Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

UK wealth management is undergoing profound transformation. Market dynamics are completely reshaping the sector. For boutique investment-driven firms, their future hinges on strategic choices that will determine their long-term viability, sustainability, and relevance.

The consolidation wave: threat or opportunity?

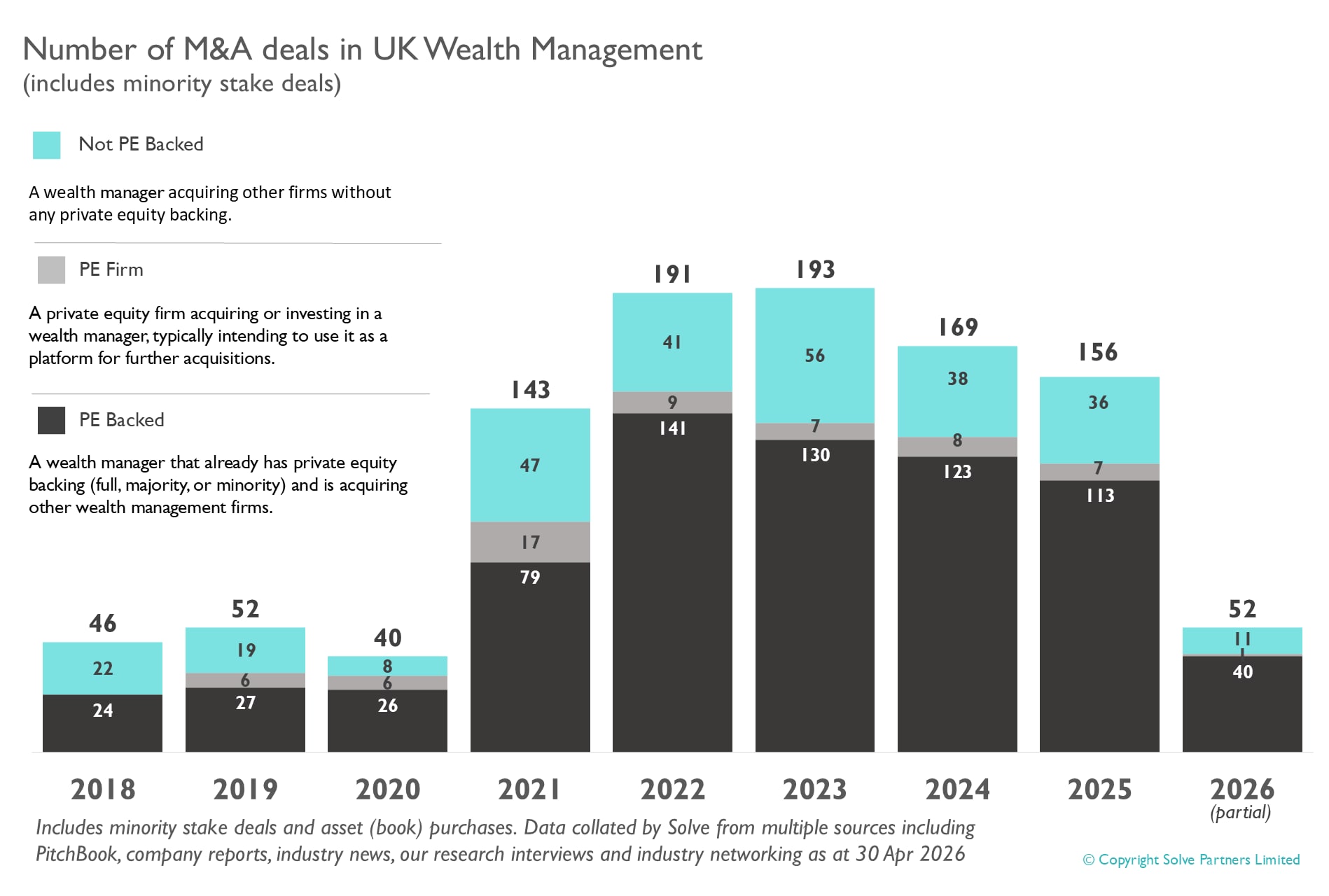

Consolidation in UK wealth management continues to drive industry change for all types of firms. Larger players, often backed by private equity and driven by economies of scale, continue to acquire smaller firms at pace. Large players increasingly favour full-service offerings, presenting a challenge for investment-led boutiques, where the focus is investment expertise and not financial planning.

Solve Partners tracks the market trends in consolidation in wealth and, since 2021, over 88% of the known deals have been boosted by PE money at a rate of 140-160 deals per year. The influx of PE investment into the sector has been one of the biggest changes seen in recent years and is a reflection of the value creation opportunity by those investors.

For boutique investment-led wealth managers, the consolidation trend creates an uncomfortable conundrum. Selling provides an opportunity to access advisory services, scale, resources, and to position for growth. The downside is loss of identity and a long-built reputation. Remaining independent means retaining that identity and reputation; however it also means competing against increasingly well-resourced rivals who can invest heavily in technology, talent, and client acquisition.

Yet consolidation could present genuine opportunities for a well-positioned boutique firm. Acquired firms face integration challenges, experience cultural dilution and, sometimes, a loss of personalised service. Complex clients and those who value bespoke investment management and direct access to decision-makers can find themselves lost in larger organisations. This creates clear opportunities for boutiques that can deliver a truly personalised service. A distinct segment of wealthy individuals actively seeks smaller, agile firms. These clients value the flexibility, responsiveness, and personal attention boutiques provide.

Turning regulatory pressure into competitive advantage

The regulatory environment remains demanding. The FCA's focus on Consumer Duty, scrutiny of charges, and ESG expectations have intensified year on year. However, regulatory pressure impacts firms differently. Firms with transparent fee structures and genuine, responsibly led, investment expertise are well-positioned. FCA scrutiny falls heaviest on firms where the value proposition is unclear or where fees seem disconnected from client outcomes.

For boutiques delivering a well-governed investment service and nurturing strong client relationships, Consumer Duty represents competitive advantage, raising the bar and exposing weaker, less-specialist competitors.

Tax changes and the UHNW migration risk

The changing UK tax landscape represents an acute threat for boutique wealth managers focused on UHNW clients. Abolition of the ‘non-dom’ regime, changes to capital gains tax and IHT, and broader wealth taxation rhetoric have created genuine concern in investors. In a higher-tax state, UHNW clients may consider relocating to jurisdictions with lower tax burdens. For boutiques dependent on a concentrated UHNW book, losing even two or three key relationships could severely challenge them. To mitigate this, boutiques could partner with firms that are multi-jurisdictional, enabling them to continue servicing clients who leave the UK.

The advice-led ascendancy

One of the most significant structural shifts has been the rise of advice-led firms at the expense of more traditional investment-led models. This reflects regulatory pressure on investment fees, proliferation of low-cost passive solutions, and a growing client demand for holistic, end-to-end investment services.

For boutique investment-led managers, this represents both philosophical challenge and practical threat. The traditional model - where investment expertise drives primary value - increasingly looks outdated when clients can access good returns through low-cost multi-asset funds and model portfolios. In a bull market, passive investment management has proved successful, but with recent market volatility and a likely market bubble, passive management carries the risk of tracking down.

While advice-led firms excel at financial planning, tax efficiency, and behavioural coaching, they can struggle with genuinely complex investment needs. For boutiques, the strategic response should be to maintain focus upmarket, on clients whose investment complexity genuinely justifies bespoke portfolio management - one where the value proposition is defensible.

Cost to serve: the efficiency imperative

Harsh reality is that cost to serve has risen dramatically while fee pressure intensifies. Technology expectations have soared - clients expect mobile apps, sophisticated reporting and real-time access to data. Regulatory compliance demands ongoing investment in delivering suitable services while recognising vulnerabilities. Cyber security grows more onerous. Talent costs remain stubbornly high.

This economic pressure forces difficult strategic choices: simplify the client offering and service delivery, pursue acquisition (requiring capital and risking integration issues), or fundamentally reconsider which activities truly require boutique expertise or which are a commodity and can be standardised or outsourced. The latter enables boutique firms to become more agile; no longer sidetracked by operational issues and constraints, they can truly focus on strategy. Ultimately, reacting more quickly to market volatility and changing market dynamics will bring competitive advantage.

The strategic response: focus on value, outsource the rest

For boutique investment-led wealth managers confronting these dynamics, the path forward requires clarity about key selling points. What does the firm do exceptionally well that clients cannot easily find elsewhere? For most genuinely investment-led boutiques, the answer combines sophisticated portfolio construction, access to institutional-quality opportunities, personalised service from senior professionals, and flexibility to pursue client-specific strategies.

Notably, portfolio administration, fund dealing, custody, regulatory reporting, and performance measurement generate little revenue and create no real competitive advantage. These activities consume significant resource and worse, they distract management from activities that do create value.

It’s imperative to review the operating model - identifying every function that can be standardised, rationalised or commoditised, and centralising it. Better still, consider partnering with specialists who invest heavily in delivering operational excellence and commodity services as their primary focus.

Boutique investment-led wealth managers that thrive over the next decade will focus on core competencies while partnering strategically for everything else. This requires a mindset shift from "we must control every aspect" to "we must ensure excellence, whether delivered internally or through carefully selected partners."

This focus creates several competitive advantages. First, it allows boutiques to maintain lean cost structures while delivering service quality rivalling larger firms. Second, it enables genuine specialisation - when not distracted by operations, firms can develop deep expertise in specific strategies, asset classes, or client segments. Third, it makes boutiques more attractive to talent: investment professionals who join small firms to practice portfolio management, not wrestle with operational issues.

Saxo’s conclusion: adaptation and opportunity

The market forces reshaping UK wealth management - consolidation, regulatory intensity, tax uncertainty, advice-led competitors, and cost pressure - are real and consequential. Yet history suggests disruption creates opportunities for nimble, strategically clear firms willing to adapt. The winning formula for boutiques rests on three pillars.

In the melee of activities that are going on in the market today, firms need to be able to react quickly. The consolidation wave, regulatory burden, and operational complexity threatening unfocused boutiques benefit those firms with strategic clarity. By partnering for operational excellence while focusing on investment strategies and client relationships, boutique investment-led wealth managers can not merely survive but thrive.

The boutiques that emerge stronger will be those that made difficult strategic choices early, invested in necessary partnerships and platforms, and protected their most valuable asset: the time their investment professionals spend adding genuine value for clients.

|  |

Tue Mortensen | Reece BakerSenior Sales and Relationship Manager, United Kingdom +44 (20) 71512061 reeb@saxomarkets.com |

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy