Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Your first stock trade — or even your first few stock trades — is an important step. But a portfolio made only of stocks can still be exposed to one asset class, and often to the same market drivers.

Once you have started investing, the next question is not simply “what should I buy next?” A better question is: how do I build beyond stocks in a more thoughtful way?

Markets do not reward the same exposures every quarter. Multi-asset investing is less about chasing returns and more about building a portfolio that can behave through different regimes, especially when drawdowns test decision-making.

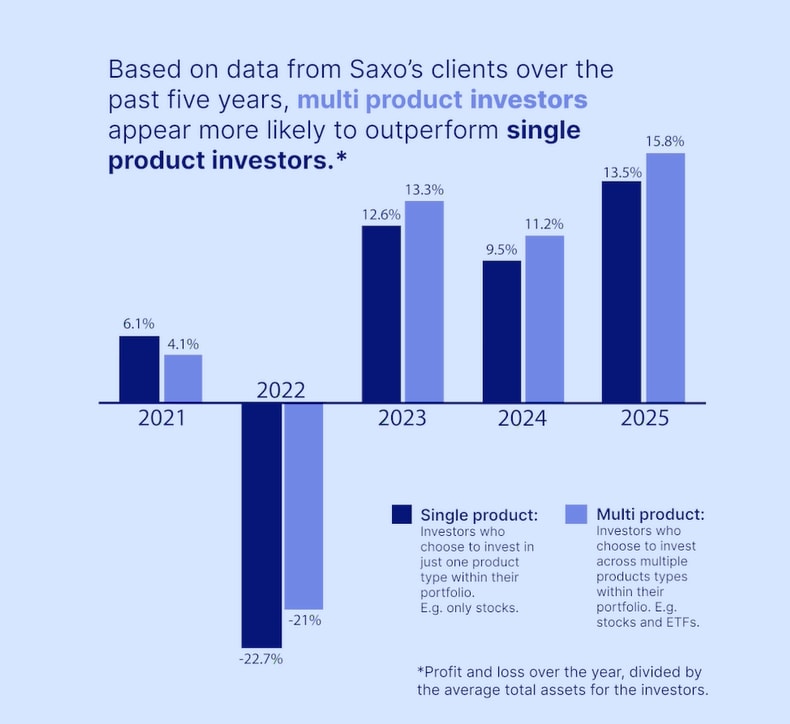

An interesting insight from aggregated Saxo client activity over the past five years: clients who used more than one product type were more likely to have higher profitability outcomes than clients who only used one product type, such as stocks only.

Note: Past performance is not indicative of future results.

Source: Saxo client data.

This is an association, not proof that using multiple products causes better results. But there are sensible reasons why broader portfolios may lead to better outcomes: a smoother ride can help investors stay invested through drawdowns; different environments reward different exposures; and adding another product type can reduce hidden concentration in one stock, sector, region or theme.

The practical takeaway: a broader toolkit can give investors more ways to respond when market leadership shifts, and may reduce the risk that one stock, sector or theme dominates portfolio outcomes.

That does not mean a full portfolio rebuild. It can start with one additional building block — such as ETFs for broader exposure, using Shortlists to track current themes, learning collateralised options strategies for shares they own, exploring securities lending where available, or understanding CFDs and margin lending before using leverage — which we explore in the sections below.

Buying individual stocks can be exciting because the story is clear: a company, a product, a founder, an earnings result, or a market theme.

But single stocks also come with single-company risk. Earnings disappointment, management changes, regulation, currency moves, or sector rotation can all affect one stock sharply.

That is where ETFs can help.

ETFs allow investors to access a basket of securities in one trade. They can be used to gain exposure to:

For many investors, ETFs can be a useful way to build a portfolio core, while individual stocks become more targeted satellite positions.

Risk to consider: ETFs can still fall in value, especially during broad market selloffs, and thematic or sector ETFs may be concentrated in a narrow set of risks.

How to think about it: If your first trade was a single stock, ask whether your portfolio depends too much on one company, one sector or one country. ETFs may help broaden that exposure.

Explore next: ETF ideas and diversified market exposure.

Markets move quickly. One week, investors may be focused on AI and semiconductor earnings. The next, the focus could shift to central banks, oil prices, banks, defence, China, Japan, gold or dividend stocks.

Shortlists can help investors keep track of the themes currently driving market attention.

They are not a recommendation to buy or sell. Instead, they can be used as a starting point for research, helping investors compare names within a theme and understand where market interest is building.

Shortlists can be useful if you want to explore:

Risk to consider: Shortlists may highlight popular or timely themes, but market attention can reverse quickly, and not every theme will suit every investor’s risk profile or time horizon.

How to think about it: If you are not sure what to research next, start with the themes the market is already watching. Then ask whether the idea fits your risk profile, time horizon and portfolio needs.

Explore next: Curated Shortlists across stocks, ETFs and market themes.

Some investors who already own shares use options to manage their stock exposure in more advanced ways.

A simpler starting point may be to first understand put options. A put option gives the holder the right to sell a stock at a set price before expiry. For investors, this matters because puts are often linked to two useful concepts: downside protection and disciplined entry levels.

From there, investors can learn about income strategies such as covered calls. A covered call involves selling a call option on shares already owned. The investor receives option premium upfront, but the trade-off is that upside may be capped if the stock rises above the strike price. The shares may also be called away.

Another example is a cash-secured put, which is also commonly used as an income strategy. This involves selling a put option on a stock an investor may be willing to buy at a lower price, while keeping enough cash aside in case the shares are assigned. The investor receives premium upfront, but may be required to buy the stock if it falls below the strike price.

Options can be useful portfolio tools, but they are not beginner products.

Risk to consider: Options involve specific risks, including assignment risk, missed upside, downside exposure, early exercise, expiry dates, strike prices and premium. They may not be suitable for all investors.

How to think about it: Start with the basics: what is a put, what is a call, what is a strike price, and what happens at expiry. Then move to collateralised strategies such as cash-secured puts and covered calls, where the risks and trade-offs must be clearly understood before placing any options trade.

Explore next: Options education, put options, cash-secured puts and covered calls.

Investors who already hold stocks or ETFs may also be able to earn additional income by lending eligible securities, where this service is available.

With securities lending, eligible holdings may be lent to other market participants, typically in exchange for lending income. The investor still has market exposure to the underlying security, while potentially earning an additional return from holdings they were already planning to keep.

This can be useful for long-term investors who want to make their existing portfolio work a little harder, without necessarily changing their market view or selling their holdings.

Risk to consider: Securities lending involves risks, including counterparty risk, collateral risk, possible delays in recall, and differences in how dividends, voting rights or corporate actions may be treated. Income is not guaranteed and availability may vary by security and market.

How to think about it: Securities lending may be worth understanding if you already hold stocks or ETFs for the longer term and want to explore potential incremental income. It should still be reviewed carefully, especially the risks, eligibility, and how income is calculated.

Explore next: Securities lending basics and eligible holdings.

Some investors use leveraged products or borrowing tools to increase market exposure or act on short-term opportunities. These tools can create flexibility, but they also increase risk.

CFDs

Contracts for Difference, or CFDs, allow traders to take a view on price moves without owning the underlying asset. They can be used to trade both rising and falling markets, and often provide access to stocks, indices, commodities, FX and other markets.

Because CFDs are leveraged, a smaller amount of capital can control a larger market exposure. This means gains can be amplified, but losses can also be amplified. Losses may exceed the initial amount committed.

CFDs are generally more suited to active traders who understand position sizing, stop losses, market volatility and leverage risk.

Risk to consider: CFDs are leveraged products, so losses can be magnified and may exceed the initial amount committed.

Margin lending

Margin lending allows eligible clients to borrow against their existing portfolio, using eligible holdings as collateral. This can provide additional buying power without first selling existing investments.

This flexibility can be useful in some situations, but borrowing has costs.

Risk to consider: If markets move against the portfolio, losses can be magnified and clients may need to add funds, reduce positions, or face forced selling.

How to think about it: Leverage should be considered only after understanding the risks, costs, and how it fits your investment or trading plan.

Explore next: CFD education and margin lending basics.

Your first stock trade is a starting point, not the full journey.

The next layer depends on what you are trying to achieve:

Markets will always offer new ideas. The key is to build in a way that matches your goals, risk appetite and time horizon.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy