Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Singapore equities have been getting more attention, and for good reason. The STI has benefited from a mix of defensive income appeal, strong bank earnings, resilient domestic demand, relatively stable Singapore dollar dynamics, and investor interest in markets seen as more insulated from global policy and geopolitical shocks.

Policy support has also helped. Measures such as the Equity Market Development Programme are aimed at deepening Singapore’s equity market, improving liquidity and broadening investor participation beyond the most familiar large-cap names. MAS says the EQDP is intended to strengthen the local asset-management and research ecosystem and increase investor interest in Singapore equities.

But for many investors, Singapore equity exposure still begins and ends with the big banks, large REITs and a handful of STI heavyweights. That may leave part of the market underexplored.

Below the STI, Singapore’s small and mid-cap universe offers exposure to a different set of themes: semiconductor supply chains, AI infrastructure, data-centre backup power, construction, civil engineering, gold, aviation fuel, luxury watches and agribusiness. These are not always household names, and that makes a disciplined screen useful as a first step.

The aim is to identify companies where earnings growth, profitability, leverage discipline and share-price momentum currently appear to be aligned. That can help investors build a more focused research list, while still recognising that small and mid caps carry higher volatility, liquidity and company-specific risks.

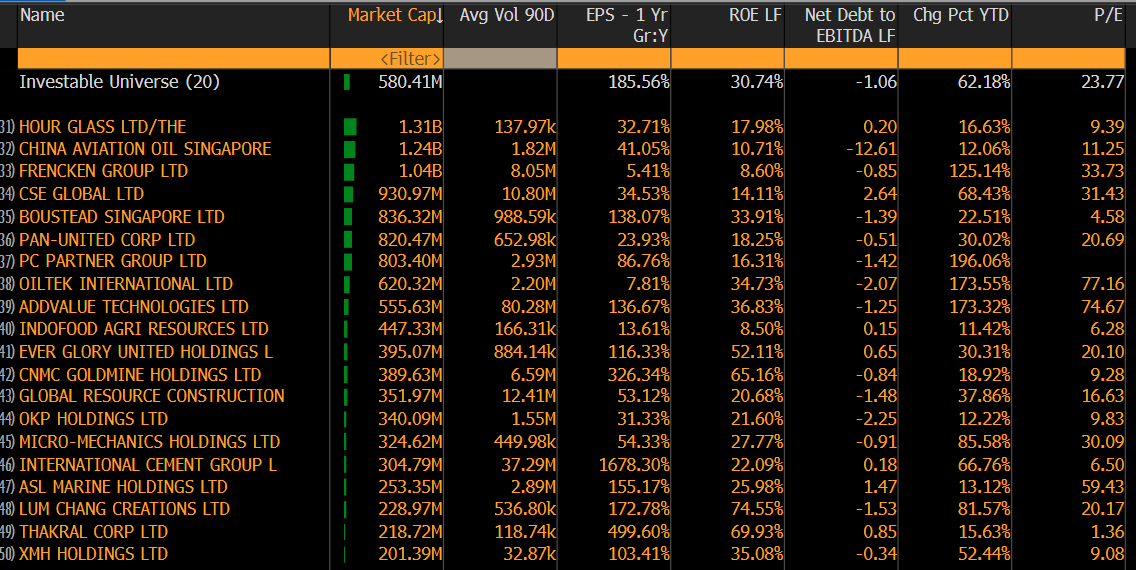

Using that framework, our screener identified 20 Singapore-listed small and mid-cap stocks that may warrant closer research. The list should be treated as an informational starting point, not as investment advice or a recommendation to buy, sell or hold any security.

This screen identified Singapore-listed small and mid-cap stocks using the following filters:

These filters are intended to narrow the universe to companies with a combination of earnings momentum, profitability, balance-sheet discipline and share-price strength.

However, they do not assess whether a stock is attractively valued, whether earnings growth is sustainable, whether liquidity is sufficient, or whether the company is suitable for a particular investor. Those questions require further analysis.

The screen is designed to reduce two common risks in small-cap investing: chasing low-quality momentum and focusing only on apparently cheap stocks with weak fundamentals.

EPS growth above 5% helps identify companies where earnings are moving in the right direction. This can be useful in small and mid caps, where improving earnings visibility, contract wins or cyclical recovery can sometimes change market perception.

ROE above 8% adds a profitability filter. It helps identify companies generating a reasonable return on shareholder capital. Still, ROE should be reviewed carefully, as it can be affected by leverage, asset sales, low equity bases or one-off gains.

Net debt/EBITDA below 3x helps remove highly leveraged companies. This is important because smaller companies may have less financial flexibility if funding costs rise, cash flow weakens or refinancing conditions tighten.

YTD share-price gain above 10% adds a momentum filter. This helps identify stocks where the market has already started to recognise a stronger earnings profile or investment narrative. The risk is that some of the positive news may already be reflected in the price.

In short, the screen identifies where the numbers look interesting. It does not determine whether the stocks are attractive investments.

The list below is arranged by market capitalisation, from largest to smallest, based on the screen.

Source: Bloomberg Equity Screener

What it does:

The Hour Glass is a luxury watch retailer with boutiques across Asia-Pacific. It sells high-end watches and benefits from demand for premium and collectible timepieces.

Why it may be interesting:

It offers exposure to luxury consumption, wealth effects and demand for scarce luxury watch brands. Among the names in the screen, it may appeal to investors researching established consumer businesses rather than higher-growth but less proven small-cap stories.

Key risk:

Luxury demand can weaken if consumer sentiment slows, wealth effects fade or the watch resale market cools. Inventory management, brand allocation and discretionary spending cycles remain important.

What it does:

China Aviation Oil Singapore is involved in jet fuel supply and trading, mainly serving China’s aviation market and international aviation customers.

Why it may be interesting:

It provides exposure to aviation fuel demand and air travel activity. Its low leverage profile may also be relevant for investors screening for balance-sheet resilience.

Key risk:

Margins can be affected by oil-price volatility, trading conditions and aviation demand. China-linked exposure and changes in fuel procurement dynamics also need to be monitored.

What it does:

Frencken provides precision engineering and integrated manufacturing solutions for sectors such as semiconductors, life sciences, medical, industrial automation and automotive.

Why it may be interesting:

It is one of the Singapore-listed names with exposure to advanced manufacturing and the semiconductor equipment supply chain. This makes it relevant for investors researching second-order links to the global technology and AI cycle.

Key risk:

The business is cyclical. A slowdown in semiconductor capex, industrial demand or customer orders could pressure earnings and margins.

What it does:

CSE Global provides technology solutions across automation, communications, electrification and infrastructure-related systems.

Why it may be interesting:

It has exposure to infrastructure upgrades, industrial digitalisation, energy transition projects, utilities and automation demand. This gives it a broader industrial technology angle.

Key risk:

Leverage is higher than most names in the screen. Project execution, cash collection, order-book quality and refinancing conditions need to be watched closely.

What it does:

Boustead Singapore is a diversified engineering and technology group with exposure to energy engineering, geospatial technology, healthcare and real estate solutions.

Why it may be interesting:

It has a more diversified and established business model than many smaller names in the screen. Its exposure to geospatial technology and infrastructure-related services may be relevant for investors researching quality mid-cap exposure.

Key risk:

The conglomerate structure can make valuation more complex. Different business segments may perform very differently, so investors need to understand what is driving earnings and cash flow.

What it does:

Pan-United supplies ready-mix concrete and low-carbon concrete solutions, including more sustainable building materials.

Why it may be interesting:

It is a Singapore construction-linked name with a sustainability angle. Low-carbon concrete may become more relevant as developers and governments focus on greener building materials.

Key risk:

Construction demand, raw material costs and pricing discipline are key risks. Even essential materials businesses can face margin pressure when input costs rise or project demand slows.

What it does:

PC Partner designs and manufactures computer electronics, including graphics cards, mini PCs, embedded systems and gaming hardware.

Why it may be interesting:

It sits in the broader computing hardware ecosystem. With AI demand expanding from data centres to PCs and edge devices, hardware-linked names may attract investor attention. It is also one of the strongest YTD performers in the screen.

Key risk:

The stock has already rallied sharply, which raises valuation and momentum-reversal risks. Demand may also be cyclical and linked to gaming, consumer hardware and AI-related product cycles.

What it does:

Oiltek provides process technology and renewable energy solutions for the vegetable oils industry, including edible and non-edible oil refining.

Why it may be interesting:

It gives exposure to agri-processing, renewable energy solutions and food-related industrial capex. This is a niche part of the food and vegetable-oils value chain.

Key risk:

Project margins, order-book delivery and customer capex cycles matter. Valuation risk should also be assessed if recent earnings growth proves difficult to sustain.

What it does:

Addvalue develops satellite-based communication and digital broadband products used across sea, land, air and space connectivity.

Why it may be interesting:

It is a niche satellite communications and connectivity play. Demand for resilient communications infrastructure could support investor interest in this area.

Key risk:

Commercialisation timelines can be long. Smaller technology companies can face uneven revenue, funding needs and profitability cycles.

What it does:

Indofood Agri Resources is a vertically integrated agribusiness involved in oil palm cultivation, milling, refining and branded cooking oil products.

Why it may be interesting:

It gives exposure to food, agriculture and palm-oil markets. This may behave differently from banks, REITs or technology stocks, which can be relevant for investors looking at diversification within Singapore equities.

Key risk:

Earnings are sensitive to palm oil prices, weather, FX movements, regulation and ESG scrutiny. Commodity-linked earnings can change quickly.

What it does:

Ever Glory United is a Singapore-based mechanical and electrical engineering contractor.

Why it may be interesting:

It sits in the building services and infrastructure ecosystem. Mechanical and electrical contractors can benefit from construction activity, building upgrades and infrastructure projects.

Key risk:

The sector can be highly competitive, with tight margins and working-capital swings. Investors need to assess whether profits are converting into cash flow.

What it does:

CNMC Goldmine is a gold mining company focused on the Sokor Gold Field in Kelantan, Malaysia.

Why it may be interesting:

It offers equity-market exposure to gold. That may be relevant for investors studying gold-linked equities during periods of geopolitical risk, central-bank gold buying or lower real-yield expectations.

Key risk:

Gold miners carry operational risk. Earnings depend on gold prices, production volumes, mining costs, regulatory conditions and mine execution.

What it does:

Global Resources Construction is involved in construction projects including public housing, industrial complexes and infrastructure works.

Why it may be interesting:

It offers exposure to Singapore construction and infrastructure activity. If local building and public-sector project activity remains supported, contractors may continue to see order-flow opportunities.

Key risk:

Construction earnings can be lumpy. Project delays, labour costs, material costs and margin pressure are key risks.

What it does:

OKP Holdings is an infrastructure and civil engineering group specialising in roads, expressways, airport runways, bridges and related public infrastructure.

Why it may be interesting:

It provides exposure to public infrastructure spending and civil engineering demand in Singapore. These can be steadier than some private-sector construction segments.

Key risk:

Tender competition, project delays and cost overruns can weigh on margins and cash flow.

What it does:

Micro-Mechanics designs and manufactures consumable parts and precision tools used in semiconductor assembly and testing.

Why it may be interesting:

It is a Singapore-listed semiconductor supply-chain proxy, with exposure to chip production, testing and advanced packaging activity. It may be relevant for investors researching supply-chain links to AI and electronics demand.

Key risk:

Semiconductor cycles are volatile. If chip demand or capex slows, smaller suppliers can feel the pressure quickly.

What it does:

International Cement produces and distributes cement and gypsum plasterboards, mainly in Central Asia.

Why it may be interesting:

It gives exposure to infrastructure and construction-material demand in its operating markets. The screen shows strong EPS growth, suggesting recent earnings momentum has been significant.

Key risk:

Cement is cyclical. Energy costs, FX movements, country risk and construction demand can all affect earnings.

What it does:

ASL Marine is an integrated marine services group involved in shipbuilding, ship repair, ship conversion, chartering and engineering.

Why it may be interesting:

It gives exposure to the marine and offshore cycle. When demand improves, marine companies can see operating leverage.

Key risk:

Marine cycles are volatile. Balance-sheet discipline, order-book quality and execution are critical. Downturns can be sharp if demand weakens.

What it does:

Lum Chang Creations focuses on urban revitalisation, including conservation, restoration, interior fit-out and addition and alteration works.

Why it may be interesting:

It is a niche construction and asset-enhancement play in Singapore. The screen shows strong profitability and earnings growth, which may suggest improving project momentum.

Key risk:

Project-based earnings can be uneven. Investors need to check whether recent growth is recurring, contract-specific or influenced by one-off factors.

What it does:

Thakral is an investment and lifestyle group with exposure to real estate in markets such as Australia, Japan and Singapore, alongside lifestyle and brand distribution businesses.

Why it may be interesting:

It offers a mix of real estate, consumer/lifestyle and potential value-unlocking themes. The screen shows strong earnings growth and high profitability.

Key risk:

The business mix is complex. Investors need to understand whether earnings are recurring or driven by asset valuations, investment gains or one-off factors.

What it does:

XMH provides diesel engines, propulsion systems and power-generation solutions for marine and industrial customers. Its Mech-Power business supplies generator sets for commercial buildings, hospitals, infrastructure projects and data centres.

Why it may be interesting:

It has a second-order link to data-centre infrastructure. Data centres need reliable backup power, and AI workloads are increasing focus on power availability. This makes XMH relevant for investors researching the broader infrastructure layer around AI.

Key risk:

It is not a pure AI stock. Generator demand can be project-based, competitive and margin-sensitive. Liquidity may also be lower given its smaller size.

1. AI is not just about chips

Some names in the screen have indirect exposure to the AI infrastructure buildout. PC Partner links to graphics cards and computing hardware. Frencken and Micro-Mechanics sit closer to semiconductor equipment and precision manufacturing. XMH Holdings has exposure to backup power systems used in data centres.

This does not make these pure AI stocks. It only suggests that AI-related capital expenditure can have second-order links to hardware, precision parts, power systems and infrastructure. Investors should still assess how material these exposures are to each company’s revenue and earnings.

2. Singapore construction is quietly showing up

Names such as Pan-United, Global Resources Construction, OKP Holdings, Lum Chang Creations and Ever Glory United suggest that construction and infrastructure remain active pockets in the local market.

However, construction-linked companies can be exposed to tender competition, labour shortages, materials inflation, project delays and cash-flow volatility. Strong revenue growth does not always translate into strong margins or free cash flow.

3. Commodity and real-asset exposure is present

CNMC Goldmine provides gold exposure, International Cement links to construction materials, and Indofood Agri brings palm oil and food/agri exposure. China Aviation Oil Singapore adds aviation fuel and energy-trading exposure.

These names may behave differently from financials or technology stocks, which can be useful from a diversification perspective. But commodity-linked earnings can also be volatile and exposed to external variables that investors cannot control.

4. Some names are more established, but not risk-free

The Hour Glass, Boustead Singapore, Pan-United and China Aviation Oil Singapore may appeal to investors researching more established business models rather than only high-growth small-cap stories.

That does not remove risk. Consumer demand, segment complexity, construction cycles and commodity-linked trading margins can still affect earnings outcomes.

This screen is only a first cut. Before forming any investment view, investors should assess:

A company can pass a quantitative screen and still be unsuitable if valuation is stretched, earnings are not sustainable, liquidity is thin or the risk profile does not match an investor’s objectives.

The biggest risk is momentum chasing. Many stocks on this list have already rallied strongly. That may reflect improving fundamentals, but it can also mean expectations are already high. If earnings disappoint, momentum can reverse quickly.

Liquidity is another major risk. Some Singapore small and mid caps can have wide bid-ask spreads, limited daily turnover and sharp price gaps. This can make position sizing and exits more difficult, particularly during market stress.

There is also earnings cyclicality. Construction, marine, semiconductors, cement, gold, palm oil and aviation fuel are all exposed to cycles. A strong year can be followed by a weaker one if demand, prices or margins turn.

Finally, investors should remember that quantitative screens do not capture everything. Governance quality, management execution, disclosure standards, customer relationships and capital allocation discipline require manual due diligence.

This Singapore small and mid-cap screen highlights 20 companies where earnings growth, profitability, leverage discipline and share-price momentum currently appear aligned.

The list includes several areas that may be useful for further research: AI infrastructure enablers, semiconductor supply-chain names, construction and infrastructure plays, gold exposure, aviation fuel, luxury consumption and agribusiness.

But the screen should not be interpreted as a recommendation or endorsement. It is a way to narrow a broad universe into a more manageable research list. The next step is to assess whether each company’s valuation, liquidity, earnings quality, governance and risk profile are appropriate.

For investors willing to look beyond the usual STI names, Singapore small and mid caps may offer a broader set of themes. But small-cap investing requires patience, risk control and careful due diligence. The screen may open the door, but the research still has to do the heavy lifting.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy