Key points:

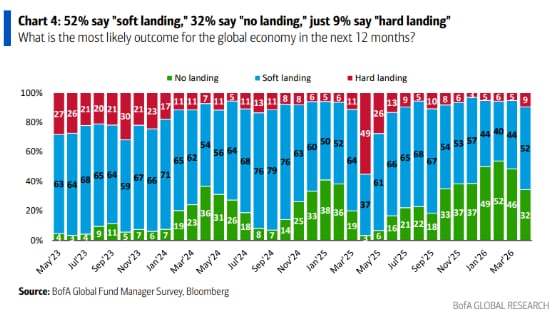

The latest BofA Fund Manager Survey shows a sharp downgrade in growth expectations and a clear rise in inflation worries, but the base case is still a soft landing rather than recession.

Positioning has turned more defensive, yet not defensive enough to suggest panic. Equity exposure has been cut, cash has risen, and regional leadership is shifting, but investors have not fully abandoned risk.

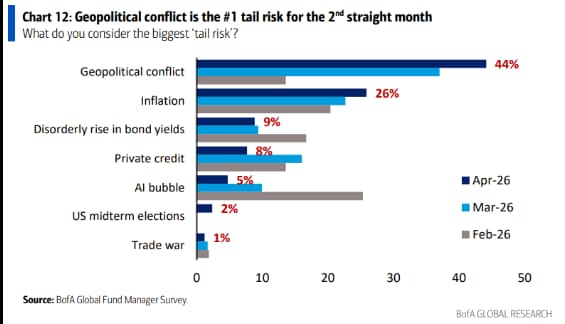

Geopolitics remains the dominant tail risk, and the market is treating oil as the main transmission channel into inflation, yields, and sentiment.

The key point is that expectations are cooling faster than fundamentals are collapsing. That signals caution, not capitulation. In our view, that can create a more balanced setup if the pressure points begin to ease.

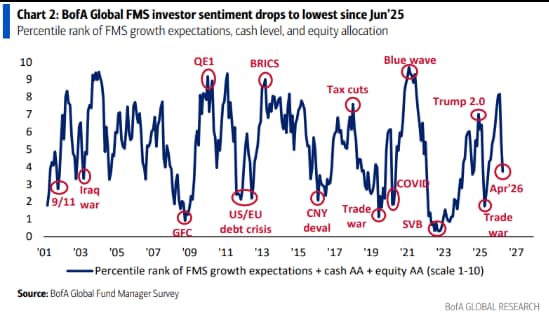

The April 2026 BofA Global Fund Manager Survey — drawn from 193 fund managers overseeing $563 billion in assets and conducted April 3–9 — delivers the starkest bearish reading in ten months. But, it is not a survey of panic. It is a survey of recalibration.

Managers have become notably more cautious as growth expectations weaken and inflation concerns re-accelerate. But they have not positioned for a deep recession or a full exit from risk.

In practical terms, investors are no longer paying up for broad optimism. They are becoming more selective about where they want exposure, more sensitive to macro risks, and more cautious about crowded trades. But that caution is not the same as capitulation. In our view, that can create a more balanced setup if the pressure points begin to ease.

The key point is that expectations are cooling faster than fundamentals are collapsing. In our view, that leaves the market in an uncomfortable but potentially constructive middle ground: cautious enough to be defensive, but not so fearful that it cannot respond to better news.

Macro signals: lower growth, more inflation, but still soft landing

The macro message from the survey is clear. Managers have turned materially more downbeat on growth while becoming more worried about inflation. That is why stagflation fears have risen so sharply in the latest reading.

But the survey stops short of an outright recession call. The base case still leans toward a soft landing, and a clear majority of respondents say recession remains unlikely. That makes this survey important not because it signals collapse, but because it signals a less comfortable regime.

What has changed is the mix. Investors are no longer just worried about slower growth, but slower growth with stickier inflation — a much harder backdrop for both markets and policymakers.

That shifts what investors reward: less pure beta, more pricing power, stronger balance sheets, and resilient earnings.

This is why the survey should be read as a regime-shift signal rather than a generic bearish one. The market is moving away from the comfort of disinflation and broad easing hopes, and toward a backdrop where quality and resilience carry more weight.

Geopolitical signals

Geopolitics has become the dominant tail risk in the survey, and that is not just because of headline risk. It is because markets increasingly see geopolitical conflict as the mechanism through which inflation, yields, and growth concerns can all worsen at once.

Several survey takeaways reinforce that point.

Many respondents expect the current conflict to end as early as April 2026, which creates a near-term sentiment reversal catalyst if de-escalation materialises.

Fewer than one-third expect full normalisation of shipping through the Strait of Hormuz by mid-year, suggesting supply disruption risk is likely to outlast any ceasefire headline.

Russia-Ukraine resolution expectations remain near zero, reinforcing the idea that geopolitical stress is not fading from the macro backdrop any time soon.

That combination matters. Investors may be willing to price a ceasefire, but they are not yet willing to price a full reset. In other words, the survey suggests markets may get relief from diplomacy, but not full comfort.

Positioning signals

The positioning picture is defensive, but not extreme. Investors have reduced equity exposure and raised cash, yet not to the levels that usually mark outright capitulation.

Equity allocation

Global equity allocation has fallen sharply to a net 13% overweight, down from 37% overweight in March. That is a meaningful de-risking move, but it is still an overweight. Investors have cut risk, not abandoned it.

Cash allocation

Cash levels have risen to 4.3%, the highest since May 2025. But that is still below the classic 5% threshold that usually signals true fear. In other words, managers are more cautious, but they are not hiding in cash.

U.S. vs Europe vs Asia

Regional positioning shows a market becoming far more discriminating.

U.S. equities improved to a net 10% underweight from 17% underweight in March. Investors are still underweight, but less aggressively so.

Eurozone equities fell to a net 4% overweight from 21% overweight in March, showing one of the sharpest sentiment deteriorations in the survey.

Emerging markets remain the most favoured regional position, though the overweight narrowed to 41% from 53% in March.

Japan saw one of the most notable reversals, falling to a net 11% underweight from a net 14% overweight in March.

That tells us the market is not rotating into a single new consensus. It is cutting exposure where growth and energy vulnerability look more exposed, while becoming more cautious even on areas that had previously enjoyed strong structural support.

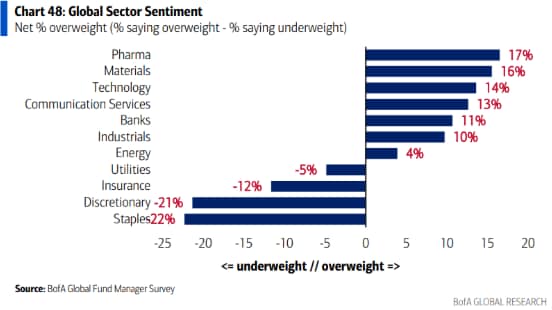

Sector positioning

The sector snapshot suggests this is not a clean defensive rotation, nor a full return to risk-on leadership.

Investors added to communication services, technology, and discretionary this month, while trimming healthcare, staples, and banks. The broader takeaway is that positioning is becoming more selective. There is a tentative willingness to add back to growth-sensitive areas, especially tech and communications, but not enough to suggest a broad cyclical embrace.

So the message from the sector chart is that investors are starting to reopen some growth exposure, while still keeping an overall bias toward resilience and quality. That fits the broader survey message: caution is easing at the margin in parts of the market, but conviction is not fully back.

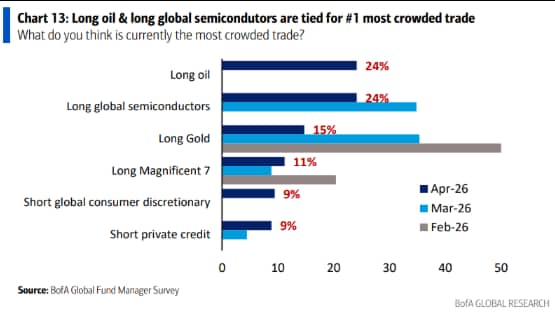

Commodities: oil vs gold

Commodity positioning is one of the clearest messages in the survey.

Long oil is now one of the most crowded trades at 24%.

Long global semiconductors is tied with oil as the most crowded trade.

Long gold has fallen well down the crowded-trade ranking, at 15%.

That is a notable shift. Gold is no longer the market’s default geopolitical hedge. Oil has taken that role because it sits much closer to the inflation and growth transmission channel. But crowding also means investors should be careful. Oil may still work as a hedge, but it is no longer an under-owned one.

Structural USD weakness

The survey still points to a medium-term bias toward dollar weakness, even if geopolitics can support the dollar tactically in the short run.

A majority of respondents expect the U.S. dollar to weaken over time, with slowing growth concerns outweighing near-term safe-haven demand.

More than half of participants cited loose monetary policy and risks to Federal Reserve independence as potential structural headwinds for the dollar.

Investors remain net underweight the U.S. dollar, continuing a consensus that has been building for several months.

That matters because it reinforces the idea that even in a world of geopolitical stress, investors do not see the dollar as an unambiguous long-term winner.

Why we are cautiously optimistic

The latest BofA Fund Manager Survey still reflects a cautious market, but the setup is not as bleak as the headline sentiment suggests.

First, geopolitics, while still a risk, may be starting to cool at the margin. Many respondents expect the current conflict to end as early as April 2026, which means markets may begin to price a better backdrop before full clarity arrives. That does not remove the risk of renewed disruption, especially through oil and shipping, but it does suggest the worst fears may no longer be intensifying at the same pace.

Second, some of the most crowded positioning has already been corrected. Equity exposure has been cut sharply, cash has risen, and sector positioning suggests investors have become more selective rather than euphoric. Tech positioning also looks less stretched even as earnings expectations remain relatively firm. In our view, that leaves the market less vulnerable to the kind of unwind that usually follows an overcrowded consensus.

Third, bearish positioning can become a bullish signal if the macro and geopolitical backdrop starts to cooperate. When sentiment is cautious, expectations are lower and the bar for positive surprises comes down. That does not guarantee upside, but it does mean improving oil dynamics, resilient earnings, or clearer signs of de-escalation could have an outsized impact on sentiment.

Risks to the view

The constructive case is straightforward. If geopolitical risks continue to cool, oil stabilises, and earnings remain resilient, then today’s defensive positioning could support a more constructive market backdrop. In our view, in that scenario, the current caution may look less like a warning sign and more like latent capacity for sentiment to improve.

But that optimism should remain cautious. If peace proves fragile, oil moves higher again, or earnings guidance starts to weaken, then the same defensive positioning could deepen rather than reverse. That is why the two most important signals from here remain oil and earnings, with geopolitics shaping both.

In our view, the survey does not point to capitulation. It points to a market that has already de-risked, corrected some crowding, and may be better placed to respond if the backdrop improves — but still vulnerable if it does not.