Macro: It’s all about elections and keeping status quo

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

Head of Commodity Strategy

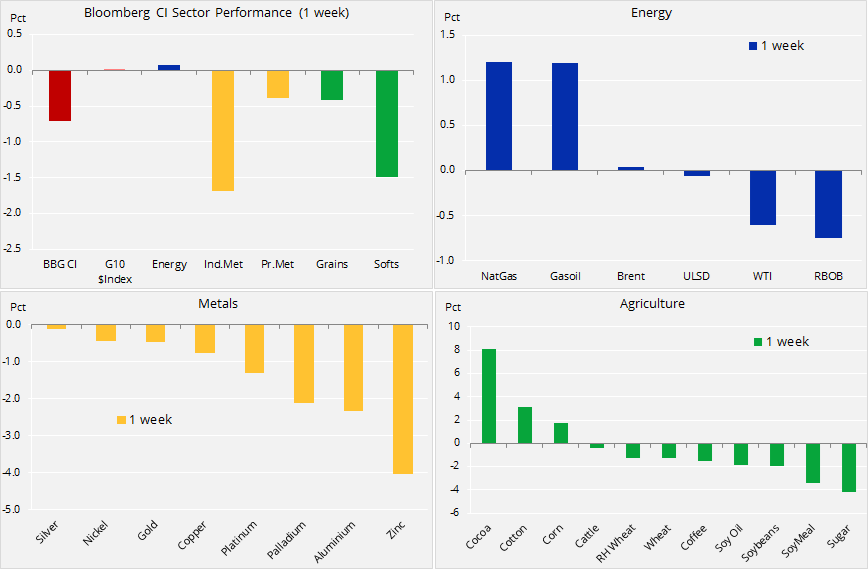

Global trade tensions helped trigger a broad-based retreat across key commodities. The risk of an escalating tit-for-tat trade war could hurt global growth forecasts and subsequently, demand for raw materials. Industrial metals slumped to a 12-week low, oil drifted lower as the focus turned to rising supply focus while profit-taking hit key crops following the recent weather-related surge.

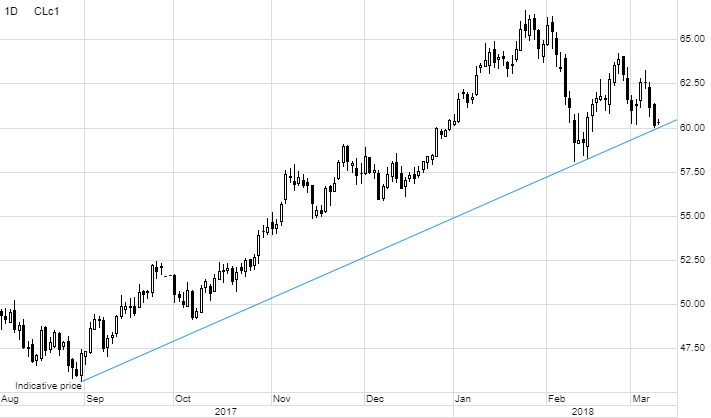

Crude oil traded near the lower end of the range that has emerged since January. While receiving a great deal of directional input from the ebbs and flows of the stock market, a continued elevated bullish sentiment among speculative traders is being supported by robust global demand. However, crude is simultaneously challenged by rising non-Opec supply and now also the aforementioned trade tensions.

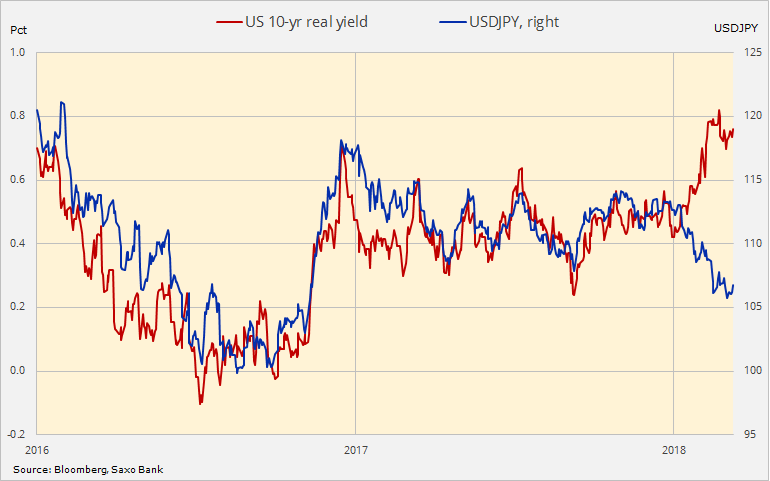

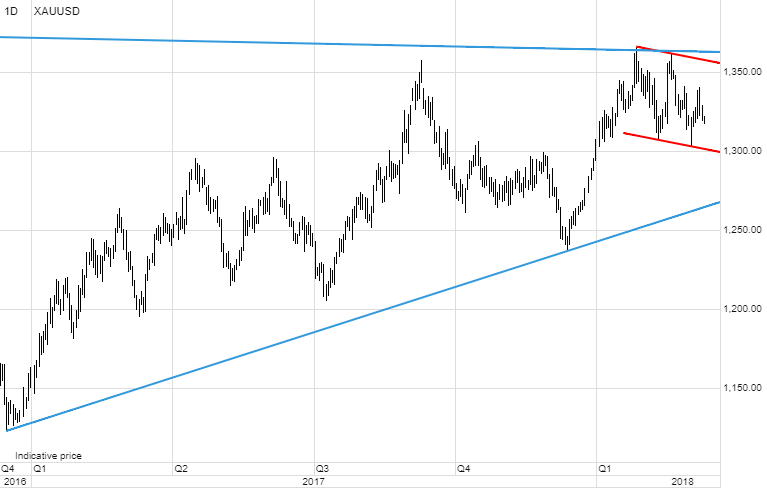

Gold also went looking for support after failing for a second time in two weeks to break above resistance at $1,340/oz. Additional weakness was seen ahead of and after Friday's strong US jobs report and after hopes of easing tensions between the US and North Korea helped send the yen lower against the dollar. A May meeting between Trump and Kim Jong-un could be the breakthrough needed to ease nuclear tensions on the Korean peninsula.

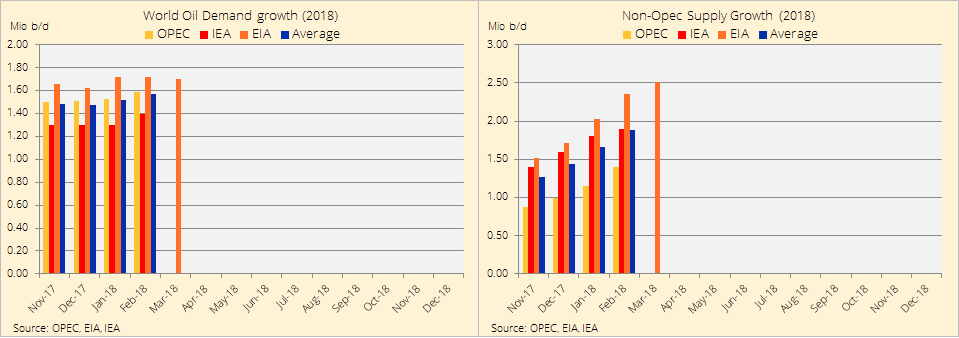

Strong non-Opec oil production growth looks set to challenge Opec and Russia's ability to maintain price stability, at least in the short term. In its latest Short Term Energy Outlook the Energy Information Administration sees US oil production averaging 10.7 million barrels/day in 2018, an increase of 1.4 million b/d from 2017. The IEA added to the unease when it said in its Oil 2018 report that production growth from the United States, Brazil, Canada, and Norway would more than meet global oil demand growth through 2020.

In the week to February 27, hedge funds increased the combined long oil bet in WTI and Brent for the first time in five weeks by 36,000 lots to 1 million lots – this after cutting it by a total of 133,000 lots during the previous four weeks. The dwindling short base led to another rise in the long/short ratio to a record 12.6. This highlights a continued downside risk to oil should the technical and/or fundamental outlook turn less favourable.

The EIA continues to raise 2018 non-Opec supply growth while keeping demand growth steady. Monthly reports from Opec and IEA are due this coming week on March 14 and 15.

Given the recent resilience among speculative investors, they are unlikely to worry about a deeper correction as long as prices stay above $61/barrel on Brent crude oil and $57.50/b on WTI crude. These levels represent the 38.2% correction of the June-January rally and while above the current price action, will be viewed only as a weak correction within a strong uptrend.

For now WTI crude oil has settled into a $60 to $65/b range with outside market events providing most of the input for daily price swings. A close below $60/b carries the risk of an extension to the mentioned key level at $57.50/b.

Gold has settled into range between $1,300/oz. and $1,340/oz. with the negative impact of the recent rise in US real yields being offset by the positive impact of a stronger Japanese yen. Increased stock market volatility has also played its part in recent gold gyrations. Trump's initial tariff announcement sent stocks lower and gold higher only to weaken again as the stock market recovered when a watered-down version was announced.

US real yields – the yield you will earn after inflation – have almost doubled since the beginning of the year. Offsetting this negative development for gold has been the weaker dollar, especially against the Japanese yen.

Adding to the mix was Friday's jobs report, the last before the March 21 Federal Open Market Committee meeting. A Goldilocks report showing strong job growth and lacklustre inflation left the door wide open for a sixth rate hike and potentially also a hiking of the forward guidance. The previous rate hikes in this current cycle which began in December 2015 have so far triggered a repeat pattern of gold weakening ahead of a FOMC meeting only to rise strongly once the rate hike was announced.

A continued rise in rates is unlikely to derail gold's ability to move higher. Not least if higher rates are caused by the wrong kind of inflation, i.e. the sort that is driven by rising prices due to import tariffs instead of demand-based inflation.

We maintain a constructive view on gold, especially given its ability to withstand the recent jump in real yields. Its rangebound nature, however, is likely to continue ahead of the March 21 FOMC meeting with nervousness about the rate hike being offset by the risk of rising global trade tensions.

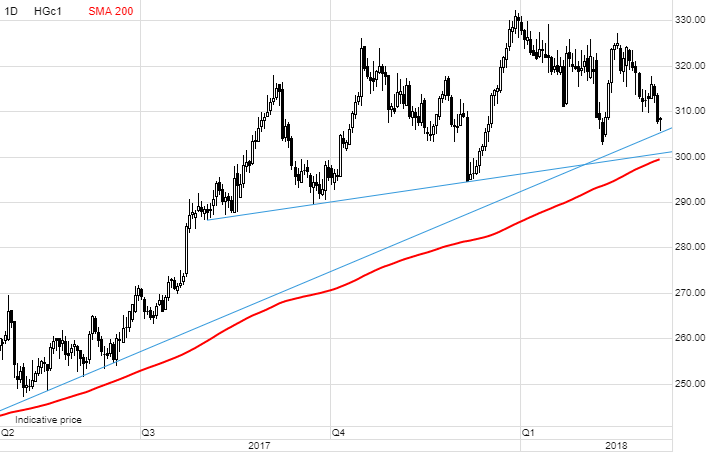

Industrial metals with the exception of nickel are all trading down on the year with the risk of trade wars now adding to the existing nervousness about the short- to medium-term outlook for growth and demand in China. This occurs at a time when China's transition from the old economic model to a new and less commodity-intensive economy could take its toll on demand.

HG Copper's strong surge from the 2016 low has been running out of steam during the past few months with the price struggling to break above resistance at $3.30/lb, the 50% retracement of the 2011 to 2016 selloff. For now the price remains stuck in a range with support just below $3/lb.

HG Copper, first month cont.

Top performers of the week

Natural gas has spent the past few weeks recovering after once again finding support at $2.50/therm. A colder than normal winter has led to robust demand which has helped offset record production.

Cocoa, up 30% year-to-date, surged higher to reach a 16-month high with the Ivory Coast Cocoa Board reported to have oversold the bean as production continues to suffer from drought.

Cotton was supported by unusually strong export demand and an escalating drought in Texas which can cause planting problems. In the latest update on supply and demand from the US Department of Agriculture these developments helped trigger a price-supportive downward revision of US ending stocks.

The DoA report also gave corn a boost from a surprise drop in domestic stocks on rising export demand after dry and hot conditions took a toll on the crop in Argentina, the No. 3 global corn and soy exporter.

The dramatic rally across the grain and soy sectors since mid-January has to a large extent been speculatively driven. During a six-week period from January 16 to February 27, funds went from holding a combined record short across six grain and soy futures of 480,000 lots to a net-long of 250,000 lots.

With so many recently established longs the risk of a correction was high going into the monthly supply and demand report. As a result both wheat and soybeans ran into profit-taking after data proved less supportive than expected.

2024: The wasted year

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

As US economic slowdown hints at a shift away from exceptionalism, USD faces downside with looming Fed cuts. AUD and NZD set to outperform as their rate cuts lag. JPY gains on carry unwind bets and BOJ pivot.

Amid AI and obesity drug excitement, equities see varied prospects: neutral on overvalued US stocks, negative on Japan due to JPY risks, positive on Europe. European defence stocks gain appeal.

With the economic slowdown, quality assets will gain favour, especially sovereign bonds up to 5 years. Central banks' potential rate cuts in Q2 suggest extending duration, despite policy and inflation concerns.

Commodities poised for rebound. The "Year of the Metal" boosts gold and silver, copper awaits rate cuts. Grains may recover, natural gas stabilises. Gold targets $2,300-$2,500/oz, copper's breakout could signal growth.

Markets are driven by election optimism, overshadowing growing debt and liquidity concerns. The 2024 elections loom large, but economic fundamentals and debt issues warrant cautious investment.

As US economic slowdown hints at a shift away from exceptionalism, USD faces downside with looming Fed cuts. AUD and NZD set to outperform as their rate cuts lag. JPY gains on carry unwind bets and BOJ pivot.

Amid AI and obesity drug excitement, equities see varied prospects: neutral on overvalued US stocks, negative on Japan due to JPY risks, positive on Europe. European defence stocks gain appeal.

With the economic slowdown, quality assets will gain favour, especially sovereign bonds up to 5 years. Central banks' potential rate cuts in Q2 suggest extending duration, despite policy and inflation concerns.

Commodities poised for rebound. The "Year of the Metal" boosts gold and silver, copper awaits rate cuts. Grains may recover, natural gas stabilises. Gold targets $2,300-$2,500/oz, copper's breakout could signal growth.