Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Summary: Our Q2 outlook argues that investors should stop thinking in binaries. AI remains a powerful long-term theme, but geopolitics, energy disruption, and supply-chain stress are making markets more selective and less forgiving. The key message is to stay exposed to structural growth while reducing concentration risk and building resilience through broader diversification, real assets, quality income, and sectors tied to energy, infrastructure, and security.

Markets are entering Q2 with two forces pulling at once. The Iran conflict is the macro shock dominating headlines, while AI remains the structural trend shaping capital spending, policy priorities, and long-term market leadership. For investors, the challenge is not choosing one over the other, but understanding how to position for both.

The geopolitical shock matters beyond oil as a sustained energy disruption can feed into inflation expectations, bond yields, rate-cut assumptions, and broader risk appetite. The bigger picture is that AI is still one of the most important investment cycles of this decade, but conviction around it is no longer unconditional. It remains policy-backed, capex-driven, and tied to national competitiveness, but a sustained energy shock would make the path more uneven by raising power costs, tightening financial conditions, and forcing investors to ask harder questions about monetisation, balance-sheet strength, and how much capex can still be defended if growth slows.

In other words, the geopolitical shock may not end the AI buildout, but it can make it more energy-sensitive, more selective, and less forgiving for the parts of the theme that rely most on cheap capital and distant promises.

That is the real task for investors in Q2. Staying exposed to structural growth, but reducing dependence on a single macro outcome.

For long-term investors, the first rule is still not to panic. Geopolitical shocks are rarely a good reason to abandon a long-term plan, and the cost of stepping out can be high. However, understanding whether the portfolio has drifted into hidden concentration is key.

That matters now because many portfolios look diversified on paper but are less diversified in practice, with heavy exposure to a narrow cluster of AI winners, too much dependence on one region, and too much reliance on bonds as the only line of defence.

For safety and income in a world of volatile inflation and rates, bonds still matter but they may not be enough on their own. Therefore, it becomes necessary to make sure the portfolio is not relying on one type of defence.

For investors, the most useful response is not to trade every twist in the conflict. It is to ask whether diversification still works. A simple long-term investor checklist is:

If the answer to most of those questions is no, that probably means the portfolio deserves a rebalance.

The Iran conflict matters to markets first through energy, but the investment impact no longer stops at the oil price. Disruption to shipping lanes, insurance costs, freight routes, and intermediate inputs means the shock increasingly looks like a supply-chain and cost shock as well, and can start to hit margins, delivery times, and inflation more broadly.

For investors, this changes the way the shock should be read.

That broadening matters for portfolio strategy.

The most useful way to think about the Iran conflict for investors is using three scenarios as different tests of portfolio resilience.

A de-escalation outcome would allow markets to move away from pure defensiveness and back toward breadth. If the oil risk premium fades, growth fears ease, inflation pressure softens, and supply disruptions start to clear, broader equities can recover.

Positioning in that setting should favour:

A prolonged disruption is more uncomfortable because it keeps oil, freight, and input costs elevated at the same time. That leaves markets dealing with slower growth, stickier inflation, and more volatile bond pricing.

Positioning in that setting should lean toward balance:

The tail-risk scenario is the one that most clearly shifts the market from positioning for opportunity to positioning for resilience. In that case, oil would likely move into the danger zone for both growth and inflation, and stagflation fears could come to the forefront. Bloomberg Intelligence analysis has shown that oil above $100 has historically been the danger zone for equities, with S&P 500 profitability slipping as energy costs bite into margins.

Positioning there should focus on:

If Iran is the macro shock, AI remains the structural trend, but that no longer means the market has the same conviction in every part of the story.

What changed in Q1 is not the existence of the theme, but the willingness of investors to fund it unquestioningly. The easy phase of the trade is over. Investors are asking harder questions about valuations, earnings conversion, competitive moats, energy intensity, and whether AI makes some software businesses stronger while making others more vulnerable. They are also asking a harder macro question: if energy costs stay high and financial conditions remain tight, which parts of the AI buildout still get funded and which parts begin to look easier to delay, shrink, or question?

That is why the more useful distinction now is not between AI winners and losers in one broad sense, but between:

For long-term investors, the stronger strategy may be to move away from narrow concentration and toward broader exposure across the AI value chain, while recognising that not all parts of that chain deserve the same level of conviction.

That means looking beyond the headline winners to areas such as:

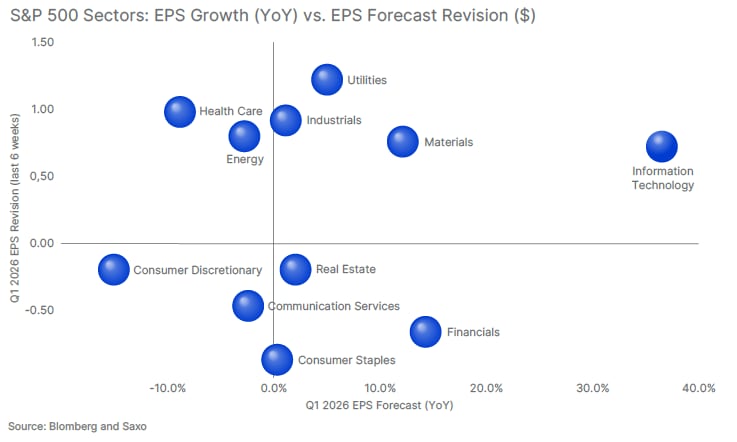

Earnings expectations still support the structural AI case. S&P 500 EPS growth is still expected to improve into Q2, and technology remains one of the strongest earnings engines in the market. Earnings revisions have also held up better in technology. But strong sector-level earnings expectations also do not remove the risk that parts of the AI theme are over-owned, over-promised, or more exposed to an energy and funding shock than the market had priced a quarter ago. That tells investors two things at once: the earnings engine behind AI has not disappeared, but leadership remains narrow enough, and conviction fragile enough, that concentration risk is still real.

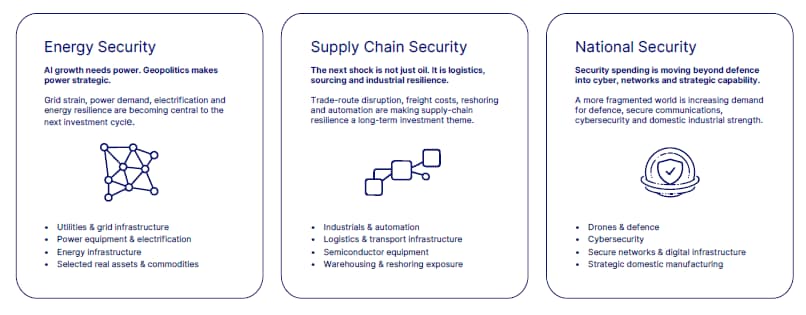

The overlap between AI and geopolitics is where the most interesting long-term investment implications are starting to emerge. AI is increasing demand for power, chips, data centres, grids, and secure digital infrastructure. Geopolitics is increasing the premium on energy resilience, trusted supply chains, and domestic strategic capability. Put together, they are creating a market shaped less by convenience and more by security.

AI is energy-hungry, and geopolitics is making energy more strategic.

This theme maps most clearly to:

Positioning here is about owning the physical buildout that supports both AI demand and a more security-conscious world.

The Iran shock is a reminder that logistics, shipping, sourcing, and intermediate inputs can quickly become market issues. At the same time, AI and industrial policy are pushing countries and companies to shorten, diversify, or harden supply chains.

This theme maps most clearly to:

Positioning here is about favouring businesses tied to resilience, localisation, and operational efficiency rather than just global volume growth.

Geopolitics is not only raising demand for military spending. It is also lifting demand for cybersecurity, secure communications, strategic technology, and domestic industrial capability.

This theme maps most clearly to:

Positioning here is about recognising that national security spending is broadening beyond traditional defence and increasingly overlaps with technology and infrastructure.

This is also why real assets deserve more attention in investor portfolios. They are not only a hedge against geopolitical shocks. They are part of the structural response to a more energy-hungry, supply-constrained, and security-conscious world.

From an investment strategy perspective, real assets can do two jobs at once:

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy