Outrageous Predictions

A Fortune 500 company names an AI model as CEO

Charu Chanana

Chief Investment Strategist

Can AI be trusted to take over in the boardroom? With the right algorithms and balanced human oversi...

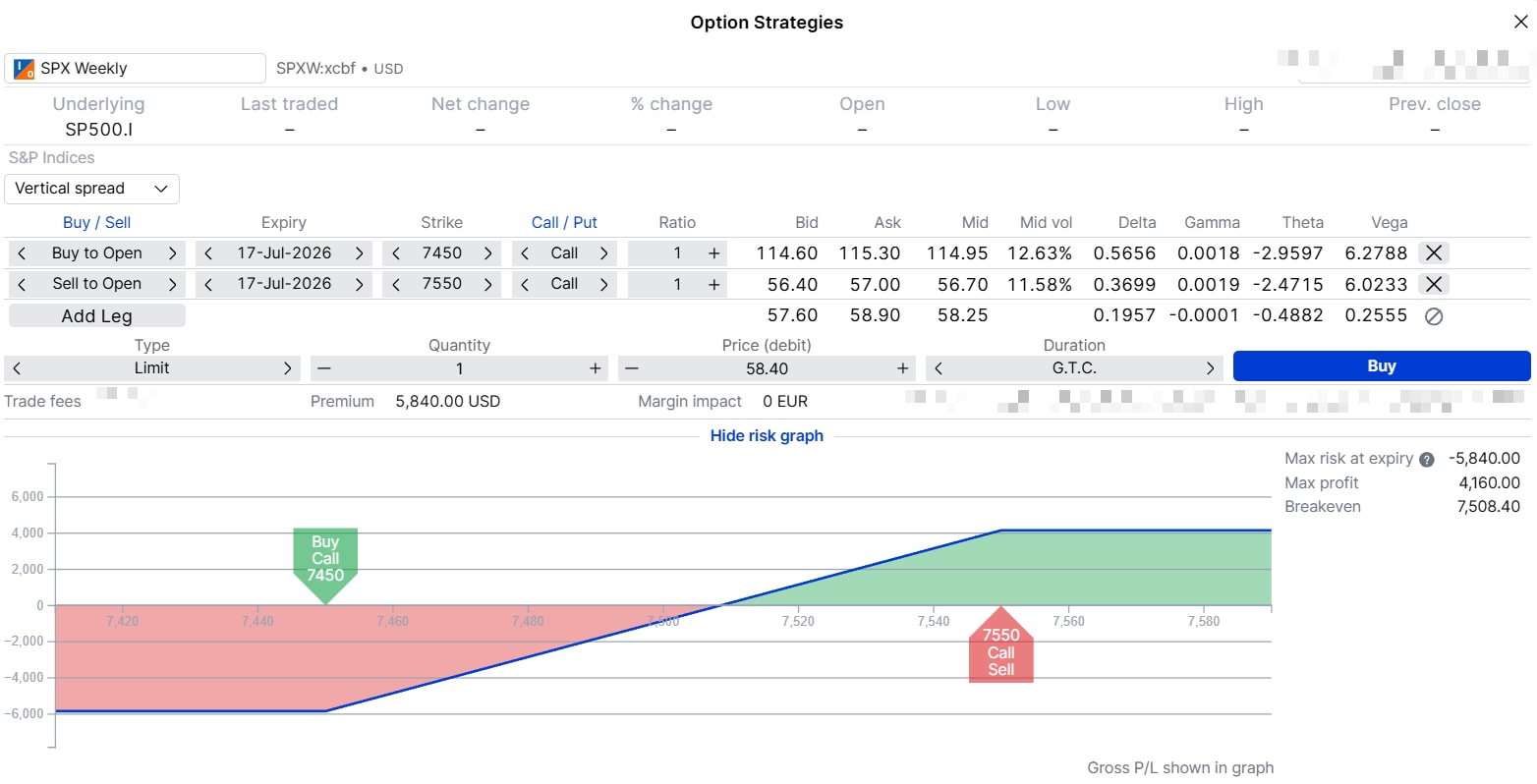

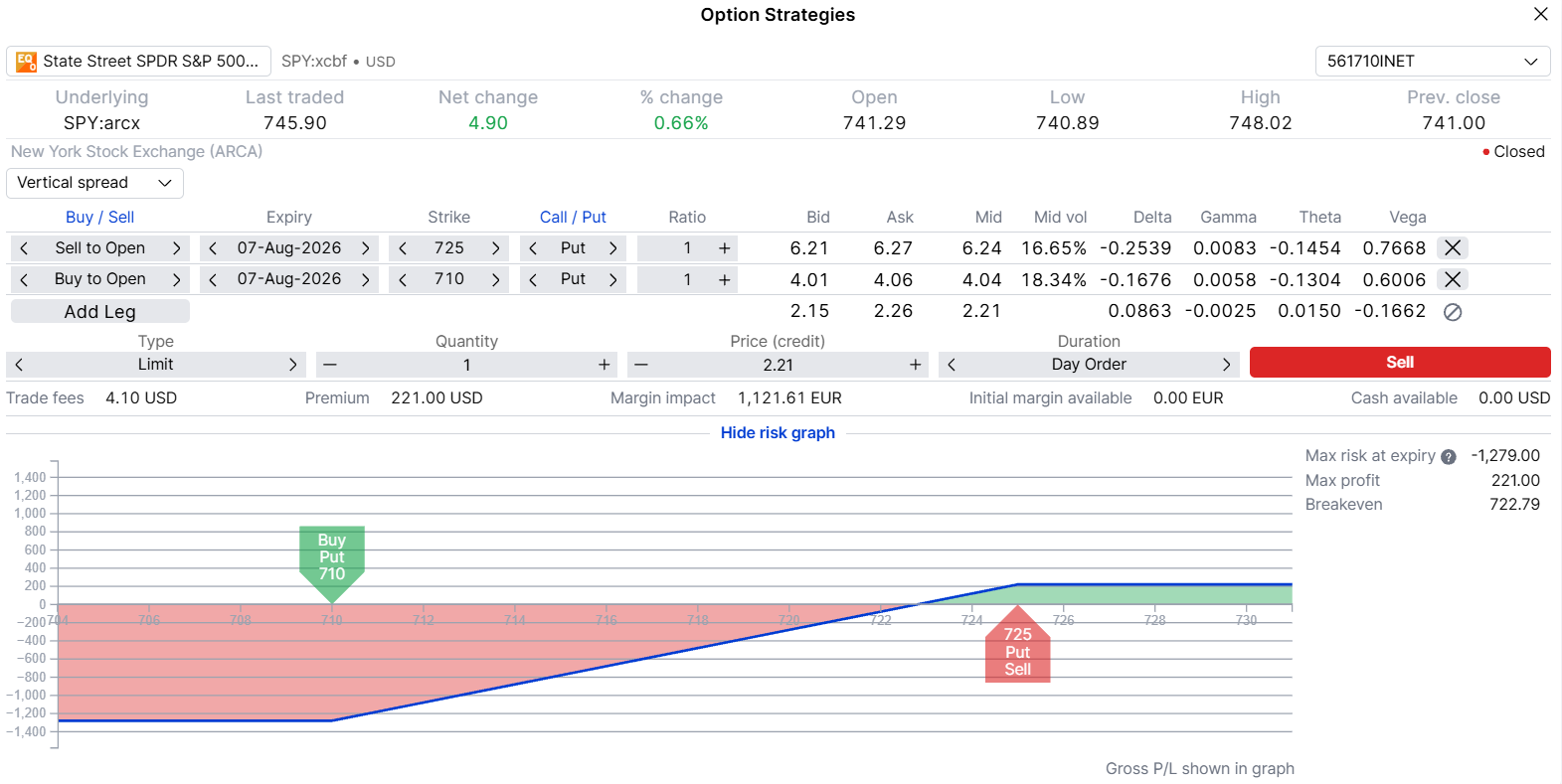

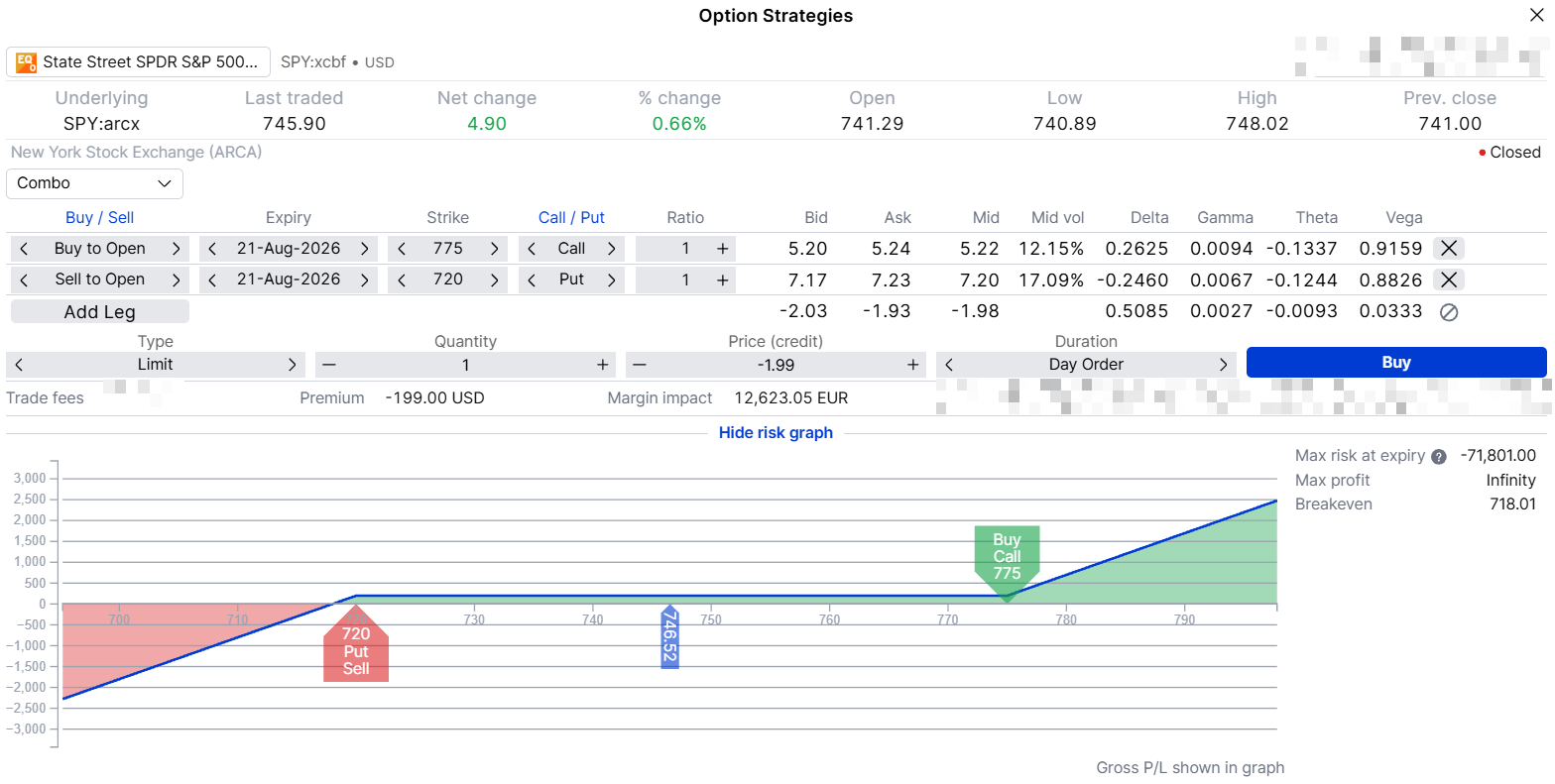

Summary: Q2 earnings season arrives in waves - banks on 14 July, mega-cap tech 29-31 July - and SPXW weekly options have a specific expiry mapped almost exactly onto each window. This article presents three structures for three views: a defined-cost call spread for bank week, a credit-generating put spread for tech week, and a SKEW-informed risk reversal for the full season.

Earnings season has a schedule. And the schedule is the edge.

JPMorgan reports on 14 July. Goldman Sachs and Citigroup follow on 15 July. Then two weeks of quiet before Alphabet, Meta, Microsoft, and Amazon all report within 72 hours of each other in late July. Three distinct windows – and SPXW and SPY weekly options have a specific expiry for each: July 17, August 7, August 21. None of the structures below require a position in any individual stock.

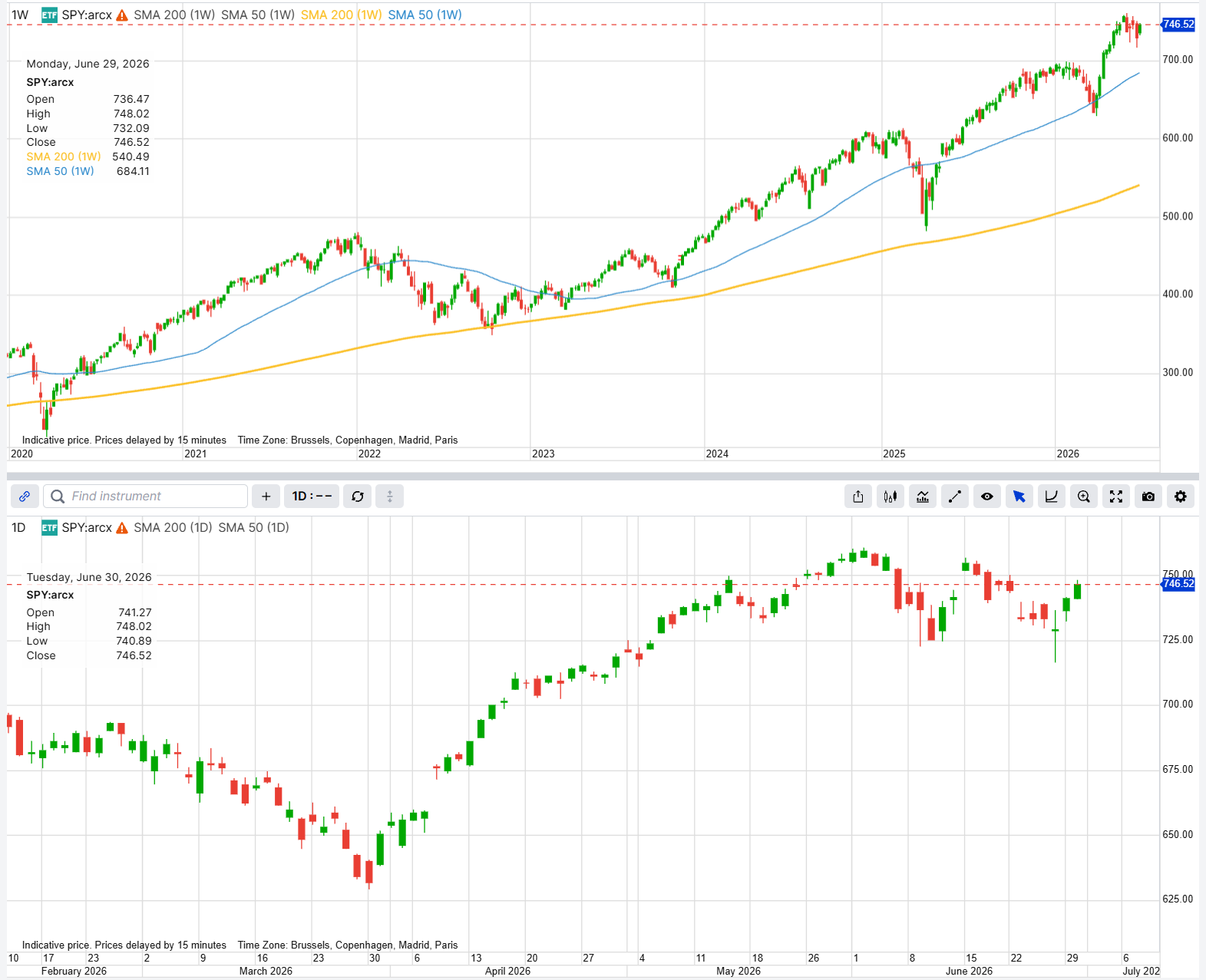

SPY weekly and daily chart, 30 June 2026 close. Source: SaxoTrader, 1 July 2026. Prices shown reflect the close of 30 June 2026 and will differ at the time of publication.

JPMorgan Chase reports before the open on 14 July; Goldman Sachs and Citigroup follow on 15 July. The SPXW July 17 expiry closes two trading days later. A bull call spread on the index using this expiry is a directional position on how the market absorbs those results – defined maximum loss, no single-stock binary exposure.

Alphabet and Meta are expected to report on 29 July. Microsoft on 30 July. Amazon on 31 July. Technology sector earnings growth for Q2 2026 is projected near 43.6% year-over-year. The CBOE SKEW Index closed at 144.46 on 30 June – elevated put premium relative to equidistant calls. A bull put spread sells that SKEW-inflated premium and defines the maximum loss with a lower-strike put.

VIX closed at 17.65 on 30 June; SKEW closed at 144.46. Out-of-the-money puts are carrying more implied volatility than equidistant calls: the $720 put (3.6% OTM) at roughly 17.09% versus the $775 call (3.8% OTM) at roughly 12.15% – a gap of 4.9 percentage points. A risk reversal sells the more expensive put and funds the call with the proceeds, generating a net credit from that asymmetry.

Important: this is an undefined-risk structure and carries substantially more risk than the two defined-risk strategies above. The short put carries uncapped downside below $720 – unlike strategies 1 and 2, where maximum loss is fixed at entry. The maximum acceptable loss must be set as a hard stop before entry (using stop-loss orders). That stop does not change after the position is on.

Illustrative only. This structure carries no assumption about the direction of the index. It is a view that the index will not fall significantly below $720 by 21 August – and that should a sustained rally materialise, the long call captures it at reduced net cost, funded by the SKEW asymmetry.

Bank earnings open on 14 July. Tech week follows, with Alphabet, Meta, Microsoft, and Amazon reporting 29–31 July. The calendar is public – but the index options market is where that calendar is priced. Selecting the right expiry for the right window converts a public schedule into a structured position.

Options prices and greeks in this article are drawn from live SaxoTrader data captured on 1 July 2026. SPY and SPXW prices reflect the 30 June 2026 close. Prices will differ at the time of reading and at the time of trading – always verify live pricing via your broker before entering any position.

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The Author is permitted to wait at least 24 hours from the time of the publication before they trade the instruments themselves.

The author does not hold positions in any of the instruments mentioned in this article at the time of publication.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with a view to providing clients with valuable information and options.

This content will not be changed or subject to review after publication.

| More from the author |

|---|

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Chief Investment Strategist