Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

AI has been the defining market theme of the past two years — but even powerful trends can experience fatigue.

With the AI-heavy tech sector slipping this month, while healthcare, materials, financials and energy lead the S&P 500, many investors are asking a simple question:

“How do I stay invested in the long-term AI story without being too exposed to short-term swings?”

Below is a clear explainer of what investors are doing today, why these approaches are gaining traction, and the risks to keep in mind.

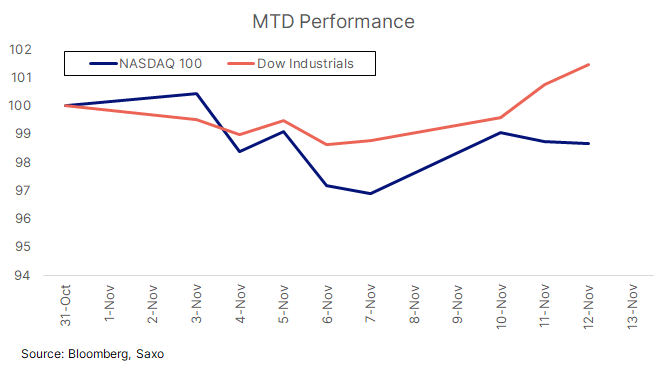

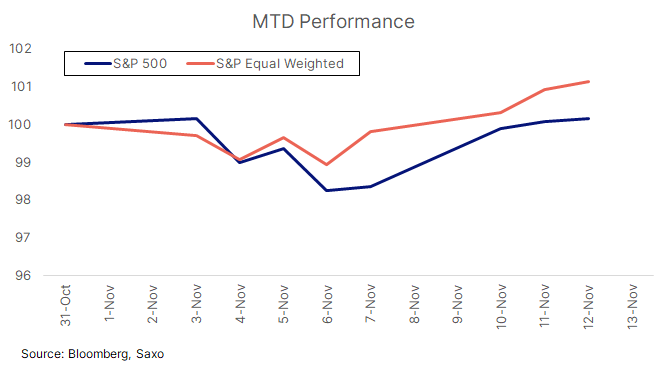

With the Nasdaq 100 down 1.3% MTD and the Dow up around 2%, investors are increasingly rotating into parts of the market with more earnings stability and less sensitivity to AI-driven sentiment.

Where flows are going

This month’s strongest performers include:

Why these sectors attract flows

These areas tend to offer:

The idea behind the rotation

Instead of exiting tech, investors are balancing AI-heavy portfolios with sectors that have clearer demand drivers, more predictable fundamentals, and valuations that are not stretched.

Risks to consider

Some investors are hedging AI exposure via how the portfolio is built, not what it holds:

Risks

Not all tech is experiencing the same valuation pressure. Investors are selectively rotating within tech rather than abandoning it.

Investors are rotating into areas with clearer earnings and less AI hype, such as:

These segments offer a way to stay connected to structural trends — digitalisation, capex cycles, healthcare innovation, and power demand — without the valuation risk sitting in a few AI megacaps.

Risks

Gold and silver remain popular hedges when high-valuation sectors see turbulence.

Why they’re used

Risks

These strategies help manage volatility while staying invested in long-term themes.

Risks

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy