Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

The selloff in the software sector in February was driven by AI disruption fears, a sharp valuation reset, and wider concerns about funding conditions, including private credit exposure to software businesses.

Recently, however, the software sector has stabilised from macro relief, resilient earnings expectations, and a shift from indiscriminate selling toward more selective differentiation across business models.

In our opinion, the key question now is not whether the recovery in software as a sector (SaaS) can continue, but it is about how can investors differentiate between companies that are becoming more essential in an AI-driven world and which may be becoming more replaceable.

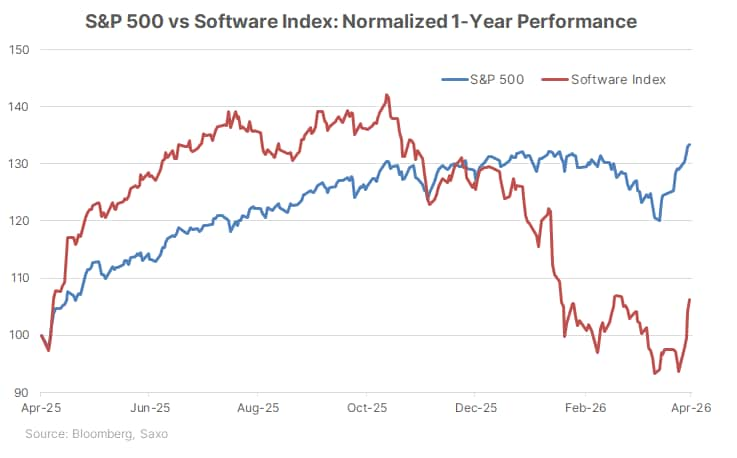

This week's rebound in software stocks comes after a massive selloff in the sector earlier this year. The US software index is up close to 10% in April (as of 16 April), vs. less than 8% gain in the S&P 500. That rally in the software sector follows an extended period of weakness, with the broader software sector still down sharply this year and several large software names, including Oracle and Microsoft, remaining below where they started the year.

That sharp bounce does not necessarily mean the sector has fully recovered. Instead, it raises a more useful question: has the market moved beyond indiscriminate selling and into a more selective phase? In our opinion, that is now the right way to frame the software story. The earlier selloff was driven by a mix of factors rather than a single trigger, including AI disruption fears, rich starting valuations, questions over returns on heavy AI spending, and broader financing concerns such as private credit exposure. The recent stabilisation suggests investors are increasingly distinguishing between software companies with proprietary data, deep workflow integration and clearer monetisation paths, and those whose products may be more exposed to automation or pricing pressure.

Investor concerns intensified as new AI models and tools raised questions about whether some software functions could be replicated, automated, or delivered more cheaply. This hit sentiment across the sector, particularly in business models tied to standardised workflows or seat-based pricing. Investors reassessed whether scale, data, and distribution would protect incumbents or whether more powerful AI models could compress parts of their value proposition.

Anthropic’s Mythos became part of that discussion, as initially added to disruption fears and helped drive a repricing across software, but it later also forced investors to distinguish between companies that may be reinforced by more powerful AI and those that may be more exposed to it.

The selloff was worsened by stretched starting valuations. When the narrative shifted, many software companies had little valuation cushion, given the Software Index traded close to a multiple of 30x at the end of 2025 compared to S&P 500 around 22x.

As AI enthusiasm matured, investors also became more focused on whether large AI investments by hyperscalers and enterprises would translate into durable returns.

The selloff became more significant when it moved beyond an equity valuation story and began to raise financing concerns. Software companies account for around 16% of the roughly $1.5 trillion U.S. loan market tied to private credit, and fears of default in the private-credit funds exacerbated the software sell-off.

This mattered because it suggested that weaker software valuations and earnings concerns could affect not just public market sentiment, but also funding conditions, deal activity, and broader risk appetite.

The Middle East shock added another layer of pressure by lifting oil prices and reviving inflation concerns. The technology benchmark index, Nasdaq, entered correction territory in late March as investors reacted to war-related oil and inflation risks. That backdrop was particularly unhelpful for software, which is often treated as a longer-duration sector and is therefore sensitive to changes in yields and rate expectations.

One important stabiliser has been a shift away from indiscriminate selling. Investors are increasingly focused on whether software companies benefit from proprietary enterprise data, embedded workflows, and high switching costs.

Companies such as Oracle are being viewed as better positioned because of these characteristics, while Workday has faced more debate given concerns that some of its data is more standardised and therefore potentially easier for AI systems to work with or replicate. Microsoft also fits into this broader discussion because of its enterprise distribution, cloud ecosystem and installed base. These are market observations rather than recommendations. At the same time, selectivity can cut both ways: if AI drives margin pressure, lowers pricing power, or reduces seat growth in parts of the sector, the rebound could remain narrow and uneven.

There is also a cyber angle here. Mythos’ vulnerability-discovery capabilities have added to concerns about what more powerful AI models could expose in legacy systems and critical infrastructure. That likely helped reinforce the rebound in cybersecurity-linked software such as Palo Alto Networks and CrowdStrike, especially as geopolitics also increased demand for resilience trades. However, this support may prove partial rather than broad-based, as stronger demand for resilience does not eliminate wider risks from weaker enterprise IT spending or a more selective budgeting cycle.

A second stabiliser was the easing in geopolitical stress. The U.S.-Iran ceasefire and broader efforts to end the conflict helped revive appetite for technology stocks and lifted the Nasdaq to a fresh record high on April 15. That helped reduce immediate inflation and rate concerns, which had weighed on software valuations. Even so, software remains sensitive to yields and the broader rate outlook, so any renewed inflation pressure, oil shock, or repricing of rate expectations could quickly challenge the sector again.

A third support came from earnings. Bloomberg data show that Wall Street analysts have been raising their earnings estimates for the sector. Profits at software and services companies are expected to increase 16.5% in 2027, up from 15.7% at the end of February. The data also points to a similar improving trend in 2027 revenue expectations. That suggests that while valuation multiples had compressed sharply, forward earnings and revenue expectations have held up better than the selloff had implied. The risk, however, is that these expectations still need to be delivered in an environment where enterprise customers may become more cautious on IT budgets and where AI monetisation may not fully offset margin pressure or competitive intensity.

The combination of rising projections and falling prices has also helped the group’s valuation. The US software index is now trading at about 23.2 times forward earnings, compared with roughly 35 at its peak over the past year. That leaves the software sector much closer to the S&P 500, which is trading at about 20.7 times forward earnings. In practical terms, that means the premium investors are paying for software has narrowed sharply, allowing greater focus on earnings durability and business quality rather than valuation alone. Still, the sector is not obviously cheap in absolute terms, and valuation risk could re-emerge quickly if growth slows, guidance disappoints, or markets become less willing to pay a premium for future earnings.

In our opinion, the most useful way to think about the sector now is not whether software as a whole is cheap or expensive, but whether individual business models are becoming more essential or more replaceable in an AI-driven environment.

A factual way to assess that is to look at whether a company has:

proprietary or hard-to-replicate enterprise data. For example, companies such as Microsoft, Oracle, Salesforce or Palantir may be viewed through this lens because they sit on large enterprise data sets, customer workflows, analytical layers or distribution ecosystems that may be difficult to replicate.

products embedded in mission-critical workflows. For example, software used in core cloud infrastructure, enterprise resource planning, cybersecurity, databases, analytics, or customer relationship management may be harder to displace than lighter productivity or support tools.

evidence that AI is supporting revenue, pricing, backlog or contract value. For example, investors may look for signs such as stronger remaining performance obligations, improving deal sizes, higher customer spend, or management commentary linking AI products to commercial outcomes rather than product launches alone.

a valuation reset that is matched by stable or improving earnings expectations. For example, a stock may warrant a closer look if its multiple has compressed materially but consensus earnings expectations, backlog trends, or guidance remain relatively resilient.

Areas that may warrant more caution are those where products are tied to more standardised tasks, pricing remains dependent on simple seat growth, or AI could lower barriers to entry.

For example, functions such as below may face greater pressure if AI agents can perform similar tasks more cheaply or efficiently:

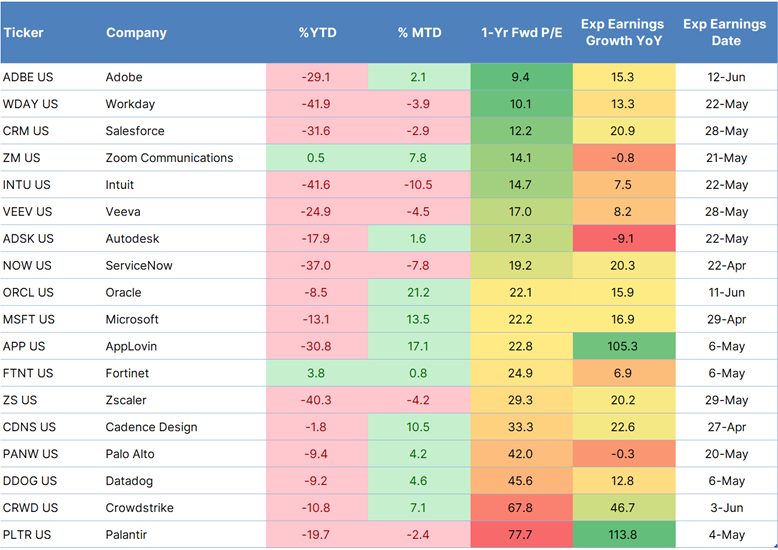

The table below provides a snapshot of larger software and cybersecurity names across valuation, performance and growth expectations. It is sorted by next-year estimated price-to-earnings, which helps show where the derating has been most severe and where the market may still be assigning a premium. Used alongside year-to-date and month-to-date performance and expected earnings growth, it offers a practical way to compare which names look more heavily reset, which still command richer valuations, and where investor expectations remain relatively stronger.

Source: Bloomberg

In our opinion, the key shift is that investors are no longer asking whether all software is at risk. They are asking which business models are reinforced by AI and which ones may be challenged by it. Mythos appears to have played into that shift by first intensifying disruption fears and then helping investors differentiate between larger platforms and cybersecurity names that may benefit from stronger AI capabilities, and those whose value proposition may come under greater pressure.

That said, the rebound still needs to clear several tests. AI may support demand in some areas, but it may also compress margins, weaken pricing power, and intensify competition in others. Software also remains sensitive to rates, enterprise spending and valuation discipline. In our opinion, that means the recovery can continue, but it is more likely to be selective than broad and more dependent on delivery than on narrative alone.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy