Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

How long-term investors can use covered calls and cash-secured puts to make portfolio decisions more deliberate

For many long-term investors, options can seem like a different world. They are often associated with speculation, leverage, and fast trading. That image is not completely unfair, but it is also incomplete.

Used carefully, some options strategies can help shareholders make clearer decisions around shares they already own or would be willing to buy. Two of the simplest examples are covered calls and cash-secured puts.

A covered call can help an investor receive premium on shares they already own. A cash-secured put can help an investor receive premium while waiting to buy shares at a lower price. Neither strategy removes risk. Both require the investor to accept a clear obligation.

The move from shareholder to options user is therefore not about becoming more aggressive. It is about becoming more deliberate.

Most investors understand shares. You buy part of a company, accept that the price will move up and down, and hope the value rises over time.

Options are different. They are contracts linked to shares, with a fixed expiry date and a fixed price called the strike price. They also involve a premium, which is the money paid or received for the option.

For long-term investors, options can help define future decisions: the price where you may be willing to sell, buy, or take risk.

Shares answer the question: “What do I want to own?” Options add a second question: “At what price am I willing to act?”

The safest starting point is not a random options trade. It is a share you already know well.

If you own 100 shares of a company, you may be able to sell a covered call. This means selling a call option against shares you already hold in exchange for premium upfront.

Because you already own the shares, the call is “covered”. That does not make the strategy risk-free, but it means the obligation is linked to shares already in your portfolio.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it's crucial to make informed decisions.

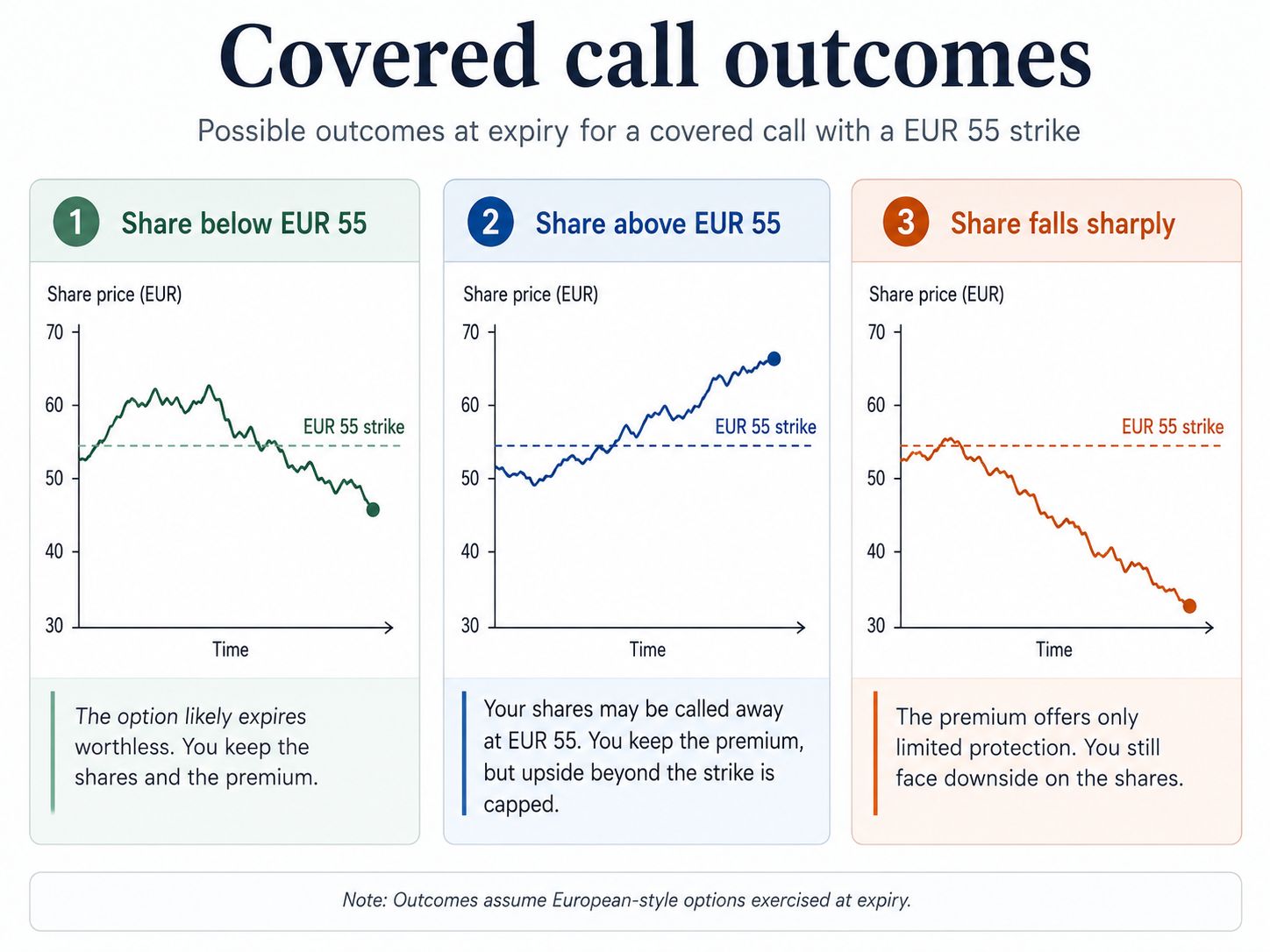

Imagine you own 100 shares of a company trading at EUR 50. You like the company, but you would be comfortable selling if the share price reached EUR 55.

You sell a call option with a EUR 55 strike price and receive EUR 1 per share. Because one standard equity option contract usually represents 100 shares, that means you receive EUR 100 before costs.

There are three broad outcomes at expiry.

Covered call outcomes depend on where the share price is at expiry

| Share price at expiry | What happens | What it means for the investor |

|---|---|---|

| Below EUR 55 | The call expires worthless | You keep the shares and the EUR 100 premium before costs |

| Above EUR 55 | You may have to sell at EUR 55 | You keep the premium, but your upside above EUR 55 is capped |

| Well below EUR 50 | You keep the premium, but the shares fall | The premium softens the fall, but does not remove share price risk |

This is the main trade-off. A covered call does not remove the risk of owning shares. It exchanges some future upside for premium today.

If the share price rises above the strike price, your shares may be called away. If you no longer want to sell, you may be able to buy back the option or roll it to a later expiry and higher strike, but that can cost money and add complexity.

For long-term investors, the rule is simple: only sell a covered call at a price where you would be comfortable selling the shares.

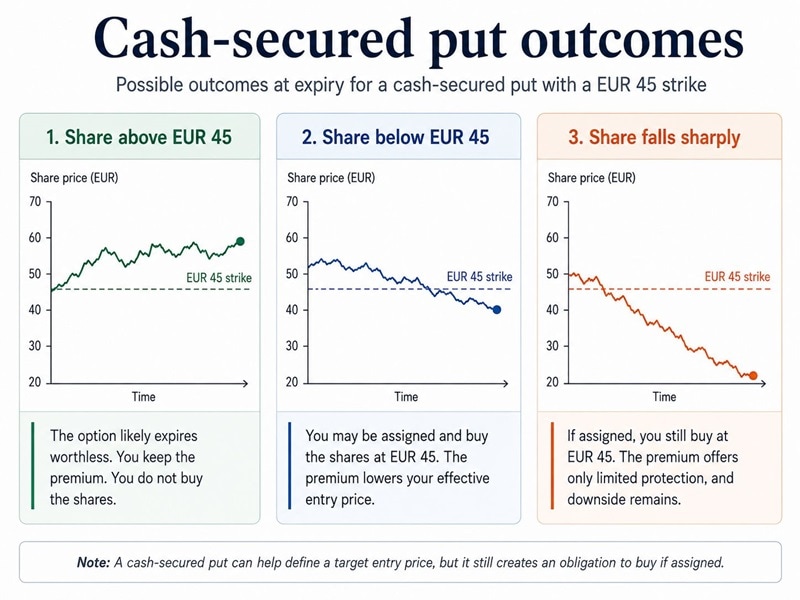

A cash-secured put starts from the opposite situation. Instead of already owning the shares, you would like to buy them at a lower price.

Imagine a share is trading at EUR 50. You like the company, but you would rather buy at EUR 45. You sell a put option with a EUR 45 strike price and receive EUR 1 per share, or EUR 100 before costs.

A put option gives the buyer the right to sell shares to you at the strike price. By selling the put, you accept the obligation to buy 100 shares at EUR 45 if assigned. Because the put is cash-secured, you keep enough cash available to pay for those shares.

Again, there are three broad outcomes.

| Share price at expiry | What happens | What it means for the investor |

|---|---|---|

| Above EUR 45 | The put expires worthless | You keep the EUR 100 premium before costs |

| Below EUR 45 | You may have to buy 100 shares at EUR 45 | Your effective purchase price is EUR 44 before costs |

| Well below EUR 45 | You still may have to buy at EUR 45 | You face losses like any investor who buys shares above the market price |

A cash-secured put can be useful if you already want to own the shares. It is not a safe way to collect income on a company you would never want to buy.

The most useful options users are not necessarily the most aggressive investors. Often, they are the most disciplined.

Covered calls and cash-secured puts force investors to define decisions earlier: what price they would sell at, what price they would buy at, and what risks they are willing to accept.

That is where options can support a long-term investment approach. They can help investors make decisions before emotions take over.

Before placing a first options trade, the investor should be able to answer these questions clearly:

If the answer to any of these questions is unclear, the trade is not ready. That is not a failure. It is risk management doing its job.

Moving from shareholder to options user does not mean abandoning a long-term mindset. Done carefully, it can mean adding structure around shares you already understand.

Covered calls can help investors receive premium while setting a possible sale price. Cash-secured puts can help investors receive premium while setting a possible purchase price. Both strategies can be useful, but only when the investor understands the obligation.

The premium is never free money. It is compensation for accepting a trade-off.

For long-term investors, that is the right way to think about options. Not as shortcuts. Not as speculation dressed up as income. But as tools that can make portfolio decisions clearer, more disciplined, and easier to plan before the market tests your patience.

| Related articles/content |

|---|

| Alphabet after earnings - how a covered call can help investors manage a strong rally | 30 Apr 2026 Tesla shares after earnings could a covered call make sense | 27 Apr 2026 A structured way to buy IWDA at a lower price using options | 20 Mar 2026 How to improve the yield on a long-term IWDA holdings | 12 Mar 2026 How to use a collar to protect stock gains - a Tesla case study | 20 Feb 2026 Palantir after earnings - using options to define a potential entry price | 4 Feb 2026 Golds pullback - thinking beyond buy or sell | 3 Feb 2026 Why options got so popular in recent years | 28 Jan 2026 Netflix earnings - using a cash-secured put to set a lower entry price | 16 Jan 2026 Micron covered call - harvesting extra income after a strong rally | 13 Jan 2026 The Venezuela oil shock - Trading the reconstruction without chasing the hype | 6 Jan 2026 |

| More from the author |

|---|

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist