Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

Summary: When markets turn ugly, emotions can become more dangerous than fundamentals. History shows that investors who panic, sell, and miss the rebound often do more damage to returns than the selloff itself. That is why discipline matters most when markets feel hardest to trust.

Days like today test investors twice. First, through falling prices. Second, through the urge to do something dramatic.

That second test is often the more dangerous one.

In sharp selloffs, the biggest risk is often not the market itself, but the investor’s emotional response to it.

The hardest truth in investing is that long-term returns are not usually destroyed by one bad selloff. They are damaged when fear turns volatility into bad decisions.

DALBAR’s latest investor behaviour study showed that the average equity investor earned 16% in 2024, far below the S&P 500’s 23%.

That gap is a reminder that investors often underperform not because markets fail them, but because emotions do.

Morningstar’s “Mind the Gap” research reaches a similar conclusion. The gap between investment returns and investor returns comes from the timing of cash flows, in other words, when investors buy, sell, add, or pull money. In volatile periods, that behaviour gap tends to become more costly.

This is why days like today are more about managing emotions than remodelling portfolios.

The temptation in sharp selloffs is to move to safety and wait for clarity. The problem is that markets do not ring a bell when fear peaks, and the rebound often comes when sentiment still feels awful.

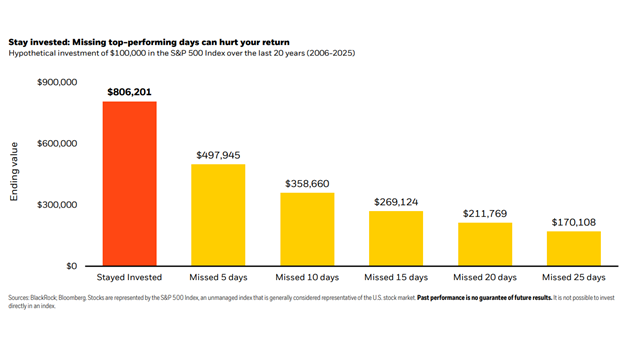

J.P. Morgan gives a concrete stat: over the past 20 years, seven of the stock market’s 10 best days occurred within 15 days of one of the 10 worst days.

The graph from Blackrock below shows how a hypothetical $100,000 investment in stocks would have been affected by missing the market’s top-performing days over the 20-year period from January 1, 2006 to December 31, 2025. For example, an individual who remained invested for the entire time period would have accumulated $806,201, while an investor who missed just five of the top-performing days during that period would have accumulated only $497,945.

That does not mean investors should ignore risk. It means they should respect the difference between risk management and panic management. If the portfolio was built with a time horizon, diversification, and realistic liquidity needs in mind, then a chaotic day is not automatically a signal to abandon it. More often, it is a reminder to stick to process.

In markets like this, discipline is the real hedge. Portfolios can recover from volatility. Emotional decisions are much harder to undo.

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy