Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

Summary: ArcelorMittal reports earnings on Thursday, and the options market is already pricing a move of more than 10%. That is the starting point for this case study. In this article, I walk through how to read the expected move from option chain data, how to structure a range-bound view using an iron condor, and why defined risk is not the same as low risk.

ArcelorMittal reports earnings on Thursday, and for investors looking at the shares through an options lens, the key question is not only whether the company beats or misses expectations. It is also whether the share price moves more, or less, than the options market is already pricing in.

For this article, we use ArcelorMittal’s Amsterdam-listed shares and options. ArcelorMittal is a dual-listed stock, with active trading in Amsterdam and in the US through its ADR listing. Options are available in both markets, but based on the open interest shown in the option chains, the Amsterdam listing appears to offer the more liquid options market for this specific case study.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

ArcelorMittal’s Amsterdam-listed shares were trading around EUR 50.60 in the latest snapshot. The longer-term trend still looks constructive, with the shares above their 200-day and 200-week moving averages, but the stock has also become much more volatile after its strong rally and subsequent pullback. That makes it a useful educational case study for earnings trading.

ArcelorMittal’s Amsterdam-listed shares remain above their longer-term moving averages, even after a sharp pullback from earlier highs. Source: SaxoTrader

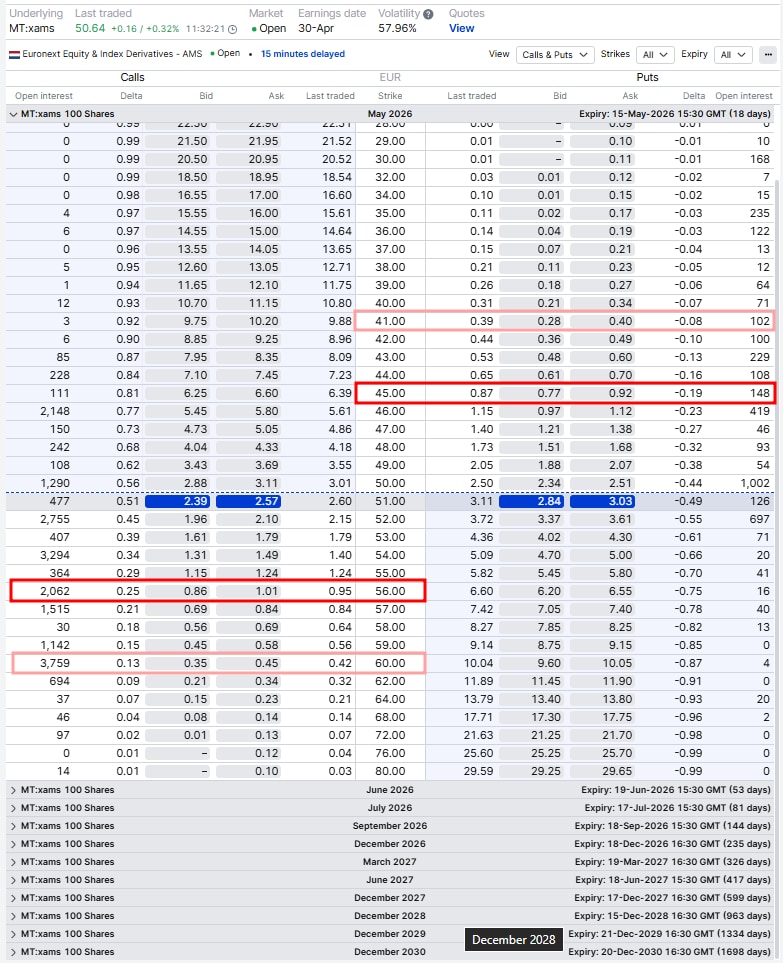

Using the 15 May monthly options, the near-the-money 51-strike call and put trade at a combined midpoint of roughly EUR 5.43. With the share price near EUR 50.60, that suggests the options market is pricing a broad move of a little over 10% by expiry. In simple terms, that points to a rough range of about EUR 45 on the downside and EUR 56 on the upside.

Using the 15 May monthly options, the near-the-money 51-strike call and put imply a broad range of roughly EUR 45 to EUR 56 by expiry. Source: SaxoTrader

This expected move is an estimate, not a forecast. It does not say whether the shares should rise or fall. It simply gives traders a market-implied range to compare against their own view. That distinction matters around earnings, because a trader can be correct about the company’s direction but still be disappointed if the share-price move is smaller than the options market had priced in.

Investors who have a clear directional view could use other defined-risk structures. A bullish investor could consider a bull call spread, while a bearish investor could consider a bear put spread. Those strategies are designed for traders who want to express a clearer view on direction.

This article isolates a different view for educational purposes: what if the options market is already pricing enough movement, and the shares stay broadly within the expected range after earnings? One way to structure that view is with an iron condor.

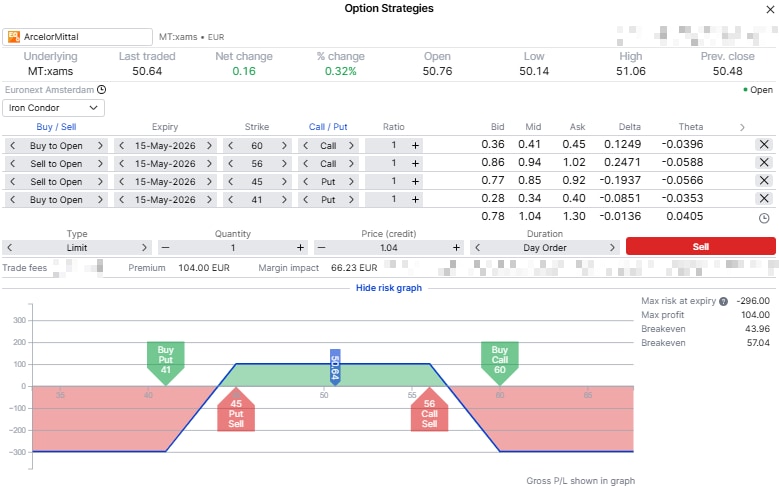

In the example shown here, the structure uses the 15 May expiry with a long 41 put, a short 45 put, a short 56 call, and a long 60 call. In practical terms, the trade sells a defined-risk put spread below the market and a defined-risk call spread above the market.

The position brings in a net credit of about EUR 1.04 per share, or roughly EUR 104 per standard contract covering 100 shares, before costs. The short strikes are at EUR 45 and EUR 56, broadly around the expected range shown by the options market.

This example iron condor uses short strikes at EUR 45 and EUR 56, with long wings at EUR 41 and EUR 60, creating defined risk on both sides. Source: SaxoTrader

The maximum profit is the premium received. In this example, that is about EUR 104 before costs. This maximum profit is achieved if ArcelorMittal closes between the two short strikes, EUR 45 and EUR 56, at expiry, so that both short options expire worthless.

The maximum risk is defined by the width of either spread minus the premium received. Both spreads are EUR 4 wide: the put spread is between EUR 41 and EUR 45, and the call spread is between EUR 56 and EUR 60. A EUR 4-wide spread equals EUR 400 of maximum spread exposure per standard contract covering 100 shares. After subtracting the EUR 104 premium received, the maximum risk is about EUR 296 before costs.

The breakeven levels are also based on the short strikes and the premium received. The lower breakeven is the short put strike minus the premium received, or roughly EUR 45 minus EUR 1.04, which gives about EUR 43.96. The upper breakeven is the short call strike plus the premium received, or roughly EUR 56 plus EUR 1.04, which gives about EUR 57.04.

This iron condor is designed around a range-bound view. The ideal outcome is that ArcelorMittal’s earnings reaction is smaller than the market-implied move, implied volatility falls after the event, and the shares remain between the short strikes.

The risk is that earnings trigger a larger move than expected. If the shares fall below EUR 45 or rise above EUR 56, losses start to build. If the move continues toward the long put at EUR 41 or the long call at EUR 60, the trade can approach its maximum loss.

This is why an iron condor is not a low-risk trade simply because risk is defined. Defined risk means the maximum loss is known in advance. It does not mean the probability or size of loss is small.

A more aggressive version of this range-bound idea would be a short strangle. In simple terms, that means selling the out-of-the-money put and call without buying the protective wings. In this example, it would be similar to removing the long 41 put and long 60 call from the iron condor.

The advantage is that the trader receives more premium and has more flexibility to manage the position. The trade-off is much greater risk, because the position no longer has defined maximum loss. A sharp move after earnings can therefore become very costly. Short strangles require strong risk management and a clear adjustment plan. Without that, the higher premium can quickly become an expensive lesson.

The useful lesson is that earnings trading is not only about being right on the company. It is about matching the view to the structure. Direction matters, but so do the expected move, implied volatility, time to expiry, liquidity, and the size of the defined risk.

This ArcelorMittal example is therefore not presented as the preferred way to trade the earnings event. It is a practical case study showing how an iron condor can be used to express one specific educational view: that the post-earnings move may remain inside the range already implied by the options market.

The expected move is an estimate of how much the options market is pricing for the share price by a certain expiry date. In this case, the 15 May options suggest a broad move of roughly 10% around the current share price. It is not a prediction of direction.

ArcelorMittal trades both in Amsterdam and in the US through its ADR listing. Options are available in both markets, but the Amsterdam-listed options show higher open interest in the chain used for this article, making them the more relevant market for this educational example.

An iron condor is an options strategy that combines a short put spread below the market and a short call spread above the market. It is designed for a range-bound view and has defined maximum profit and defined maximum risk.

An iron condor can work when the share price stays between the short strikes and the premium received is not offset by an adverse price move. Around earnings, it may also benefit if implied volatility falls after the event, but only if the share-price move remains contained.

The main risk is a larger-than-expected move. If the share price moves beyond one of the short strikes, losses can build. The long options limit the maximum loss, but they do not prevent the position from losing money.

Each spread is EUR 4 wide. With a standard contract covering 100 shares, that equals EUR 400 of maximum spread exposure. The position receives about EUR 104 in premium, so the maximum risk is approximately EUR 400 minus EUR 104, or EUR 296 before costs.

A short strangle can collect more premium because it does not include the protective long options. However, that also means the maximum risk is not defined. It may offer more flexibility for experienced traders, but it requires disciplined risk management and can be dangerous if the share price moves sharply after earnings.

A trader with a clearly bullish view could consider a bull call spread, while a trader with a bearish view could consider a bear put spread. Those structures are also defined-risk strategies, but they express a more directional view than the iron condor discussed in this article.

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy