Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

A selloff can create opportunity, but only if investors distinguish between temporarily weaker prices and weaker businesses.

A practical way to do that is to screen for companies with strong growth, healthy margins, solid returns on capital, low leverage, and positive free cash flow.

In the US screen, names such as Nvidia, Microsoft, Meta Platforms, and Adobe stood out, while the non-US screen surfaced a different mix including Novo Nordisk, Barrick Mining, and Experian.

These are not recommendations. They are examples from a rules-based shortlist designed to help investors focus their research during a market sell-off.

Why this matters in a selloff

When markets turn lower, almost everything gets marked down together at first. That can make good companies look no different from fragile ones. But price weakness on its own does not create value. What matters is whether the underlying business still has the ability to grow, defend margins, generate cash, and fund itself without stress.

That is why the better question in a selloff is not what is down the most? It is which companies still look strong when conditions get harder?

The screen: how we filtered for quality

We used a Bloomberg screen focused on large, liquid US-listed companies and then added filters designed to identify businesses with a stronger operating profile.

We used two starting universes:

This keeps the screen focused on larger, more established companies rather than thinly traded names that can often look statistically attractive for the wrong reasons.

We then applied the following criteria:

This is a selloff filter. It looks for stocks that have pulled back from prior highs, without simply chasing momentum.

This helps identify companies that have delivered meaningful top-line growth over time, rather than just a short burst of performance.

Higher margins can signal pricing power, operational discipline, or a stronger competitive position.

This is one of the cleaner measures of business quality. It shows whether a company is generating strong returns from the capital it deploys.

Positive free cash flow matters even more in volatile markets. It gives companies flexibility and makes earnings quality more credible.

Low leverage helps reduce refinancing risk and balance-sheet stress when conditions tighten.

Strong returns on equity can be a sign of efficient capital use, provided they are not simply driven by leverage.

Quality still needs a valuation check. So we added:

These filters do not mean a stock is cheap. They simply help avoid paying any price for quality and bring some valuation discipline into the process.

What the screens produced

We applied the framework across two universes.

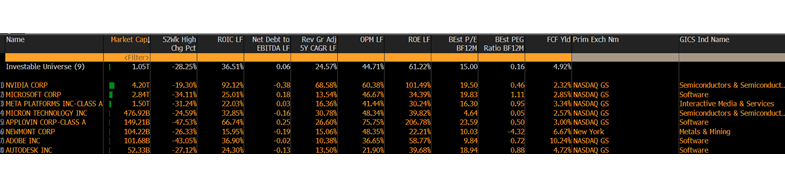

From a broad US starting universe, the screen narrowed the list to 8 names:

Nvidia – AI chips and accelerated computing

Microsoft – cloud, software, and enterprise technology

Meta Platforms – social media and digital advertising

Micron Technology – memory chips and semiconductor storage

AppLovin – mobile app advertising and software tools

Newmont – gold and copper mining

Adobe – creative software and digital marketing tools

Autodesk – design, engineering, and construction software

Source: Bloomberg, as on 26 March 2026

This is an interesting mix because it is not concentrated in just one theme. It includes AI and semiconductor leaders, platform businesses, software, and a gold producer. That matters because quality can show up in different sectors for different reasons.

The non-US version screen narrowed the universe to 10 names:

The regional mix is notable. It brings in healthcare, consumer, logistics, data services as well as metals and mining. It also shows that outside the US, quality screens can surface a broader mix of commodity-linked and defensive growth names.

The screen results highlight a few useful distinctions.

Several of the names are still cyclical or sentiment-sensitive. Micron, Nvidia, and Devon, for example, may all meet the quality threshold on returns, growth, or balance-sheet strength, but they are still exposed to cycle, commodity, or expectations risk.

That is an important reminder: a quality screen is not a low-volatility screen.

Many of the names that passed the screen have very strong operating margins, high returns on equity, or high returns on invested capital. That suggests the screen is surfacing businesses with either real pricing power, strong market position, or unusually efficient economics.

Adding forward P/E and PEG filters helped avoid a pure “best business at any price” outcome. In a selloff, this matters. A quality company can still disappoint investors if the starting valuation remains too demanding.

The net debt-to-EBITDA cap is one of the most useful filters in this kind of market. It helps separate companies that can self-fund through volatility from those that may be more dependent on favourable financing conditions.

The second screen is not just a geographic extension. It changes the flavour of the shortlist.

Compared with the US results, the Western Europe, Asia, and Canada output leans more clearly toward healthcare, mining, logistics, selected consumer names, and energy.

This framework is useful because it combines five things investors often want in tougher markets:

That is a sensible starting point for identifying companies that may be better positioned to withstand macro uncertainty.

A screen is a shortlist, not a conclusion.

It does not tell you:

In other words, a good screen can improve the odds of finding quality, but it cannot replace actual research.

In periods of market stress, the strongest opportunities often come not from buying what has fallen the most, but from identifying which businesses still look fundamentally strong after the market has turned more cautious.

That is what these screens are designed to do. They are not trying to predict the bottom. They are trying to improve the quality of the shortlist.

The US output leans more toward platform, software, and growth-heavy quality. The Western Europe, Asia, and Canada output brings in more healthcare, mining, logistics, energy, and cash-generative cyclicals. Together, they show that quality is not one sector or one market. It is a set of characteristics.

And in a selloff, that is often the more useful place to start.

Important information

This material is for information and educational purposes only. It is not investment advice, a personal recommendation, or a solicitation to buy or sell any financial instrument. The securities named are included solely as examples from the screening output to illustrate the framework. Past performance and historical financial metrics are not reliable indicators of future results. Investors should conduct their own analysis and consider their objectives, financial situation, and risk tolerance before making any investment decision.

This material is marketing content and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with the aim of providing clients with valuable information and options.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy