Outrageous Predictions

A Fortune 500 company names an AI model as CEO

Charu Chanana

Chief Investment Strategist

Can AI be trusted to take over in the boardroom? With the right algorithms and balanced human oversi...

Key points:

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

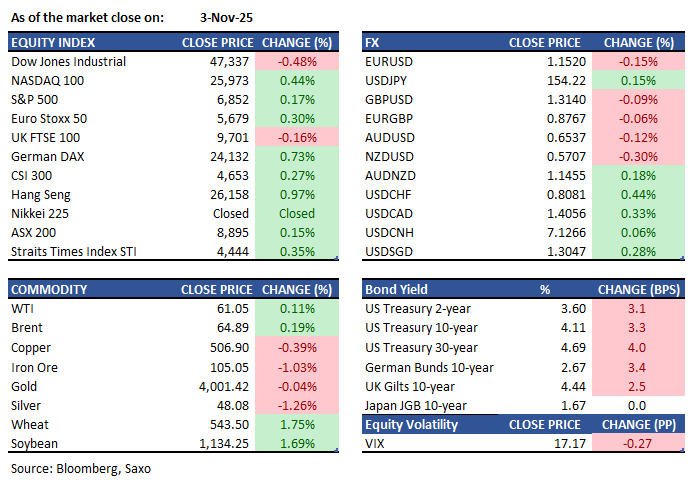

Macro:

Equities:

Earnings this week:

Tuesday

Asia: Nintendo, Mitsubishi, NTT Inc

Outside Asia: Uber Technologies, Pfizer, Shopify, Super Micro Computer, Spotify, Yum! Brands, AMD

Wednesday

Asia: Hong Kong Exchange, Toyota, Itochu, Softbank, Mitsui & Co.

Outside Asia: Robinhood Markets, Qualcomm, AppLovin, DoorDash, McDonald’s, Lyft, ARM, Novo Nordisk

Thursday

Asia: Recruit, Suzuki Motor, DBS

Outside Asia: Warner Bros. Discovery, DraftKings, Block, Moderna. AirBnB

Friday

Asia: Mitsubishi Heavy Industries; OCBC; Honda; Macquarie; Fujikura

Outside Asia: Constellation Energy, KKR

FX:

Commodities:

Fixed income:

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy