口座開設は無料。オンラインで簡単にお申し込みいただけます。

最短3分で入力完了!

コモディティ戦略責任者(Saxo Group)

サマリー: 2023年は商品市場にとって、ジェットコースターのような年でした。年初は中国のロックダウン解除への期待が高まり、市場は楽観に包まれていました。しかし、インフレ抑制を目的とした中央銀行の利上げが激化し、経済の低迷懸念が強まるにつれ、市場は次第に緊張を強めていきました。経済成長や需要への懸念はエネルギーや工業用金属に重くのしかかりましたが、一方で気候変動による天候の変化も大きく影響し、好調な銘柄もあれば、低迷に苦しむ銘柄も生まれました。

※本レポート内日本語は、ご参考情報として原文(英語)を機械翻訳したものです。

2023年、商品市場はどのような年だったのか?振り返れば、希望と失望が入り混じった、なかなか複雑な1年でした。経済成長や需要への懸念がエネルギーや工業用金属に重くのしかかり、一方で気候変動が思わぬ好材料、悪材料を生み出すなど、まさに嵐の中の航海のような年でした。

年初は、数ヶ月におよぶコロナ禍のロックダウンから解放された中国の再開に注目が集まり、市場は幸先の良いスタートを切りました。しかし、インフレ抑制を目的とした中央銀行の継続的かつ積極的な利上げによる景気下振れリスクへの懸念が市場で強まり、すべてが順調だったわけではありません。こうした懸念が和らぎ始めたのは、ようやく各中央銀行が利下げに転じる可能性が高いと市場が判断した第四半期に入ってからです。中東での戦争、ウクライナでのロシアの継続的な攻撃、紅海での船舶攻撃など、地政学的リスクが高まり、世界の分断が進んだ1年でした。

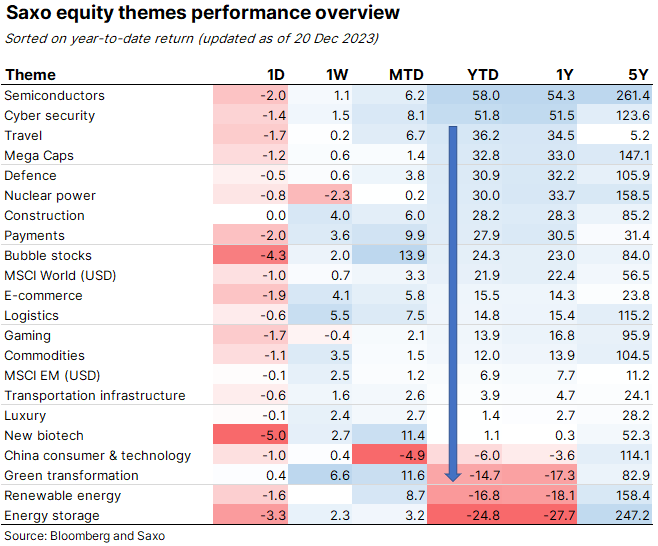

グリーントランスフォーメーションも大きな潮流となりましたが、特に中国では燃料需要がピークを迎える可能性が高く、関連企業は厳しい局面に直面しました。金利上昇とコスト高騰により、評価額が急落し、後半には売り圧力が高まりました。サクソバンクの株式テーマ別パフォーマンスでも、グリーントランスフォーメーション、再生可能エネルギー、エネルギー貯蔵が最下位に低迷する一方、コモデティテーマは年間約12%のプラスリターンと中位に位置しています。

しかし、来年には資金調達コストが低下し、気候変動対策への取り組みも進むことから、2024年にはこれらの低位セクターが復活する可能性があります。ガス、原油、石炭の需要も過去最高を更新しており、世界的なエネルギー需要の増加が続く中、この移行プロセスは今のところ、より環境に配慮したものとなっています。

330ドルの幅で取引された後、年初来で約12%上昇した金は、中央銀行の継続的な需要やアジアの個人投資家の買いが牽引し、米国の短期金利が上昇を続ける中、実質利回りの急上昇やポジションを保有するための資金調達コストの上昇に注目する投資家の継続的な売りを相殺する形で、やや驚くほど堅調なパフォーマンスを示しました。しかし、この上昇の大部分は、中央銀行が金利の次の動きが低くなる可能性が高いことを最終的に示唆した第4四半期中に実現したことは注目に値します。

ニッケル、亜鉛、アルミの低迷が主因で、スズの上昇で一部相殺されました。すでに低い在庫水準にあり、資金調達コストが下がるにつれて産業用ユーザーからの補充が見込まれることから、2024年も銅市場は引き続き下支えされるものと思われます。

ブレントは、ウクライナ戦争によって相場が急騰し、その後暴落した2022年の64ドルのレンジに比べ、比較的小さな27.5ドルのレンジで1年を過ごしました。現在の価格は80ドル前後で、年初の平均価格より数ドル低い程度です。この比較的小さなレンジは、OPEC+が積極的な供給管理を通じて安定した価格を維持しようとしているためです。しかし、OPEC+が価格の上昇を望んでいることは間違いありませんが、米国やイランなどからの生産量の増加と第4四半期の需要の低迷により、OPEC+は市場シェアを手放す一方で価格上昇に失敗しており、半分の勝利にとどまっています。

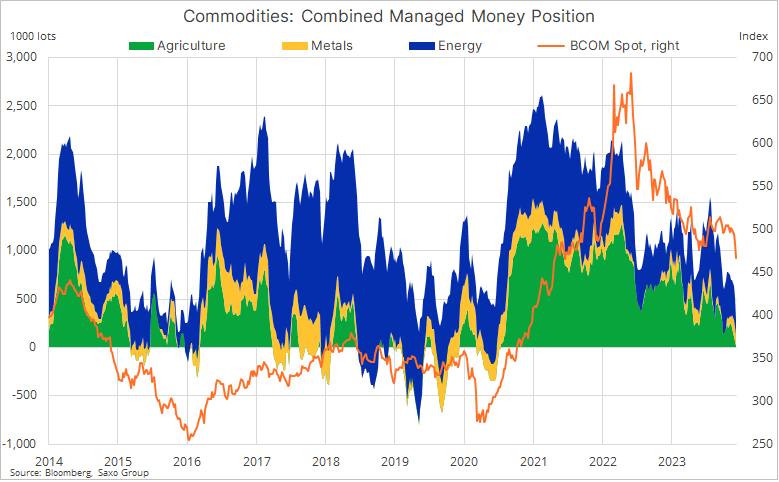

10月以降、ヘッジファンドと商品取引顧問(CTA)による売りが続いた結果、主要24商品先物のネット・ロング・ポジションは、コモディティ、特に燃料に対する世界的な需要が崖っぷちに落ち込んだ2020年初頭のコビド危機の最盛期の水準にまで崩壊しました。

こうした動きは、中国をはじめとする世界の成長不安や、資金調達コストの急上昇によって産業界が過剰在庫の削減に動く中、2023年に苦戦を強いられた資産クラスがますます過小評価されていることを浮き彫りにしています。また、2024年にテクニカルおよび/またはファンダメンタル的な見通しが支援材料となり、新たな買いやショートカバーが入るような状況が整えば、このセクターが力強く回復する可能性もあります。このような変化を引き起こす要因としては、利下げによって資金調達コストが低下し、それに伴って内在するコンタンゴが業界の在庫補充につながること、OPECが原油供給を厳格に管理していること、そしてとりわけ、主要国経済全体の景気減速リスクを相殺するのに役立つ主要コモディティ全体の需給逼迫の兆しがあることなどが考えられます。

Summary: A look back on developments that shaped the commodities market in 2023, a year that began on an optimistic note with focus on China’s reopening after months of Covid-related lockdowns sending the market off to a good start. But it wasn’t all bliss as markets grew increasingly worried about the risk of an economic fallout from continued and aggressive central bank rate hikes aimed at bringing inflation under control. Aside from economic growth and demand concerns weighing on energy and industrial metals, diverging weather developments played an important role, leading to some of the best, but also worst performances.As the 2023 hourglass runs out, it’s time to reflect on what kind of year it has been for commodities: a pretty mixed bag filled with good, bad and surprises. Aside from economic growth and demand concerns weighing on energy and industrial metals, diverging weather developments played an important role, leading to some of the best, but also worst performances.

The year began on an optimistic note with focus on China’s reopening after months of Covid-related lockdowns sending the market off to a good start. But it wasn’t all bliss as markets grew increasingly worried about the risk of an economic fallout from continued and aggressive central bank rate hikes aimed at bringing inflation under control. These concerns only began to ease this quarter when markets finally received a nod that the next move in rates would likely be lower. A war in the Middle East, Russia’s continued aggressions in Ukraine, and attacks on ships in Red Sea all added up to a year that saw increased geopolitical risks and with that an increasingly fragmented world.

It was also a year that saw the green transformation gather momentum, especially in China where fuel demand looks set to peak next year. However, that focus did little to support capital intensive companies involved with the transition as they faced heavy selling pressure during the second half of the year amid lofty valuations coming under pressure from a rapid rise in the cost of money as interest rates and yields surged higher. Saxo’s equity themes highlight this weakness with green transformation, renewable energy and energy storage being the worst performing themes while the commodities theme is found near mid-table after returning around 12%.

However, with funding costs coming down next year and with ongoing efforts to combat climate change, we suspect these under-owned sectors could see a comeback in 2024. With global demand for energy still rising, this transition process however is for now more of a green addition, after demand for gas, crude and coal also reached fresh record highs.

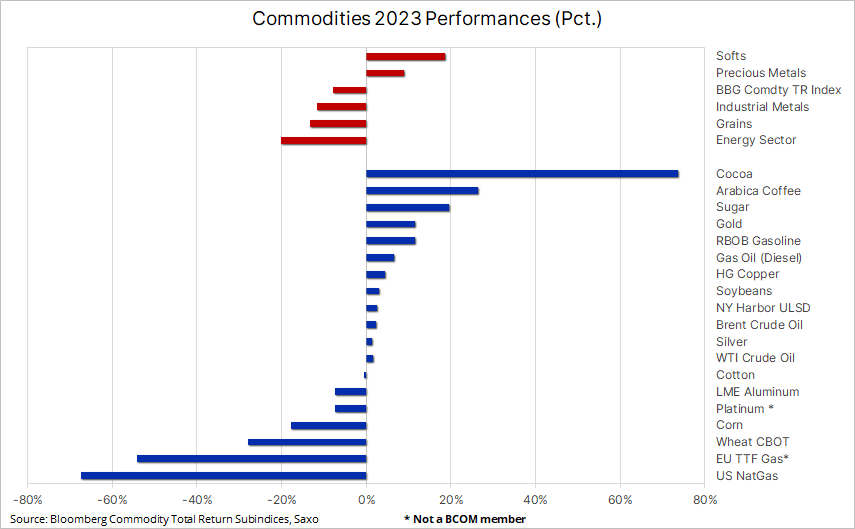

In the previous two years, the Bloomberg Commodity Total Return Index – which tracks the performance of 24 major commodity futures, spread almost evenly between energy, metals and agriculture – has returned 27% in 2021 and 16% in 2022. With that in mind, it was probably not unreasonable, given the challenges this past year, to see the index give back around 8%. Do note that if we exclude US natural gas, which slumped 67%, from the index it would trade near unchanged on the year.

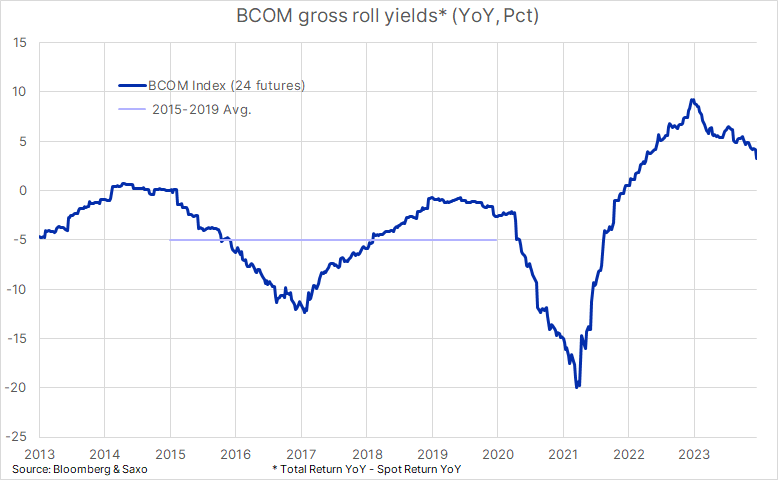

Supporting returns was another year where several key commodities traded in backwardation, a situation that reflects tight market conditions, and it helped create a positive roll yield when expiring futures contracts were rolled into a lower priced next month contract. While the year-on-year roll yield has moderated to 3.3% from around 9.4% this time last year, it is still providing some tailwind for investors that was absent in the pre-Covid years when the roll yield was averaging around -5%.

At the beginning of the year the tightness was primarily seen across the energy sector – where crude oil and refined products, such as gasoline and especially diesel were very tight amid Russian sanctions and China demand optimism. However, from May onwards, the agriculture sector took over as El Niño weather developments, primarily across the Southern Hemisphere, helped trigger tight market conditions and surging prices of sugar, cocoa and coffee – this year’s top three performers - thereby more than offsetting the negative pull from weaker grain prices following a robust Northern Hemisphere harvest season.

As per the table below, we can see the role that some key commodities have played in helping bring inflation under control. The UN Food and Agriculture Organization (FAO) food price index showed a 10.7% year-on-year drop in November, led by declines in grains such as wheat and corn, as well as vegetable oils and dairy. Natural gas, a key source of energy used in power generation, suffered major declines across the world, most notably in the US where record production and high inventories and mild weather helped drive a 67% slump, but also in Europe where gas prices continued lower following their 2022 surge amid strong production from renewable sources, mild weather, an improved ability to receive Liquefied Natural Gas (LNG) to replace pipelined gas from Russia, and not least weaker industrial demand.

Gold, up around 12% on the year after trading within a wide 330 dollar range, delivered a somewhat surprisingly robust performance, driven by continued central bank demand and retail buyers in Asia, in the process more than offsetting continued selling from investors focusing on sharply higher real yields and the rising funding cost of holding a position amid the continued rise in US short-term interest rates. It is, however, worth noting that the bulk of the gain was realized during Q4 when central banks finally indicated the next move in rates would likely be lower.

A 12% slump in the Bloomberg Industrial Metal index was primarily driven by weakness in nickel, zinc and aluminum, and only partly offset by gains in tin and not least copper which gained 5% amid surprisingly strong demand in China, not least from the green transition given its usage in multiple applications. As the year comes to a close, the copper market has found support from multiple short- and long-term supply disruptions, and together with already low inventory levels, potential restocking from industrial users as funding costs come down, we are likely to see continued support in 2024.

Brent spent the year trading in a relatively small 27.5 dollar range compared with the 64 dollar range seen in 2022 when the war in Ukraine drove the market sharply higher, before collapsing. At the current price of around $80, it trades just a couple of bucks below the average for the year, and this relatively small range can be credited to OPEC+ and its attempt to maintain stable prices through actively managing supply. There is no doubt, however, that the group would like to see prices higher but rising production from the US and Iran among others, together with Q4 demand weakness, has left the group with only with a half victory given the failure to boost prices while surrendering market share.

Continued selling since October by hedge funds and commodity trading advisors (CTA) has resulted in the net long position across 24 major commodity futures collapsing to levels last seen at the depths of the Covid crisis in early 2020 when global demand for commodities, especially fuel, fell off a cliff.

These developments highlight an increasingly under-owned asset class which has struggled in 2023 amid growth worries in China and the wider world, and a sharp rise in funding costs leading industries to reduce excess inventories. It also highlights a sector which, given the right circumstances, may see a strong recovery in 2024 once the technical and/or fundamental outlook becomes more supportive, thereby leading to fresh buying and short covering. Drivers that may trigger such a change could be rate cuts lowering the funding costs and with that the inherent contango leading to industry restocking of inventories, OPEC maintaining a tight control of the supply of crude oil, and not least signs of tightness across key commodities that will help offset the risk of an economic slowdown across key economies.

Commodity articles:

19 Dec 2023: Crude and gas pop on Red Sea Disruption Risks

14 Dec 2023: Fed's dovish tilt adds fresh fuel to precious metals

13 Dec 2023: Video - Why gold may enjoy a Santa rally for the 7th year in a row

12 Dec 2023: Video - Investing in Uranium

1 Dec 2023: Commodity weekly: Tight supply risks boost copper; OPEC+ struggles to control crude

30 Nov 2023: Precious metals take top spot for a second month

23 Nov 2023: A nervous crude oil market awaits OPEC's next move

23 Nov 2023: Podcast: Will Santa deliver another golden gift

22 Nov 2023: Will gold and silver see another Santa rally?

17 Nov 2023: Commodity weekly: Crude overshoots; silver the comeback kid

16 Nov 2023: Podcast: Silver comeback, watch OPEC as crude oil slides lower

16 Nov 2023: Crude oil weakness adds focus to upcoming OPEC meeting

15 Nov 2023: Soft CPI lifts gold and beaten down silver and platinum

12 Nov 2023: Copper supported by green transformation demand and peak rate speculation

10 Nov 2023: Commodity weekly: Crude oil risks overshooting the downside

Previous "Commitment of Traders" articles

18 Dec 2023: COT: Crude long hits 12-year low ahead of FOMC bounce

11 Dec 2023: COT: An underowned commodity sector raising risk of an upside surprise in 2024

4 Dec 2023: COT: Speculators add further fuel to gold rally

20 Nov 2023: COT: Crude selling slows, grains in demand

14 Nov 2023: COT: Crude long slumps; agriculture sector in demand