Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

For years, the U.S. has been the uncontested leader in technology—commanding the world’s most advanced chips, deepest capital pools, and strongest platforms.

But China’s tech ecosystem is closing the gap. Alibaba’s latest earnings were a reminder that China’s giants are proving they can monetize artificial intelligence and cloud computing at home, even under the weight of U.S. restrictions.

The question for investors is no longer if China can catch up—it’s how far and how fast.

China once rode a demographic dividend, with a vast pool of low-cost labor fueling manufacturing and export growth.

With the workforce now shrinking, the country is pivoting to an innovation dividend. That means AI, green energy, and advanced manufacturing are taking center stage.

For investors, it’s a structural shift that creates new opportunities.

Unlike the U.S., which pushes the frontier with ever-larger models and more advanced chips, China’s strategy is different.

China isn’t competing to build the biggest or most powerful AI models. It is making AI more efficient, accessible, and deeply embedded across the economy. The key enablers for China’s AI strategy remain in place, such as:

This creates an ecosystem where economics matter more than perfection, and good-enough domestic chips and efficient models can transform e-commerce, payments, logistics, and consumer services.

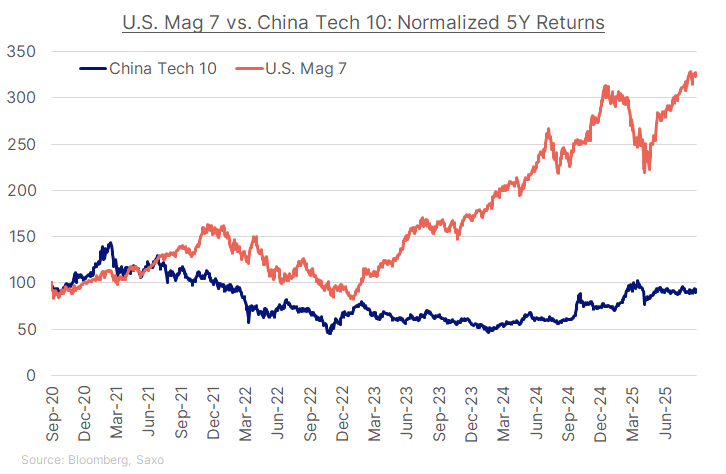

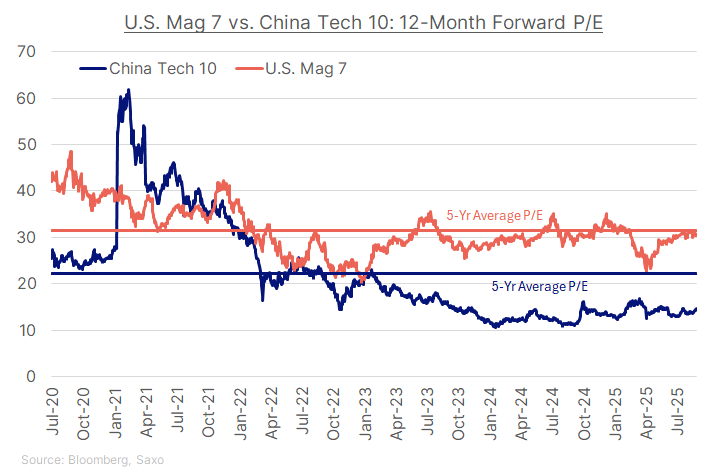

Bloomberg’s China Tech Select 10 (comprising Alibaba, Baidu, BYD, JD.com, Meituan, Midea, NetEase, Tencent, Trip.com, and Xiaomi) provides a powerful foil to the U.S. Mag 7 of Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla.

The contrast highlights a two-track story: U.S. tech is still the global benchmark at the innovation frontier, while China tech is catching up fast at home, with policy, scale, and valuation on its side.

China’s pivot to innovation and AI is real, but not without limits. Domestic players can thrive within the firewall, but globally they face hurdles around trust, compliance, and chip access. Still, the building blocks – data, energy, talent, and governance – give China the capacity to keep closing the gap at home, even if the U.S. remains the global benchmark.

For now, U.S. megacaps like Nvidia, Microsoft, and Alphabet remain the leaders at the frontier of hardware and platforms. But with valuations stretched in the U.S. and improving in China, the smarter allocation may be to think in two tracks: U.S. tech for global leadership, and China tech for domestic scale.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy