Outrageous Predictions

Révolution Verte en Suisse : un projet de CHF 30 milliards d’ici 2050

Katrin Wagner

Head of Investment Content Switzerland

la Suisse se lance dans une révolution énergétique de CHF 30 milliards d'ici 2050, rivalisant avec l...

Résumé: Oracle shares dropped more than 11% following its earnings release on 10 June 2026. That kind of move creates a very specific question: does a cash-secured put make sense here? This article walks through exactly what the strategy involves, step by step.

This article uses Oracle’s post-earnings situation as a teaching tool. The numbers are real – drawn from the SaxoTrader option chain and order ticket on 11 June 2026. But the purpose is not to say “sell this put.” It is to walk through exactly what a cash-secured put involves, step by step, using a live example where the strategy’s logic is easy to follow.

Oracle Corporation reported its quarterly earnings after the close of trading on 10 June 2026. The market’s reaction was swift: shares fell more than 11% the following session, dropping from a previous close of USD 201.26 to trade near USD 177 on 11 June (at the open). The move pushed the stock well below its 50-day moving average on the daily chart (USD 184.14) and significantly below its 200-day moving average (USD 206.07). The weekly chart adds further context: Oracle had peaked above USD 250 earlier in 2026 before the series of down moves that brought it to today’s level.

Oracle Corporation (ORCL) – weekly (top) and daily (bottom) charts as of 11 June 2026. The stock fell sharply following the earnings release on 10 June, closing near USD 180 after trading above USD 200 earlier in the week. The daily chart shows the price below both the 50-day SMA (USD 184.14) and the 200-day SMA (USD 206.07), with elevated volume on the sell-off. Source: SaxoTrader

What makes this a useful example for explaining the cash-secured put is the combination of two factors: a well-known stock at a sharply lower price, and elevated implied volatility (78.16%) that has widened option premiums significantly. Both conditions are common in the period immediately following an earnings sell-off. The mechanics of the strategy become more concrete when the numbers are this visible.

For the purposes of this article, the question is not whether Oracle is cheap or expensive at USD 177. It is: how does a cash-secured put work, and what does it actually look like when you set one up?

A cash-secured put is an options strategy for investors who want to buy a stock at a lower price than today’s market – and who are willing to be paid while they wait.

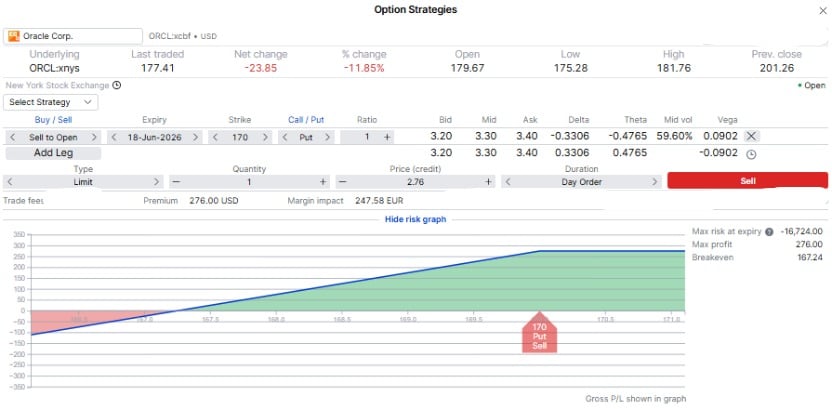

Here is how it works. The investor sells a put option at a strike price below the current share price. The buyer of that put option pays the investor a premium upfront. In return, the investor commits to buying 100 shares at the strike price if the stock is at or below that level at expiry.

The phrase “cash-secured” matters. It means the investor actually sets aside enough cash to buy those 100 shares if assigned. In this example, that is USD 17,000 (100 shares × USD 170 strike). This reserved cash is what makes the strategy more conservative than selling an uncovered – or “naked” – put, where no cash is held in reserve.

If Oracle closes above USD 170 on 18 June 2026, the put expires worthless. The investor keeps the premium and their cash is freed. If Oracle is at or below USD 170 at expiry, the investor is assigned – they buy 100 shares at USD 170, with the premium received reducing their effective entry price to USD 167.24. The downside risk mirrors owning Oracle stock from USD 167.24 downward: the premium softens the entry slightly, but does not protect against a sustained decline after assignment.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

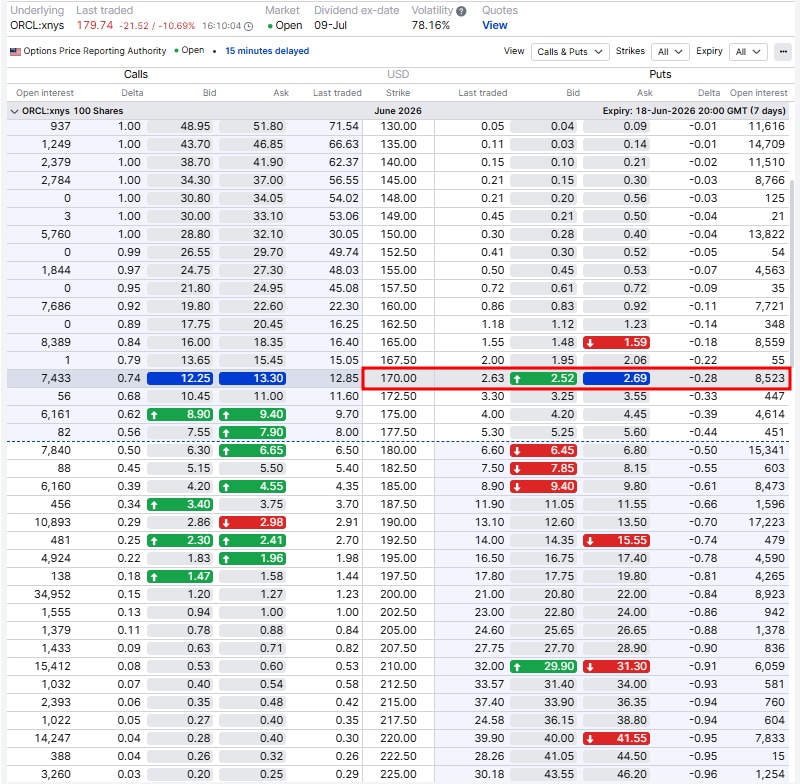

With Oracle trading near USD 177 on 11 June 2026, the 170 put expiring 18 June 2026 serves as the worked example. Here are the key parameters:

A note on execution: the options chain showed a bid of USD 2.63 and ask of USD 2.69 at the time of this example. The USD 2.76 mid-price on the order ticket reflects a slightly earlier snapshot. In practice, use a limit order placed between the bid and mid rather than a market order, and adjust if the market has moved.

Oracle Corporation (ORCL) options chain, 18 June 2026 expiry (7 days). The 170 put is highlighted, showing a bid of USD 2.63 and ask of USD 2.69 at the time of this example. Implied volatility: 78.16%. Data shown with a 15-minute delay. Source: SaxoTrader

The USD 276 premium represents approximately 1.6% of the USD 17,000 cash reserved, over a seven-day period.

More importantly, the numbers make the downside concrete:

| Scenario | Calculation | Result |

|---|---|---|

| Cash reserved | 100 × USD 170 | USD 17,000 |

| Effective entry if assigned | USD 170 − USD 2.76 | USD 167.24 per share |

| Value if assigned and ORCL falls to USD 140 | 100 × USD 140 | USD 14,000 |

| Effective cost of 100 shares | 100 × USD 167.24 | USD 16,724 |

| Paper loss at USD 140 | USD 16,724 − USD 14,000 | −USD 2,724 |

| If not assigned: premium kept | 100 × USD 2.76 | +USD 276 |

The USD 276 premium is what the investor receives if the option expires worthless. It is not a guaranteed return, and it does not protect against a significant fall in the share price after assignment.

| ORCL at expiry (18 June 2026) | What happens | Net cost per share | Outcome |

|---|---|---|---|

| Above USD 170 | Put expires worthless | – | Keeps USD 276 as income; cash freed |

| At USD 170 | Assignment likely | USD 167.24 | Owns 100 shares at effective USD 167.24 |

| Below USD 170 | Assigned – buys 100 shares at USD 170 | USD 167.24 | Owns shares at a discount to the strike; paper loss if stock continues lower |

| Well below USD 167.24 | Assigned; loss below breakeven | USD 167.24 | Loss mirrors stock ownership from USD 167.24 downward |

| ORCL at expiry | Stock position value | Option result | Approximate outcome (before costs and taxes) |

|---|---|---|---|

| USD 140 | USD 14,000 (100 shares) | +USD 276 premium | Effective cost USD 16,724; paper loss of −USD 2,724 |

| USD 160 | USD 16,000 (100 shares) | +USD 276 premium | Effective cost USD 16,724; paper loss of −USD 724 |

| USD 167.24 | USD 16,724 (100 shares) | +USD 276 premium | Break-even before costs and taxes |

| USD 170 | At the strike | +USD 276 premium | May or may not be assigned; premium kept in either case |

| USD 177+ | Put expires worthless | +USD 276 premium | USD 276 income; no shares purchased |

Approximate total result before transaction costs and taxes. Assignment may also have tax consequences depending on the investor’s jurisdiction.

To be clear: the following reasons describe the mechanics of why this strategy exists and what it achieves. They are not reasons to enter any particular trade.

A cash-secured put may not be suitable for investors who:

Downside if assigned. If Oracle is assigned at USD 170 and continues to fall, the investor absorbs the full loss from USD 167.24 downward. A move to USD 140 results in a paper loss of approximately USD 2,724 on the position. The premium received does not protect against this.

Cash tied up. The USD 17,000 reserved cannot be deployed elsewhere until 18 June 2026. At seven days, the lockup is short – but it is real. If Oracle or another opportunity requires capital during this period, it will not be available.

Elevated volatility cuts both ways. The 78.16% implied volatility that inflates today’s premiums also reflects genuine market uncertainty about Oracle’s near-term direction. Higher premiums and higher uncertainty are two sides of the same coin.

Execution. The bid-ask spread on the 170 put was USD 2.63–USD 2.69 at the time of this example. The USD 2.76 mid shown on the order ticket may not be achievable in practice. Place a limit order between the bid and mid rather than accepting the market price.

Early assignment. US equity options can be exercised before expiry. Early assignment on an out-of-the-money put is uncommon, but it is possible. Worth noting: Oracle’s next dividend ex-date is 9 July 2026, which falls after the 18 June 2026 expiry – so the dividend does not create early assignment risk for this specific trade.

Q: What if Oracle falls further to USD 150 or lower before expiry?

A: The investor would be assigned and own 100 shares at an effective cost of USD 167.24. At USD 150, that represents a paper loss of USD 1,724 per contract. This is the same outcome as having bought Oracle at USD 167.24 outright. The premium received does not change that – it only reduces the entry from USD 170 to USD 167.24.

Q: Can I close this trade early?

A: Yes. The investor can buy back the put at any time before expiry. If Oracle has recovered and the put has lost value since the trade was opened, buying it back will likely be cheaper than the premium received. If Oracle has fallen further, the put will be more expensive to close – but closing it limits further loss if the investor wants to exit.

Q: What happens if the put expires worthless?

A: The investor keeps the USD 276 premium and the USD 17,000 cash is freed. Many investors in this situation then reassess whether to repeat the trade with a later expiry – at the same strike, a different one, or not at all.

Q: Is a seven-day trade very different from a longer-dated put?

A: Yes, in a few meaningful ways. With elevated volatility, the absolute premium per day is higher than usual – which is why short-dated puts can generate comparable income to longer-dated ones in stressed markets. Time decay (theta) also accelerates in the final week, meaning the put loses value quickly if Oracle stays above USD 170. The trade resolves fast, for better or worse.

Q: What does a delta of −0.28 mean?

A: Delta measures how much the option’s price moves relative to the stock. A delta of −0.28 on the 170 put means that for every USD 1 Oracle falls, the put gains approximately USD 0.28 in value. It also offers a rough probability indicator: the market is implying approximately a 28% chance this put finishes in the money at expiry. This is not a precise prediction – it is a reflection of current market pricing.

Q: What is the dividend situation?

A: Oracle’s dividend ex-date is 9 July 2026, which falls after the 18 June 2026 expiry. This means the dividend does not affect early assignment risk for this specific trade. Had the ex-date fallen before expiry, this would require more careful consideration.

Oracle’s post-earnings sell-off on 11 June 2026 provides a clean, real-world setting to examine how a cash-secured put functions. The numbers are concrete, the trade-offs are visible, and the structure is straightforward enough to follow step by step.

To recap what this example illustrates: selling the 170 put expiring 18 June 2026 collects approximately USD 276 per contract and sets USD 167.24 as the effective entry price if assigned. If Oracle stays above USD 170, the premium is kept and the trade ends. If it falls below, the investor buys 100 shares at a cost that was defined in advance.

What the example also makes clear: the strategy does not protect against a continued decline. The 78.16% implied volatility reflects genuine uncertainty following the earnings release, and the short seven-day window means the trade resolves quickly – with no time to wait for a recovery if the stock keeps falling.

For any investor considering whether this strategy applies to their own situation, the key question is not “will Oracle recover?” It is: would you be comfortable owning 100 Oracle shares at USD 167.24 today? If yes, the cash-secured put is one way to act on that. If the current level of uncertainty makes that commitment uncomfortable, waiting – with no position – is a valid response.

The author does not hold positions in any of the instruments mentioned in this article.

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The Author is permitted to wait at least 24 hours from the time of the publication before they trade the instruments themselves.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with the aim of providing clients with valuable information and options.

This content will not be changed or subject to review after publication.

| Related articles/content |

|---|

| What investors misunderstand about covered calls | 10 Jun 2026 Covered call or cash-secured put | 2 Jun 2026 From shareholder to options user | 26 May 2026 Micron before earnings - using a covered call after a strong rally | 29 May 2026 Alphabet after earnings - how a covered call can help investors manage a strong rally | 30 Apr 2026 Tesla shares after earnings could a covered call make sense | 27 Apr 2026 A structured way to buy IWDA at a lower price using options | 20 Mar 2026 How to improve the yield on a long-term IWDA holdings | 12 Mar 2026 How to use a collar to protect stock gains - a Tesla case study | 20 Feb 2026 Palantir after earnings - using options to define a potential entry price | 4 Feb 2026 Golds pullback - thinking beyond buy or sell | 3 Feb 2026 Why options got so popular in recent years | 28 Jan 2026 |

| More from the author |

|---|

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy