Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

China tech’s comeback

As investors question the cost of the US AI buildout, China tech is gaining attention for cheaper models, open-source adoption and a more efficiency-led AI strategy.

China tech is starting to outperform again. But this is not simply a “China recovery” trade.

The more interesting story is that the AI narrative itself is changing.

For the last two years, AI leadership has largely been defined by scale: who has the most chips, the biggest data centres, the deepest hyperscaler balance sheets and the highest capex plans. That story still favours the US.

But the next phase of AI may be defined by a different question: who can deliver useful AI at the lowest cost?

That is where China tech is becoming harder to ignore.

China’s macro picture is still uneven. Consumer confidence remains fragile, the property sector is not fully healed, and policy support has been gradual rather than forceful.

So why are investors looking at China tech again?

Because the market is starting to separate China macro risk from China AI potential.

Chinese internet names are no longer being viewed only as e-commerce, advertising, gaming or social media platforms. They are increasingly being seen as part of a broader domestic AI ecosystem, including:

This matters because investors are looking for AI exposure beyond the crowded US semiconductor and hyperscaler trade.

China tech offers that — but with a different risk profile.

The stronger China AI argument is no longer just “China is investing in AI.” It is that Chinese AI models are being used more widely — including by US companies.

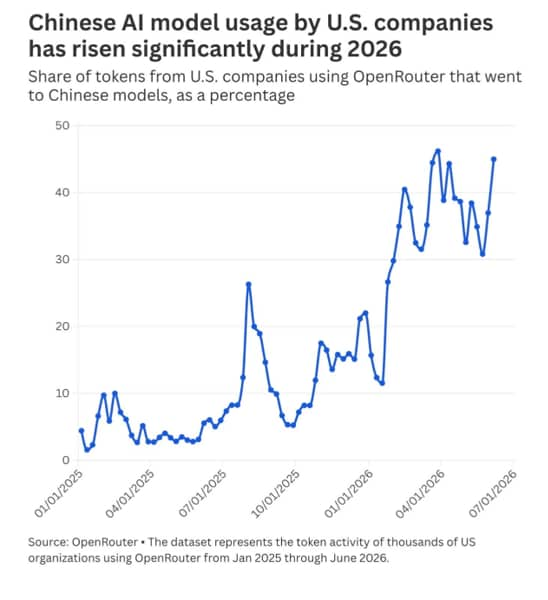

A recent OpenRouter chart shows that the share of tokens from US companies using OpenRouter that went to Chinese models has risen significantly through 2026. Chinese models have accounted for more than 30% of weekly token usage by US companies since Feb. 8, peaking at 46%. That compares with an average of 11% over the previous 12 months and just 4.5% in the first half of 2025.

That is important because OpenRouter is not just a benchmark leaderboard. It is a usage signal. It shows where developers and applications are actually routing traffic.

For investors, this changes the story. China AI is no longer only about policy ambition or domestic substitution. It is starting to show signs of global developer and enterprise adoption.

And developers tend to be pragmatic. They do not choose models because of market narratives. They choose what works, what is cheap, and what can be integrated quickly.

That is exactly where China’s open-source model strategy is becoming important.

The capex comparison is central to the investment case.

Goldman Sachs estimates suggest US hyperscalers — Amazon, Microsoft, Google, Meta and Oracle — could spend around US$764bn in 2026 and US$1.018tn in 2027 on AI-related capex.

China’s leading AI hyperscalers — Alibaba, Tencent, ByteDance and Baidu — are estimated to spend around US$102bn in 2026 and US$123bn in 2027.

In other words, the US may still outspend China by roughly eight times.

At first glance, that looks like a weakness for China. But it is also the heart of the investment case.

The US AI story is about massive infrastructure buildout: chips, power, data centres, memory, cloud capacity and capital intensity.

China’s AI story is more about doing more under constraints: cheaper models, open-source development, lower inference costs and software optimisation.

Put simply:

That distinction matters at a time when investors are asking whether AI returns can keep up with AI spending.

China does not have the same access to the most advanced chips as the US. It also does not have the same hyperscaler capex firepower.

But constraints can sometimes create a different kind of innovation.

China’s AI players have been forced to focus on:

DeepSeek was the first major moment when global investors started to question whether AI leadership had to be purely about brute-force spending.

Its impact was not just about one model. It showed that Chinese AI firms could compete by focusing on efficiency, cost and distribution.

That forced a bigger market question: if a model is good enough at a much lower cost, does every AI winner need to be a mega-cap infrastructure spender?

That question is becoming more relevant as investors worry about AI capex fatigue in the US.

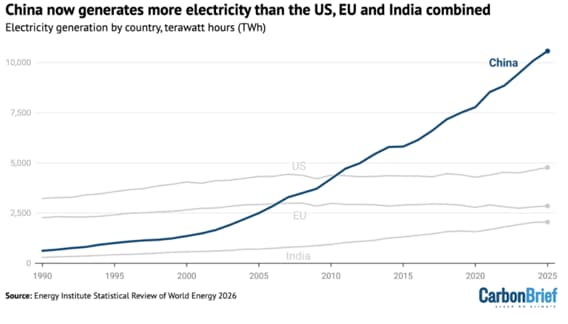

There is another underappreciated reason China tech may be getting more attention: electricity supply.

AI is not only a chip story. It is also becoming a power story. Data centres accounted for around 415 TWh, or 1.5% of global electricity consumption, in 2024, according to the International Energy Agency. The IEA expects data-centre electricity consumption to more than double to around 945 TWh by 2030, with the US accounting for the largest share of the increase, followed by China.

That creates a bottleneck for the US AI trade. The US is already seeing record power demand, driven partly by AI-heavy data centres and electrification. Reuters reported that the US Energy Information Administration expects US power demand to rise from 4,195bn kWh in 2025 to 4,269bn kWh in 2026 and 4,399bn kWh in 2027.

China, by contrast, has a much larger electricity system. The Energy Institute’s Statistical Review noted that China’s electricity generation has surged past 10,500 TWh, more than double US output, which is moving toward 4,800 TWh.

That does not mean China has no power constraints. It still faces regional grid bottlenecks, renewable curtailment issues and a heavy reliance on coal. But from an AI infrastructure perspective, China has one important advantage: it can build power, grids and industrial infrastructure at scale, quickly and with strong state coordination.

For investors, this matters because the AI winners may not only be the companies with the best models. They may also be the ecosystems with enough electricity, cooling, land, chips and infrastructure to run AI cheaply at scale.

In that sense, China’s AI story is not only about cheaper models. It is also about having a power system that may be better able to support large-scale AI deployment.

This is no longer just a DeepSeek story.

The China AI ecosystem is broadening across large platforms and model innovators:

This matters because investors are not only looking at one company or one model. They are starting to see a broader ecosystem.

That makes China tech feel less like a single-name rebound and more like a potential AI basket.

It also helps explain why the rally is happening now. Investors are looking for ways to stay in the AI theme, but without owning only the same crowded US semiconductor, hyperscaler and data-centre trades.

China tech gives investors another route into AI — one that is more focused on efficiency, deployment and lower expectations.

There are three key reasons China tech is getting attention again.

1. The US AI trade is crowded: A lot of good news is already priced into US AI infrastructure, semiconductors and hyperscalers. When expectations are extremely high, even strong earnings may not be enough.

2. China tech is still relatively unloved: Many China internet stocks spent years under pressure from regulation, weak consumption, geopolitics and valuation compression. That means the bar for positive surprises is lower than in US AI.

3. Investors want AI exposure with different risk drivers: China tech is less tied to the same semiconductor, power and data-centre bottlenecks that dominate the US AI trade. That makes it attractive as a rotation candidate.

This does not mean China tech is risk-free. It means it may offer a different way to participate in the AI theme at a time when investors are reassessing concentration risk.

The China tech trade still comes with clear risks.

1. China macro risk remains unresolved: A weaker consumer, property stress and uneven confidence could limit the earnings recovery for internet platforms.

2. Policy risk has not disappeared: China tech has re-rated before, only to be hit by regulatory shifts. Investors will still demand a risk premium.

3. Geopolitical risk could rise again: US-China tech restrictions remain a major overhang, especially around advanced chips, cloud access and model usage.

4. Data-security concerns may limit adoption: Chinese AI models may be used more widely for coding, experimentation and lower-risk workloads, but adoption in regulated industries such as banking, cybersecurity and government could be more limited.

5. China could restrict access to its own AI models: If China limits foreign access to advanced AI technologies, it could reduce one of the biggest advantages of its open-source strategy: global developer adoption.

So the investment case is not that China has no risks. It is that the market may be starting to price China tech for opportunity again, not only for risk.

China tech is not coming back because all the old risks have disappeared. It is coming back because the AI story is broadening.

The first phase of AI belonged to companies that could spend the most. The next phase may also reward companies that can make AI cheaper, more efficient and easier to deploy.

That is where China tech has a real opening.

The US remains the AI spending superpower. It still leads in frontier labs, advanced chips, hyperscaler scale and capital markets.

But China is increasingly becoming the AI efficiency challenger.

And in a market that is starting to question whether AI returns can justify AI spending, that distinction suddenly matters.

China tech may not be the cleanest AI trade. But it may be one of the more interesting ones: cheaper, less crowded and increasingly tied to the next phase of AI adoption.

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist