Key points:

- Macro: US job openings surge and US-Iran peace talks remain uncertain

- Equities: Marvell gains 33% after Jensen’s $1 trillion comment on the firm

- FX: Dollar broadly firm; USDJPY near 160, mixed moves across high‑beta FX

- Commodities: Copper settled at a new record high of $6.6495/lb

- Fixed income: 30-year down in 8 of the past 9 sessions, lowest since 8 May

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- Iranian media questioned the talks’ progress, despite Trump saying they continue, as Washington now seeks written Iranian commitments on nuclear concessions under a preliminary conflict-ending framework that had previously rested on verbal assurances.

- US JOLTS beat: US job openings rose to 7.618 million in April, well above the 7.0 million consensus and up from 6.887 million in March, reinforcing a hawkish read on the Fed's rate path.

- US job quits fell to 2.98 million in April 2026, the lowest since mid-2020, with the quits rate down to 1.9%, signaling fewer workers voluntarily leaving jobs.

- Eurozone inflation rose to 3.2% y/y in May 2026 from 3.0%, the highest since September 2023 and above the ECB’s 2% target. Energy prices surged 10.9% on Middle East–related supply issues, services and goods inflation picked up, food inflation eased, and core inflation climbed to 2.5%, with most major members seeing higher rates except Germany.

- The Economic Optimism Index edged down to 42.5 in June, below the neutral 50 mark for a tenth month. The six-month outlook hit a two-year low, personal financial sentiment stayed near neutral, and confidence in federal policies ticked slightly higher.

Equities:

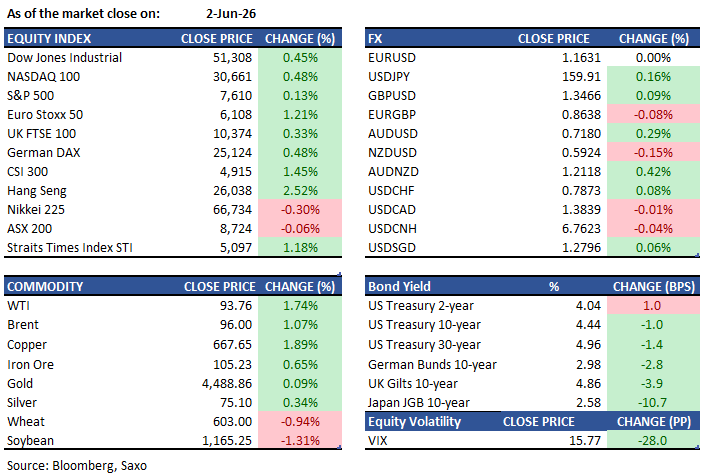

- US — The S&P 500 closed up 0.1% at 7,609.78 on Tuesday, notching a ninth consecutive session of gains — its longest winning streak since May 2025 — and a fresh record high. The Nasdaq 100 advanced 0.5% and the Dow added 0.4%, both also at records. The Philadelphia Semiconductor Index surged 4.5%, led by Marvell Technology (+33%), after Nvidia CEO Jensen Huang suggested it could become the next $1 trillion company. Hewlett Packard Enterprise soared 19.5% after reporting strong results and raising guidance. Alphabet and Anthropic's IPO filing also drew attention. After hours, Palo Alto Networks rose on a raised profit outlook, and GitLab beat on earnings and guided above consensus.

- EU — European equities rebounded on Tuesday, with the Stoxx Europe 600 rising 0.7% to 625.34, its biggest single-day gain in over a week. The Euro Stoxx 50 climbed 1.21% to 6,107.85. The tech sector led gains: STMicroelectronics surged 15.1% after nearly doubling its 2026 data centre revenue forecast to $1 billion, while ASML rose 4.9% and Infineon gained 9.5% to a record high. The DAX added 0.5% and the FTSE 100 rose 0.3%, with Antofagasta the top FTSE mover at +6.5%. Abivax was a notable decliner.

- Asia — Asian equities closed higher on Tuesday, led by Hong Kong. The Hang Seng Index surged 2.5% to 26,038.32, its biggest single-day gain since 8 April, driven by Tencent (+10.5%) after reports it is moving closer to launching an AI agent on WeChat. The Hang Seng Tech Index jumped 3.4%, with Meituan also rallying on narrower-than-expected losses. Macau casino stocks extended gains — MGM China +7.2%, Wynn Macau +5.8% — following a gaming revenue beat. Lenovo hit a record high after Macquarie raised its price target by over 70%. The HSCEI gained 3% and the CSI 300 rose 1.5%. The Kospi ended higher after recovering from sharp intraday losses. The Nikkei, STI and broader MSCI Asia Pacific Index also advanced, with the regional benchmark heading for a record, supported by falling crude prices and continued AI-related enthusiasm.

Earnings this week:

- Wednesday: Broadcom, Inditex, CrowdStrike, Medtronic, Veeva Systems

- Thursday: Ciena, Samsara, Planet Labs, Lululemon, Rubrik

- Friday: Sectra, Mr Price Group, ABM Industries, Foschini Group

FX:

- USD is broadly supported, with the main focus on USDJPY, which is grinding higher toward the key 160 level and trading at its strongest since late April, near prior Japanese intervention territory. The move is underpinned by strong US labor-market data (job openings) and safe-haven/oil dynamics linked to the US–Iran conflict, which has pushed WTI toward $95/bbl.

- USDMXN fell 0.44% to 17.2885, its largest one-day USD decline versus MXN since May 20.

- AUDUSD was flat to slightly higher and remains up about 0.8% since the US–Iran conflict began, though Australia’s Q1 GDP is a key near-term risk that could hit AUD if it disappoints.

- EURUSD is struggling for upside as higher oil prices and the broader bid for the dollar outweigh any support from Eurozone inflation data, trading around 1.1630 and leaving GBPEUR largely unchanged.

- NZDUSD is under pressure amid firm US labor data, trading around 0.5930.

Commodities:

- Copper settled at a new record high of $6.6495 per pound, up 4.6% over two sessions and 38% year-on-year. Demand continues to outpace global supply, with AI infrastructure build-out a key driver. The US Commerce Department faces a 30 June deadline to deliver an updated recommendation on copper import tariffs, keeping bullish sentiment elevated.

- Gold steadied around $4,475/oz after falling 1.9% on Monday to start June. Prices remain captive to Iran headlines, with ongoing conflict uncertainty providing a floor, though elevated inflation has reduced gold's appeal as a financial instrument in the near term.

- Oil edged higher as the US-Iran standoff showed no visible progress toward reopening the Strait of Hormuz. WTI July futures firmed, keeping energy prices elevated and contributing to broader inflationary pressures globally.

Fixed income:

- US Treasuries were broadly steady, with the 10-year yield little changed at 4.453% and the 30-year yield slipping 0.7bps to 4.966%. The 30-year has now fallen in eight of the past nine sessions and sits at its lowest since 8 May, having pulled back from a 52-week high of 5.18% hit on 19 May. Front-end yields are pricing the risk of a renewed Fed hiking cycle, with the 2-year at 4.051%.

- Fed rate path repricing is the dominant driver of the Treasury curve, according to Pimco, which argues the recent rise in long-dated yields is primarily about shifting policy expectations rather than AI-related term premium. Cleveland Fed's Hammack reinforced the hawkish tone, flagging that action may be needed soon if inflation trends persist.

- German Bunds saw the 10-year yield testing the 3% level again, a key technical threshold flagged by Danske Bank. The ECB is widely expected to hike rates at next week's meeting following the May CPI print of 3.2%, adding upward pressure to European sovereign yields.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.

Key points:

- Macro: US job openings surge and US-Iran peace talks remain uncertain

- Equities: Marvell gains 33% after Jensen’s $1 trillion comment on the firm

- FX: Dollar broadly firm; USDJPY near 160, mixed moves across high‑beta FX

- Commodities: Copper settled at a new record high of $6.6495/lb

- Fixed income: 30-year down in 8 of the past 9 sessions, lowest since 8 May

------------------------------------------------------------------

<Table with Source>

Disclaimer: Past performance does not indicate future performance.

Macro:

- Iranian media questioned the talks’ progress, despite Trump saying they continue, as Washington now seeks written Iranian commitments on nuclear concessions under a preliminary conflict-ending framework that had previously rested on verbal assurances.

- US JOLTS beat: US job openings rose to 7.618 million in April, well above the 7.0 million consensus and up from 6.887 million in March, reinforcing a hawkish read on the Fed's rate path.

- US job quits fell to 2.98 million in April 2026, the lowest since mid-2020, with the quits rate down to 1.9%, signaling fewer workers voluntarily leaving jobs.

- Eurozone inflation rose to 3.2% y/y in May 2026 from 3.0%, the highest since September 2023 and above the ECB’s 2% target. Energy prices surged 10.9% on Middle East–related supply issues, services and goods inflation picked up, food inflation eased, and core inflation climbed to 2.5%, with most major members seeing higher rates except Germany.

- The Economic Optimism Index edged down to 42.5 in June, below the neutral 50 mark for a tenth month. The six-month outlook hit a two-year low, personal financial sentiment stayed near neutral, and confidence in federal policies ticked slightly higher.

Equities:

- US — The S&P 500 closed up 0.1% at 7,609.78 on Tuesday, notching a ninth consecutive session of gains — its longest winning streak since May 2025 — and a fresh record high. The Nasdaq 100 advanced 0.5% and the Dow added 0.4%, both also at records. The Philadelphia Semiconductor Index surged 4.5%, led by Marvell Technology (+33%), after Nvidia CEO Jensen Huang suggested it could become the next $1 trillion company. Hewlett Packard Enterprise soared 19.5% after reporting strong results and raising guidance. Alphabet and Anthropic's IPO filing also drew attention. After hours, Palo Alto Networks rose on a raised profit outlook, and GitLab beat on earnings and guided above consensus.

- EU — European equities rebounded on Tuesday, with the Stoxx Europe 600 rising 0.7% to 625.34, its biggest single-day gain in over a week. The Euro Stoxx 50 climbed 1.21% to 6,107.85. The tech sector led gains: STMicroelectronics surged 15.1% after nearly doubling its 2026 data centre revenue forecast to $1 billion, while ASML rose 4.9% and Infineon gained 9.5% to a record high. The DAX added 0.5% and the FTSE 100 rose 0.3%, with Antofagasta the top FTSE mover at +6.5%. Abivax was a notable decliner.

- Asia — Asian equities closed higher on Tuesday, led by Hong Kong. The Hang Seng Index surged 2.5% to 26,038.32, its biggest single-day gain since 8 April, driven by Tencent (+10.5%) after reports it is moving closer to launching an AI agent on WeChat. The Hang Seng Tech Index jumped 3.4%, with Meituan also rallying on narrower-than-expected losses. Macau casino stocks extended gains — MGM China +7.2%, Wynn Macau +5.8% — following a gaming revenue beat. Lenovo hit a record high after Macquarie raised its price target by over 70%. The HSCEI gained 3% and the CSI 300 rose 1.5%. The Kospi ended higher after recovering from sharp intraday losses. The Nikkei, STI and broader MSCI Asia Pacific Index also advanced, with the regional benchmark heading for a record, supported by falling crude prices and continued AI-related enthusiasm.

Earnings this week:

- Wednesday: Broadcom, Inditex, CrowdStrike, Medtronic, Veeva Systems

- Thursday: Ciena, Samsara, Planet Labs, Lululemon, Rubrik

- Friday: Sectra, Mr Price Group, ABM Industries, Foschini Group

FX:

- USD is broadly supported, with the main focus on USDJPY, which is grinding higher toward the key 160 level and trading at its strongest since late April, near prior Japanese intervention territory. The move is underpinned by strong US labor-market data (job openings) and safe-haven/oil dynamics linked to the US–Iran conflict, which has pushed WTI toward $95/bbl.

- USDMXN fell 0.44% to 17.2885, its largest one-day USD decline versus MXN since May 20.

- AUDUSD was flat to slightly higher and remains up about 0.8% since the US–Iran conflict began, though Australia’s Q1 GDP is a key near-term risk that could hit AUD if it disappoints.

- EURUSD is struggling for upside as higher oil prices and the broader bid for the dollar outweigh any support from Eurozone inflation data, trading around 1.1630 and leaving GBPEUR largely unchanged.

- NZDUSD is under pressure amid firm US labor data, trading around 0.5930.

Commodities:

- Copper settled at a new record high of $6.6495 per pound, up 4.6% over two sessions and 38% year-on-year. Demand continues to outpace global supply, with AI infrastructure build-out a key driver. The US Commerce Department faces a 30 June deadline to deliver an updated recommendation on copper import tariffs, keeping bullish sentiment elevated.

- Gold steadied around $4,475/oz after falling 1.9% on Monday to start June. Prices remain captive to Iran headlines, with ongoing conflict uncertainty providing a floor, though elevated inflation has reduced gold's appeal as a financial instrument in the near term.

- Oil edged higher as the US-Iran standoff showed no visible progress toward reopening the Strait of Hormuz. WTI July futures firmed, keeping energy prices elevated and contributing to broader inflationary pressures globally.

Fixed income:

- US Treasuries were broadly steady, with the 10-year yield little changed at 4.453% and the 30-year yield slipping 0.7bps to 4.966%. The 30-year has now fallen in eight of the past nine sessions and sits at its lowest since 8 May, having pulled back from a 52-week high of 5.18% hit on 19 May. Front-end yields are pricing the risk of a renewed Fed hiking cycle, with the 2-year at 4.051%.

- Fed rate path repricing is the dominant driver of the Treasury curve, according to Pimco, which argues the recent rise in long-dated yields is primarily about shifting policy expectations rather than AI-related term premium. Cleveland Fed's Hammack reinforced the hawkish tone, flagging that action may be needed soon if inflation trends persist.

- German Bunds saw the 10-year yield testing the 3% level again, a key technical threshold flagged by Danske Bank. The ECB is widely expected to hike rates at next week's meeting following the May CPI print of 3.2%, adding upward pressure to European sovereign yields.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.