Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Summary: Leveraged ETFs are built to deliver a multiple of one trading day’s return, not a smooth multiple over weeks or months, and holding one too long can quietly work against an investor’s own thesis. This article looks at how options let investors hedge a broader position, define a holding period on purpose, or engage with these instruments more deliberately.

Leveraged ETFs are built for one trading day. Here’s how options let investors work with that reality instead of against it.

Leveraged ETFs have become a fixture on retail trading platforms. US-listed leveraged ETF assets have grown to roughly USD 198 billion, with the large majority held by retail investors rather than institutions (Source: Value The Markets, as of June 2026). For investors who already follow a volatile corner of the market – semiconductors, a single index, a sector rotation story – the appeal is easy to understand: amplified exposure without opening a margin account.

There’s a catch, though. These products are built to deliver a multiple of a single day’s return, not a multiple of the return over a month or a year. Holding one past that horizon can quietly work against an investor’s own thesis. This article walks through the main way options address that directly, hedging a broader position, then runs through a few other ways investors put these instruments to work.

A leveraged ETF resets its exposure at the close of every session. If the underlying index falls 10% one day and rises 10% the next, a 3x leveraged ETF does not return to its starting value – it ends up lower, because each day’s move compounds on a different base than the day before. This effect, often called volatility decay, means a leveraged ETF’s return can diverge meaningfully from a simple multiple of the index the longer it is held, particularly in choppy, range-bound markets (Source: Britannica Money, as of June 2026).

That divergence is not theoretical. Over the five years to July 2026, IWM, the unleveraged Russell 2000 ETF, is roughly flat to slightly positive. TNA, its 3x leveraged counterpart tracking the same index, remains sharply negative over the same stretch, even after the small-cap index itself worked its way back toward break-even (Source: Bloomberg, as of July 2026). The underlying index barely moved on net over five years; the leveraged version did not track that outcome.

IWM vs TNA, indexed return, July 2021 to July 2026 (base = 0%). The unleveraged Russell 2000 ETF ended the period roughly positive; its 3x leveraged counterpart remained deeply negative despite a full market cycle. Source: Bloomberg, as of July 2026. For illustrative purposes only.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

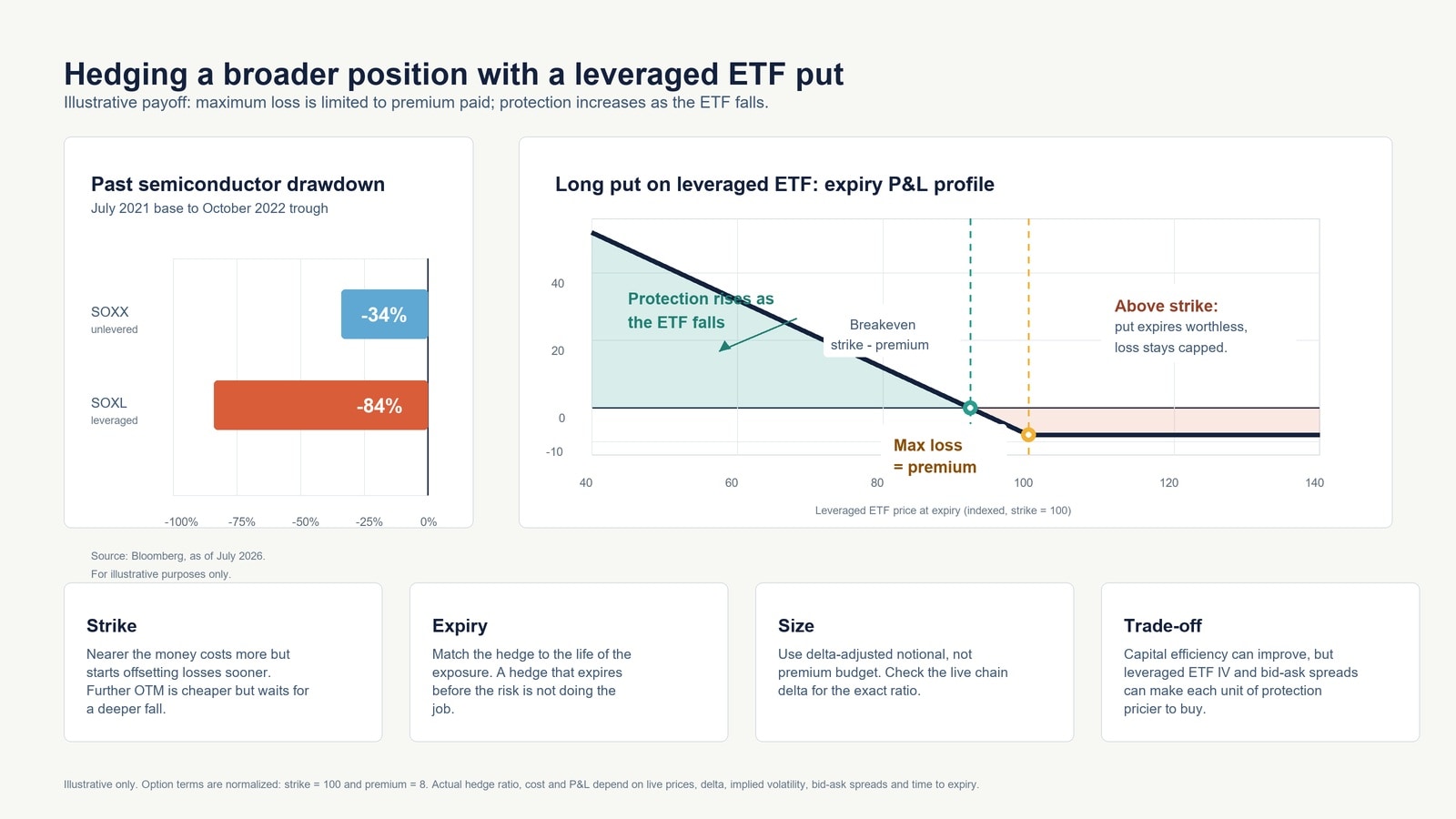

Thesis: An investor holding a basket of stocks tied to a volatile theme – semiconductors, for example – may want downside protection without liquidating the position. Buying puts directly on each individual holding can be expensive and impractical across many names.

Mechanics: Because a leveraged ETF already carries built-in sensitivity to its underlying index, a put option on the leveraged ETF can offset a proportionally larger notional swing elsewhere in the portfolio, using fewer contracts and less capital tied up in premium than an equivalent hedge built directly on the unlevered holdings. The scale of that sensitivity shows up clearly in past drawdowns: during the semiconductor selloff into October 2022, SOXL fell approximately 84% from its July 2021 base at the trough, versus roughly 34% for SOXX, the unleveraged semiconductor index ETF it tracks (Source: Bloomberg, as of July 2026).

SOXX vs SOXL, indexed return, July 2021 to July 2026 (base = 0%). The leveraged ETF’s drawdown into October 2022 ran well beyond its unleveraged counterpart’s; the same amplification that produces sharper declines also produces sharper rallies. Source: Bloomberg, as of July 2026. For illustrative purposes only.

Strategy insight – capital efficiency versus premium cost. The benefit of this approach is capital efficiency: less money tied up for a given amount of offsetting exposure. The risk is that implied volatility on leveraged ETFs tends to run structurally higher than on the unlevered index, so the hedge itself may cost more per unit of protection, even if less capital is required overall.

In our view, the same amplification that makes a leveraged ETF fall further in a selloff could also work in a put buyer’s favour, since a larger move is exactly what a long put is built to capture, and rising implied volatility during that kind of move could add a further, separate source of gain. This is a hypothesis, not a rule: the same elevated IV also makes the put pricier to buy and often comes with wider bid-ask spreads, time decay works against the position throughout, and a violent single trough, like October 2022, is no guarantee a sustained decline follows it.

Hedging a broader position with a leveraged ETF put. Maximum loss is limited to the premium paid; protection increases as the ETF falls. Source: Saxo, as of July 2026. For illustrative purposes only.

Hedging is not the only angle. A handful of others come up often enough to be worth a short mention:

None of the above is specific to a single instrument – any leveraged ETF with listed options works structurally the same way. These are some of the more widely traded examples, spanning different sectors and index exposures:

Leveraged exposure also exists on individual mega-cap technology names, the so-called Magnificent Seven, such as GraniteShares’ 2x long Nvidia product (NVDL) and Direxion’s 2x long Tesla product (TSLL); structure and availability vary by issuer and are worth confirming directly.

Liquidity varies sharply across this list, and where it’s thin, bid-ask spreads widen quickly, which can erode profitability before a position even moves. Checking the live option chain for volume and spread, rather than assuming one leveraged ETF behaves like another, remains the first step regardless of which one is involved.

Before placing the trade, check:

Assignment risk note: Leveraged ETF options are typically American-style, meaning short legs can be assigned before expiry if they move in the money. As the buyer of a put or call, there is no assignment risk – only the seller of an option faces this.

Leveraged ETFs were not designed to be held, and options on them work best when they respect that design rather than fight it. Used as a hedge, they let an investor offset risk elsewhere in the portfolio with less capital tied up. Used in the other ways above, from defining a holding period to reaching an otherwise-closed market, they open up angles the ETF itself does not offer on its own.

None of these turn a leveraged ETF into a long-term holding, and none of them remove the underlying volatility decay. What they offer instead is a more deliberate way to engage with a genuinely volatile corner of the market, with the risk defined before the position is opened, not after.

The author does not hold positions in any of the instruments mentioned in this article.

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The Author is permitted to wait at least 24 hours from the time of the publication before they trade the instruments themselves.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with the aim of providing clients with valuable information and options.

This content will not be changed or subject to review after publication.

| More from the author |

|---|

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy