Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Summary: ExxonMobil has had a volatile few weeks, and its options market is reflecting that. With an IV rank near 75%, premiums are above average relative to XOM’s own history - a condition that typically favours sellers over buyers. This article explains what IV rank means, why XOM’s is elevated, and how three common strategies use elevated premiums to their advantage.

When fear elevates option premiums, disciplined sellers take notice – here is what ExxonMobil’s current volatility profile is signalling.

ExxonMobil (XOM) has endured a turbulent few weeks. Geopolitical disruptions in the Middle East, falling oil prices, and an approaching earnings date have combined to push the stock sharply lower – and to push its options premiums sharply higher. With an IV rank of 78.34% and an IV Percentile at 92%, XOM is currently one of the more interesting candidates in the energy sector for traders considering premium-selling strategies. This brief explains why – and what to keep in mind.

A volatile stock price is not always a sign of fundamental deterioration – but it is always a signal worth reading.

XOM has given back meaningful ground in recent sessions, closing at $148.77 on 15 April and now trading below its 50-day moving average at $154.56. Two significant single-day declines were driven by a combination of Middle East geopolitical risk, energy demand uncertainty, and investor positioning ahead of Q1 earnings. After reaching nearly $175 in early 2026, the stock has retraced sharply – a move that is now fully reflected in options pricing. The company reports first-quarter 2026 results on 1 May, and its own guidance suggests material earnings headwinds – including negative timing effects estimated at between $3.5 billion and $4.9 billion, partly attributable to disruptions across its LNG operations.

XOM (1W/1D) — After peaking near $175 in early 2026, ExxonMobil has pulled back sharply to $148.77, now trading below its 50-day SMA ($154.56) while remaining well above its 200-day SMA ($125.55). Source: SaxoTrader, 15 April 2026.

Analyst sentiment is mixed. A majority retain Buy ratings, but recent downgrades and new Underperform ratings from sell-side firms reflect genuine disagreement about near-term valuation. That disagreement – combined with energy sector macro uncertainty – is precisely what elevates option premiums.

Implied volatility in isolation tells you little – IV rank tells you where premiums stand relative to their own history.

Implied volatility (IV) is the market’s forward-looking estimate of how much a stock might move over a given period. It is embedded in every option’s price: the more uncertain the market, the higher the IV, and the more expensive options become – for buyers seeking protection and for speculators seeking leverage alike.

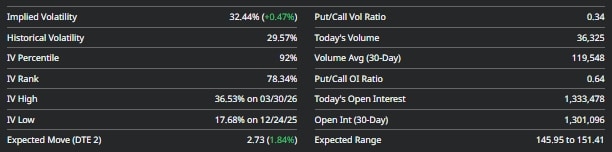

IV rank contextualises this. Rather than asking “is IV high?”, it asks: “where does today’s IV sit relative to the range of IV levels observed over the past 52 weeks?” XOM’s IV rank currently stands at 78.34%, meaning that on approximately 78 out of every 100 trading days over the past year, its implied volatility was lower than it is today. The IV Percentile – a closely related but distinct measure – comes in at 92%, indicating that current premiums sit in the 92nd percentile of all observed IV levels over the same period. Whichever measure you use, the message is the same: options are more expensive than usual relative to XOM’s own recent history.

XOM options data as of 15 April 2026 — IV rank at 78.34% and IV percentile at 92% confirm premiums are elevated relative to the stock's own history. Current IV (32.44%) sits above historical volatility (29.57%), with a put/call volume ratio of 0.34 suggesting call-side activity is dominant. Source: barchart.com.

For buyers, this is a caution flag: you are paying above-average prices for exposure. For premium sellers, it works the other direction – you receive above-average compensation for the risk you take on. The IV rank does not tell you to sell. It tells you that, if you were already inclined to sell, the conditions are more favourable than on most days.

Two distinct forces are compounding each other – one structural, one event-driven.

The first is the energy sector’s macro backdrop. Oil prices are navigating a complex environment: potential normalisation of Middle East geopolitics could remove one of the key risk premiums that has been supporting energy prices, while concerns about global demand in a slowing economic environment and ongoing uncertainty around OPEC supply discipline create a wide range of plausible outcomes for oil over the coming months. Energy stocks are sensitive to oil price moves in both directions, and that sensitivity keeps implied volatility structurally elevated relative to many other sectors.

The second driver is the earnings event. ExxonMobil reports Q1 2026 results on 1 May. Ahead of any binary catalyst – and an earnings release is one of the most predictable binary events in the equity calendar – options markets tend to price in elevated IV as participants seek protection against sharp post-announcement moves. XOM’s own guidance for material earnings headwinds adds to that uncertainty, widening the range of plausible outcomes for the stock on and after earnings day.

These two forces – sector-level macro uncertainty and a near-term earnings catalyst – are compounding each other, producing an IV rank that sits well above the median for this name.

Selling premium when IV rank is high is not about predicting direction – it is about being compensated more richly for the range you define.

When IV is elevated, common premium-selling structures generate more income for the same strike distance from the current price. This has two practical implications. First, the break-even point moves further from the current price – the stock has to move more against the seller before the position loses money. Second, if IV subsequently normalises – as it commonly does after an earnings event passes, a phenomenon known as volatility crush – the value of the sold options declines independently of any stock price move, adding a second potential source of profit.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

Three structures that options traders commonly consider in high-IV environments:

Each of these structures expresses a broadly neutral-to-bullish view on XOM: the seller is not predicting the stock will rise, but rather that it will not fall significantly below the strike they have chosen. The elevated IV rank simply improves the terms on which that view can be expressed.

Favourable conditions reduce risk – they do not eliminate it.

IV can stay elevated or rise further. An IV rank of 75% does not mean IV cannot reach 90% or 100%. If the geopolitical environment deteriorates, or if oil markets face a new shock before earnings, XOM could move significantly beyond what the market is currently implying. Selling premium into a rising volatility environment is painful.

Earnings carry binary risk. The earnings release on 1 May is a genuine binary event. If ExxonMobil’s results disappoint relative to already-lowered expectations – or if guidance for the remainder of 2026 surprises negatively – the stock can move sharply in either direction. Selling puts before the earnings date means direct exposure to that move.

Energy-sector idiosyncratic risk is non-trivial. XOM is not a utility. Its earnings and stock price are sensitive to oil prices, geopolitical events, and macroeconomic demand in ways that can produce rapid, large moves. Position sizing matters proportionally more here than in lower-volatility names.

Timing around the catalyst. Some traders prefer to sell premium after an earnings event, once the binary catalyst has passed and IV has crushed. This sacrifices the elevated pre-earnings premium but avoids the binary risk of the event itself. Both approaches represent different risk/reward trade-offs – neither is universally superior.

IV rank is one signal among many, but it is a useful one. At approximately 75%, XOM’s options market is telling you that uncertainty is elevated relative to most of the past year – and that premium sellers are currently being compensated more generously than usual for taking on defined risk in this name.

Whether that compensation is attractive enough depends on your own assessment of the energy sector, your view on how ExxonMobil’s earnings might play out on 1 May, and your capacity to hold a position through what could be a volatile few weeks. High IV rank opens a window. It does not tell you whether to step through it.

Understand the structure before placing it, size positions relative to your overall portfolio, and have a clear plan for what happens if the stock moves against you.

| More from the author |

|---|

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy