your shares at the strike price if the option is exercised.

The word “covered” matters. It means the investor already owns the shares that may need to be delivered. This is different from selling a call without owning the shares, which carries far greater risk and is not the focus here.

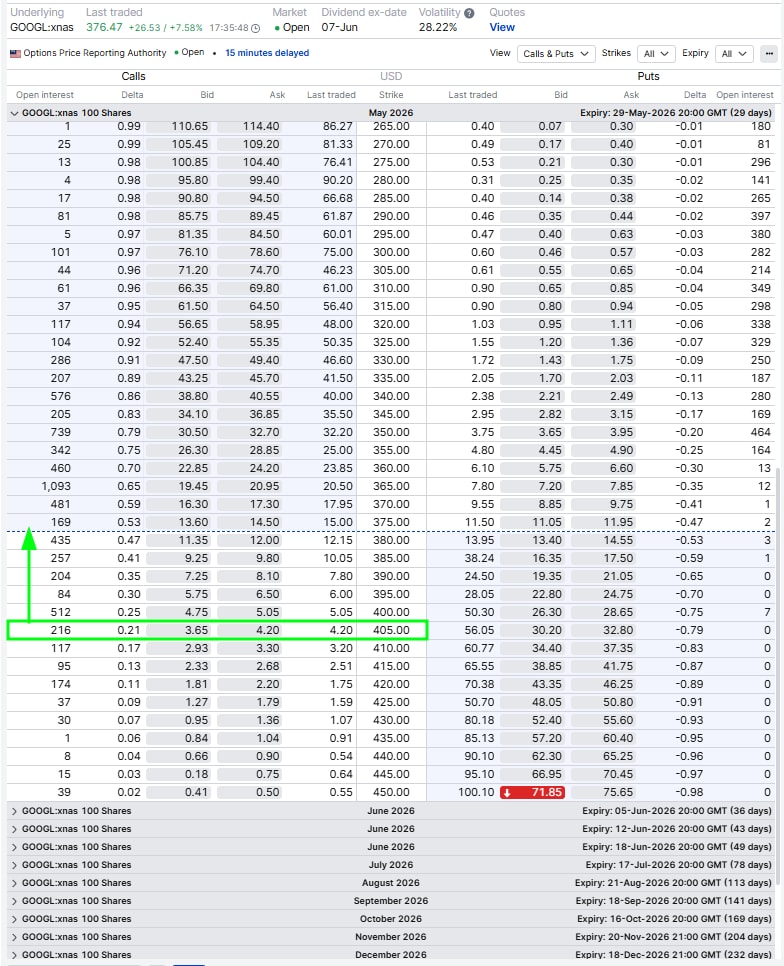

The Alphabet example

In the option chain, the highlighted example is the 29 May 2026 USD 405 call. The order ticket shows a sale price around USD 3.90 per share.

Since a standard US equity option contract normally represents 100 shares, selling 1 call at USD 3.90 would generate about USD 390 in premium before commissions, fees, and taxes.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

The key numbers are:

- Current GOOGL share price shown: around USD 376.47

- Call option sold: 29 May 2026 USD 405 call

- Option premium received: around USD 3.90 per share

- Total premium: around USD 390 per 100-share contract

- Strike price: USD 405

- Expiry: 29 May 2026

This means the investor is not selling Alphabet immediately. Instead, they are saying: “If Alphabet rises above USD 405 by expiry, I am comfortable selling my 100 shares at USD 405.”

The example uses the 29 May 2026 USD 405 call, which is above the share price shown in the screenshot. Source: SaxoTrader

What the premium means in plain numbers

If GOOGL is around USD 376.47 and the investor sells the USD 405 call for USD 3.90, the covered call creates 2 sources of potential return if the shares are called away.

First, the investor receives USD 390 in premium. Second, the shares could rise from USD 376.47 to the USD 405 strike price before being sold.

The simple calculation looks like this:

- Premium received: USD 390

- Share upside to strike: USD 28.53 × 100 = USD 2,853

- Total potential gain before costs if assigned at USD 405: about USD 3,243

- Effective sale level including premium: USD 408.90

There is also a useful income-style way to look at the premium. If the call expires worthless, the investor keeps the 100 shares and the USD 390 premium. Based on a share price of USD 376.47, the 100-share position is worth about USD 37,647. The USD 390 premium equals about 1.0% of that share value before costs.

That 1.0% is not a guaranteed total return. It is the option premium received if the call expires worthless. If Alphabet falls, the investor still owns the shares and can lose much more on the stock than the premium received.

What can happen by expiry?

The easiest way to understand a covered call is to look at scenarios.

| Alphabet at expiry | What happens | Result for the investor |

|---|

| Below USD 405 | The call will likely expire worthless | The investor keeps the shares

and the USD 390 premium |

| Around USD 405 | Assignment risk increases | The investor may keep the shares or may be assigned,

depending on the final price and exercise |

| Above USD 405 | The shares are likely to be called away | The investor sells 100 shares at USD 405

and keeps the USD 390 premium |

| Far above USD 405 | Upside is capped | The investor misses gains above USD 405,

apart from the premium received |

This is the central trade-off. The investor receives premium today, but gives up some future upside if Alphabet keeps rallying strongly.

Why use this strategy?

For a buy-and-hold investor, a covered call can serve 3 practical purposes.

First, it can generate additional income from shares already held in the portfolio. In this example, the premium is about USD 390 before costs.

Second, it can create a disciplined exit level. If the investor would be happy to reduce or sell the Alphabet position at USD 405, the covered call turns that decision into a structured plan.

Third, it can add a small cushion if the share price weakens. The USD 3.90 premium reduces the effective cost of the position by that amount per share, but only slightly. It does not protect the investor from a large fall in Alphabet’s share price.

What are the risks?

The main risk is not hidden complexity. It is misunderstanding the trade-off.

If Alphabet trades above USD 405 near expiry, the investor should be prepared for the shares to be sold at USD 405. That may feel fine when entering the trade, but it can feel less comfortable if the share price later trades at USD 430 or USD 450.

The second risk is downside exposure. A covered call does not protect the share position in the way a put option would. If Alphabet falls sharply, the investor still owns 100 shares, and the USD 390 premium only offsets a small part of that loss.

The third risk is execution. The option chain shows a bid-ask spread, meaning there is a difference between what buyers are willing to pay and what sellers are asking. Using a limit order can help investors avoid accepting a poor price, but live prices can change quickly.

The order ticket shows the sale of 1 Alphabet USD 405 call expiring 29 May 2026, with an example premium around USD 390 before costs. Source: SaxoTrader

A note on the order ticket risk graph

The order ticket shows the short call as a single option leg. That is why the ticket may display risk in a way that looks alarming when viewed on its own.

For a covered call investor, the option should be viewed together with the 100 shares already owned. The investor’s downside risk mainly comes from the share position falling. The investor’s upside is capped because the shares may need to be sold at USD 405.

This distinction matters. A covered call is not risk-free, but it is also not the same as selling an uncovered call.

Final takeaway

A covered call can be a practical strategy for an Alphabet shareholder after a strong earnings rally, but only when the investor is clear about the trade-off.

In this example, selling the 29 May 2026 USD 405 call could generate about USD 390 in premium before costs. If the call expires worthless, that is around 1.0% of the share value shown in the example. If Alphabet rises above USD 405, the investor may have to sell the shares at that price and give up further upside.

The key question is simple: would you be comfortable selling 100 Alphabet shares at USD 405 by 29 May 2026?

If the answer is yes, the covered call may be worth studying. If the answer is no, the premium is probably not enough compensation for giving up the upside.