Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

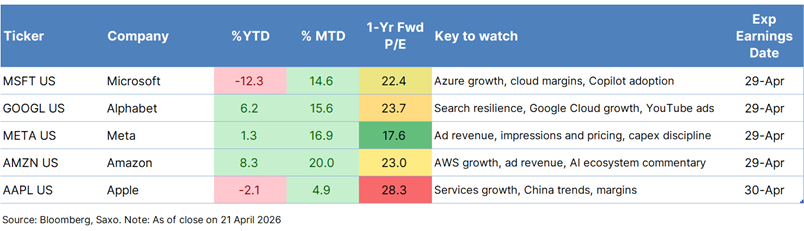

This is the next big test for the AI trade. Five of the Magnificent 7 report within two days, with Microsoft, Alphabet, Meta, and Amazon on 29 April 2026, and Apple on 30 April 2026.

The debate has shifted from overbuilding to returns. Earlier concerns around excessive AI data-centre buildout have eased, but investors now want proof that capex is translating into revenue, margins, and monetisation.

The bar is different for each name. Microsoft and Amazon need to prove cloud and AI demand are still accelerating, Alphabet and Meta need clearer monetisation, and Apple needs to defend its premium with resilience rather than hype.

The AI story is entering a more demanding phase. Earlier this year, investors worried hyperscalers were building too much AI infrastructure, too quickly, with capex rising sharply and the revenue flywheel still unclear. That tone has shifted. AI stocks have regained momentum into first-quarter earnings as overbuilding fears have eased, compute shortages remain real, and newer model momentum has helped revive confidence in demand.

This earnings week matters because the market is no longer rewarding AI ambition alone. It now wants evidence that spending is still producing durable growth, stronger earnings, and clearer returns on investment. The four hyperscalers alone are expected to spend about $645 billion in 2026, up roughly 56% from a year earlier. Investors can still forgive big spending. They may be far less willing to forgive vague spending.

Date of reporting: 29 April 2026

EPS expected: about $4.04, up roughly 17% year-on-year

Revenue expected: about $81.4 billion, up roughly 16% year-on-year

Capex: Microsoft is on track to spend close to $146 billion on AI and cloud infrastructure in fiscal 2026, among the highest across hyperscalers, with expectations for fiscal 2027 capex moving closer to $170 billion. That leaves little room for vague messaging. The market will want reassurance that this level of investment is still being matched by demand, monetisation, and operating leverage.

What to watch: Microsoft remains the market’s cleanest AI execution story, but after lagging peers it now needs to show that heavy investment is producing visible commercial traction.

Azure: Intelligent Cloud revenue is expected at about $34.2 billion, up 28% y/y, with Azure growth around 38%. Healthy cloud migrations and strong AI spending remain the key supports. AI contribution is expected at about 21.4%.

Cloud margins: Microsoft Cloud gross margin is expected at 66.23%, down from 69% in Q3 FY2025, reinforcing the view that this phase of AI growth remains infrastructure-heavy.

Commercial remaining performance obligation: This remains a key forward-looking demand indicator as Microsoft scales spending aggressively.

Copilot: Monetisation may be improving sequentially, but adoption still looks challenging. The question is whether Copilot is becoming meaningful commercial traction rather than just strategic narrative.

Stock price and valuation view: Microsoft has been the worst performer among the hyperscalers year-to-date. That leaves the stock looking less crowded than peers, but at roughly 22x forward earnings, it is not cheap enough to ignore execution risk. A strong Azure print and improving Copilot traction would reinforce the case that Microsoft remains one of the market’s highest-quality AI compounders.

Bull case: Azure growth lands at or above the high end of expectations, AI contribution continues to rise, and Copilot monetisation shows clearer progress alongside confident commentary on demand.

Bear case: Azure growth merely meets expectations, Copilot adoption remains sluggish, and capex stays very heavy, reviving concern that spending is running ahead of monetisation.

Date of reporting: 29 April 2026

Adjusted EPS expected: about $2.83

Revenue expected: about $107 billion, up roughly 11% year-on-year

Capex: Alphabet’s spending plans remain one of the key debates around the stock. The current expectation is that management maintains its FY2026 capex forecast of $175-$185 billion, with limited forward commentary on FY2027. Even so, Bloomberg estimates point to capex moving closer to $200 billion in FY2027, which shows why investors will remain highly sensitive to any signal on duration, discipline, and expected returns. The market has become more comfortable with elevated AI investment, but only because Google Cloud momentum has improved and the broader monetisation story is starting to look more credible.

What to watch: Alphabet now needs to show it is becoming a broader AI platform story without damaging the profitability of Search.

Search: Revenue is expected at about $59 billion, up 16% y/y, with a modest deceleration from the prior quarter.

Google Cloud Platform: Likely the standout metric, with growth potentially in the 50% range y/y, driven by broader AI workloads.

YouTube and advertising: Revenue is expected at about $10 billion, up 12% y/y, supported by healthy ad demand.

Margins and AI returns: Rising capex means investors will keep watching whether monetisation is visible enough to preserve operating discipline.

Stock price and valuation view: Alphabet increasingly looks like a catch-up AI trade. There is room for further re-rating if management shows AI is widening the franchise rather than just defending it. But that means the quarter needs to deliver more than a clean beat.

Bull case: Google Cloud surprises to the upside, Search remains resilient, and management shows confidence that AI is supporting growth rather than simply increasing costs.

Bear case: Search softens, capex rises further, or Cloud growth is not strong enough to convince investors that returns on AI spending are improving.

Date of reporting: 29 April 2026

Adjusted EPS expected: about $7.51

Revenue expected: about $55.5 billion, up roughly 31% year-on-year

Capex: Meta remains one of the most aggressive AI spenders in the group. Its 2026 capex guidance stands at $115-$135 billion, while consensus for 2027 is around $142 billion. Investors have largely accepted that because the core advertising machine has continued to generate strong cash flow. The debate now is less about whether Meta should invest heavily, and more about whether the pace of spending remains justified by monetisation, engagement gains, and margin resilience.

What to watch: Meta is the clearest test of whether the market still rewards aggressive AI spending when the underlying business is already highly profitable.

Ad revenue and Family of Apps: Ad revenue is expected at about $54 billion, up 30% y/y, while Family of Apps revenue is expected at about $55 billion, up 31% y/y.

Impressions and pricing: Ad impressions are expected to rise 16%, while average price per ad is expected to rise 12%. That points to both higher volume and stronger monetisation.

AI model momentum: Meta announced Muse Spark on 8 April 2026. Investors will want to hear how this feeds into engagement, targeting, and monetisation.

Reality Labs and spending discipline: The question is not just capex size, but whether management sounds disciplined on the overall envelope.

Margins: Investors will watch whether ad strength is still enough to fund AI investment without too much pressure on profitability.

Stock price and valuation view: Meta has held up relatively well, with the stock up about 1.3% year-to-date, but it has not seen the same rerating as some of the other hyperscalers. That leaves an interesting setup into earnings. At roughly 17x forward earnings, Meta screens as notably cheaper than peers, with the other hyperscalers generally trading at more than 22x forward earnings. That lower valuation gives investors some cushion, but it also raises the bar for management to show that strong advertising cash flows and AI monetisation can continue to justify heavy spending. If the company can deliver on growth while sounding disciplined on capex, the stock still has room to close some of that valuation gap. If that balance starts to wobble, the market could quickly move from rewarding ambition to penalising excess.

Bull case: Advertising revenue remains strong, impressions and pricing both stay supportive, and management frames AI spending as directly supportive of ad monetisation, engagement, and product momentum.

Bear case: Another step-up in capex or vague commentary around returns revives concern that Meta’s spending ambitions are outrunning near-term earnings visibility.

Date of reporting: 29 April 2026

Adjusted EPS expected: about $2.11

Revenue expected: about $177.2 billion, up roughly 14% year-on-year

Capex: Amazon’s investment cycle has become much more central to the stock’s narrative as AWS and the broader AI infrastructure ecosystem take on greater importance. Amazon is expected to reiterate its full-year 2026 capex guide of $200 billion, which would make it the largest spender among the AI hyperscalers. Consensus for full-year 2026 capex stands at about $195.9 billion, while Bloomberg consensus points to roughly $209 billion in 2027. On 21 April 2026, Amazon also announced an additional $5 billion investment in Anthropic, with potential for $20 billion more over time, underscoring how quickly enterprise AI demand is scaling. The market has been comfortable backing that buildout because AWS remains one of the clearest beneficiaries of rising AI demand. But comfort is conditional. Heavy capex still needs to be matched by visible acceleration in cloud growth and healthy margins.

What to watch: Amazon may be the most important read-through for the broader AI infrastructure trade because AWS sits at the centre of enterprise and developer demand for compute.

AWS: Revenue is estimated at about $36.6 billion, up 25% y/y in constant currency, driven by robust AI demand, increased Claude usage, and expanded cloud commitments.

Advertising Services: Revenue is estimated at about $16.9 billion, up 20.8% y/y in constant currency.

Retail and operating discipline: Investors will watch whether retail margins hold up as Amazon balances core commerce and AI-related investment.

AI ecosystem and commentary: The market will want reassurance that Amazon is not just spending to keep pace, but building an ecosystem that supports durable revenue growth.

Stock price and valuation view: Amazon has been the clear momentum leader in the group, with the stock up about 20% month-to-date and 8% year-to-date, making it the strongest performer among the hyperscalers. That strength reflects growing confidence in AWS, the AI infrastructure story, and the broader Anthropic ecosystem. At roughly 23x forward earnings, the stock is still carrying a premium, which means expectations are not low. If management delivers confidence on cloud acceleration and the broader AI ecosystem, Amazon can continue to justify that premium. But if AWS is merely in line while capex remains very heavy, the market may start asking harder questions about whether Amazon is investing like a winner but reporting like a laggard.

Bull case: AWS growth meets or exceeds elevated expectations, advertising remains strong, margins stay healthy, and management commentary reinforces the view that AI demand is driving durable cloud growth.

Bear case: Heavy spending continues but AWS growth is only in line, creating concern that Amazon is investing aggressively without enough acceleration to justify it.

Date of reporting: 30 April 2026

EPS expected: about $1.96, up roughly 18% year-on-year

Revenue expected: about $109.3 billion, up roughly 15% year-on-year

Capex: Apple is the least capex-intensive AI story in this group, which makes it a useful contrast. Capital expenditure is estimated at about $13.5 billion in fiscal 2026 and $15.4 billion in fiscal 2027, far below the hyperscalers. Investors are not looking to Apple for a hyperscaler-style infrastructure buildout. Instead, the focus is on whether Apple can maintain earnings durability, service-led monetisation, and product ecosystem resilience while the market increasingly rewards AI-linked growth elsewhere.

What to watch: Apple is the least direct AI infrastructure trade of the group, so the focus is less on AI hype and more on resilience.

Services: Revenue is estimated at about $30.4 billion, up 14%.

iPhone: Still the key driver of sentiment, especially around demand and upgrade behaviour.

Mac: Mac sales could surprise positively, helped by stronger Mac Mini demand.

Greater China: Investors will want to know whether recent improvement is sustainable.

Margins and product mix: Apple does not need explosive growth, but it does need to defend premium profitability.

Stock price and valuation view: Apple is not the cleanest way to play the AI enthusiasm driving the rest of the group, but it remains one of the market’s clearest durability stories. Even so, the stock is still down about 2% year-to-date, which suggests investors are not fully convinced that steadiness alone is enough in a market that is rewarding more direct AI exposure. At roughly 28x forward earnings, Apple is also trading at a richer multiple than most of its mega-cap peers. That means the bar is not low. The company does not need a dramatic AI reveal next week, but it does need to remind investors why it still deserves that premium as a mega-cap compounder. If Services remains strong, margins hold, and China looks more stable, that may be enough. But if the forward message feels too incremental, the stock risks looking expensive as well as unexciting.

Bull case: Services growth remains firm, margins hold up, and management signals that China trends are improving rather than merely bouncing.

Bear case: The quarter is acceptable but the forward message feels incremental, especially if Services growth slows or China remains uneven.

The key question is whether demand for AI products and services is still strong enough to justify the capex wave now rolling through Big Tech. Microsoft and Amazon will shape confidence in cloud and AI infrastructure. Alphabet and Meta will test whether AI spending is improving monetisation rather than just inflating costs. Apple will show whether mega-cap resilience still holds even outside the pure AI buildout story.

In short, the market can still forgive big spending. It may be far less willing to forgive vague spending.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy