Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

Summary: Most investors think about portfolios in terms of what they own. Options allow them to shape how those holdings actually behave - across three distinct objectives: growth, protection, and income. This article explains which approach fits which investor type, and what each one honestly costs.

Most investors ask which option to trade. The more useful question is what they want their portfolio to do differently.

Long-term portfolios are not all built the same way. Some are designed to compound – equities held for appreciation, time horizon measured in decades. Others are built around income: dividend-paying stocks, a preference for cash flow over capital growth. And some investors have reached a stage where protecting what they have built matters more than adding to it. The traditional 60/40 portfolio – an allocation of roughly 60% equities for growth and 40% bonds for stability and income – is a widely used starting framework, but the mix of priorities varies considerably from one investor to the next.

That distinction matters when adding options, because the approach that works well for a growth-focused portfolio can actively work against an income-focused one. Options interact with a portfolio; they do not sit alongside it neutrally. The starting question is not “which strategy?” but “what is my portfolio actually trying to do?”

Three answers are worth exploring: growth, protection, and income.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

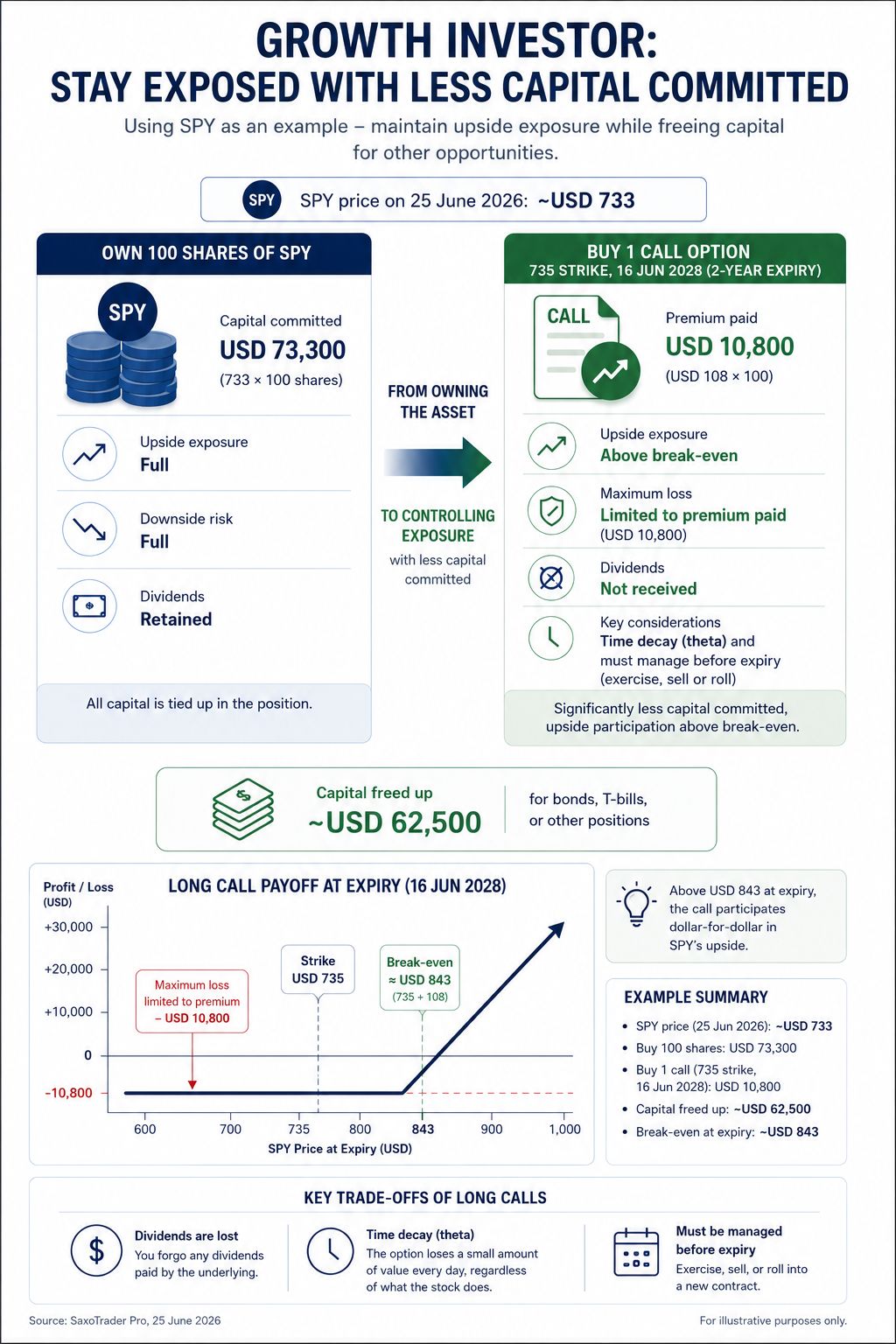

Think of an investor in their late twenties or early thirties – early career, regular income coming in, decades of compounding ahead. The priority is equity exposure. Downside tolerance is relatively higher because time absorbs setbacks in a way it cannot for someone closer to retirement.

For this investor, replacing part of a stock holding with long calls is worth understanding. Instead of committing the full purchase price to a position, the investor buys a call option – a time-limited right to benefit from price appreciation – and keeps the remaining capital deployable elsewhere. The maximum loss is the premium paid; upside above the break-even follows the underlying.

A concrete illustration using SPY (the SPDR S&P 500 ETF Trust): with SPY trading at approximately USD 733 on 25 June 2026, buying 100 shares requires a commitment of roughly USD 73,300. A call at the 735 strike for the 16 June 2028 expiry – a two-year horizon more in keeping with a long-term investor’s outlook – was quoted at approximately USD 108 per share, USD 10,800 per contract (Source: SaxoTrader Pro, 25 June 2026). That frees roughly USD 62,500 for bonds, T-bills, or other positions, while maintaining directional exposure to SPY above the break-even of approximately USD 843 at expiry.

Growth investor: long call on SPY, 735 strike, 16 June 2028 expiry – defined maximum loss of USD 10,800, capital freed approximately USD 62,500. Source: SaxoTrader Pro, 25 June 2026. For illustrative purposes only. Source: Saxo.

Three costs come with this structure: dividends are lost, the position loses a small amount of value every day regardless of what the stock does, and the call must be managed before expiry – exercised, sold, or rolled into a new contract. For a growth investor who accepts those trade-offs and values capital efficiency, the structure fits.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it's crucial to make informed decisions.

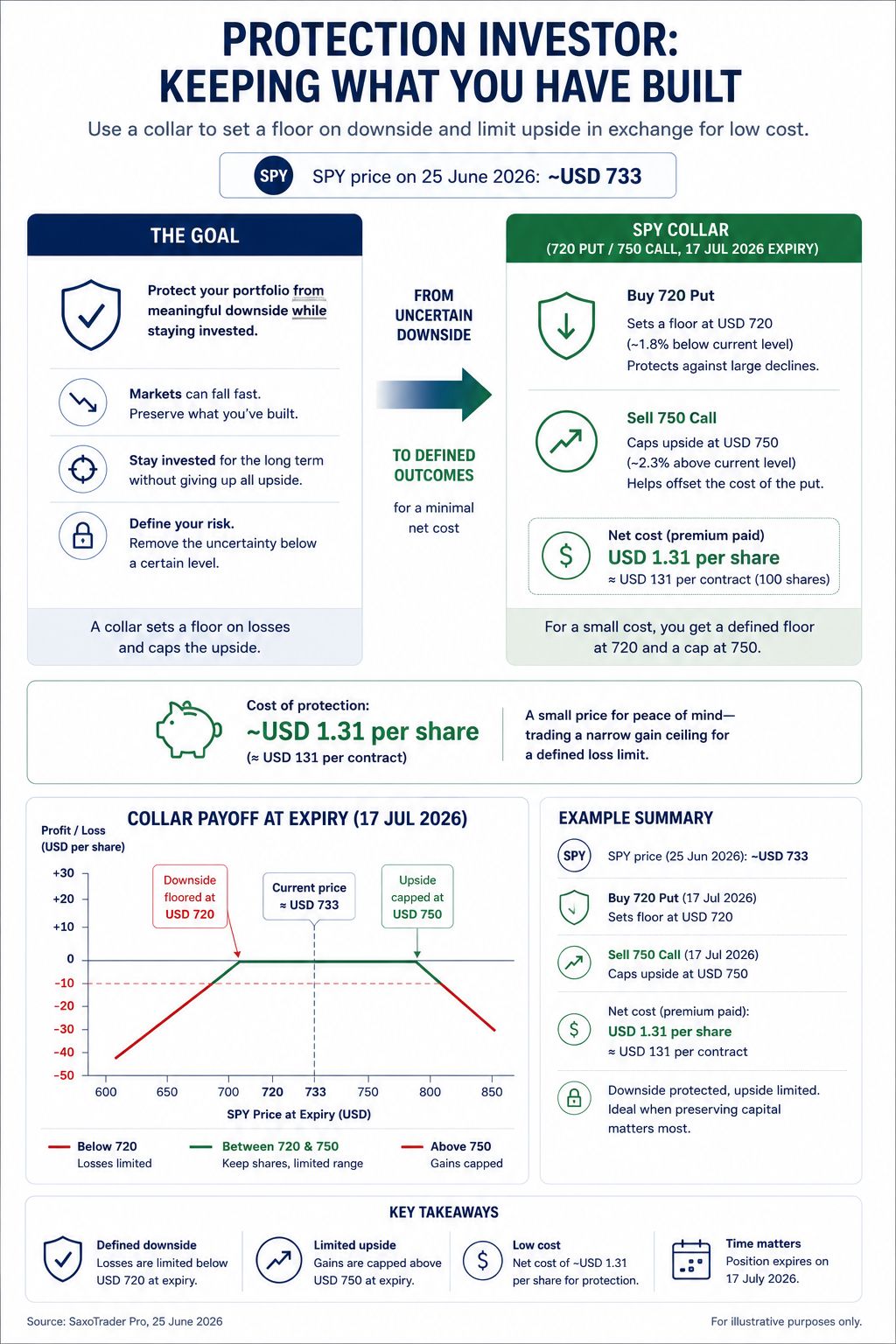

An investor in their early forties is in a different position. Wealth has accumulated. A major market drawdown now has consequences it did not have at twenty-five. The priority shifts: staying invested, yes – but not at the cost of everything built so far.

This is where options function as genuine insurance. A protective put gives the investor the right to sell a position at a fixed price before expiry, creating a defined floor below which losses cannot extend. Unlike the growth approach, this genuinely removes a specific type of risk – downside below the strike – in exchange for a premium paid upfront.

For investors concerned about the ongoing cost of insurance, a collar combines the two: a protective put is purchased to set the floor, and a covered call is sold against the same position to help fund it. The call sale caps the upside, but reduces or eliminates the net premium cost of the hedge.

Continuing the SPY illustration: a collar combining the 720 put and the 750 call, both expiring 17 July 2026, cost approximately USD 1.31 per share net – roughly USD 131 per contract (Source: SaxoTrader Pro, 25 June 2026). For that cost, the investor floors the position at USD 720 (roughly 1.8% below current levels) while capping upside at USD 750 (roughly 2.3% above). The investor trades a narrow gain ceiling for a defined loss limit – a trade that makes sense when preserving capital matters more than maximising return.

Protection investor: SPY collar (720 put / 750 call), 17 July 2026 expiry – downside floored at USD 720, upside capped at USD 750, net cost approximately USD 131 per contract. Source: SaxoTrader Pro, 25 June 2026. For illustrative purposes only. Source: Saxo

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it's crucial to make informed decisions.

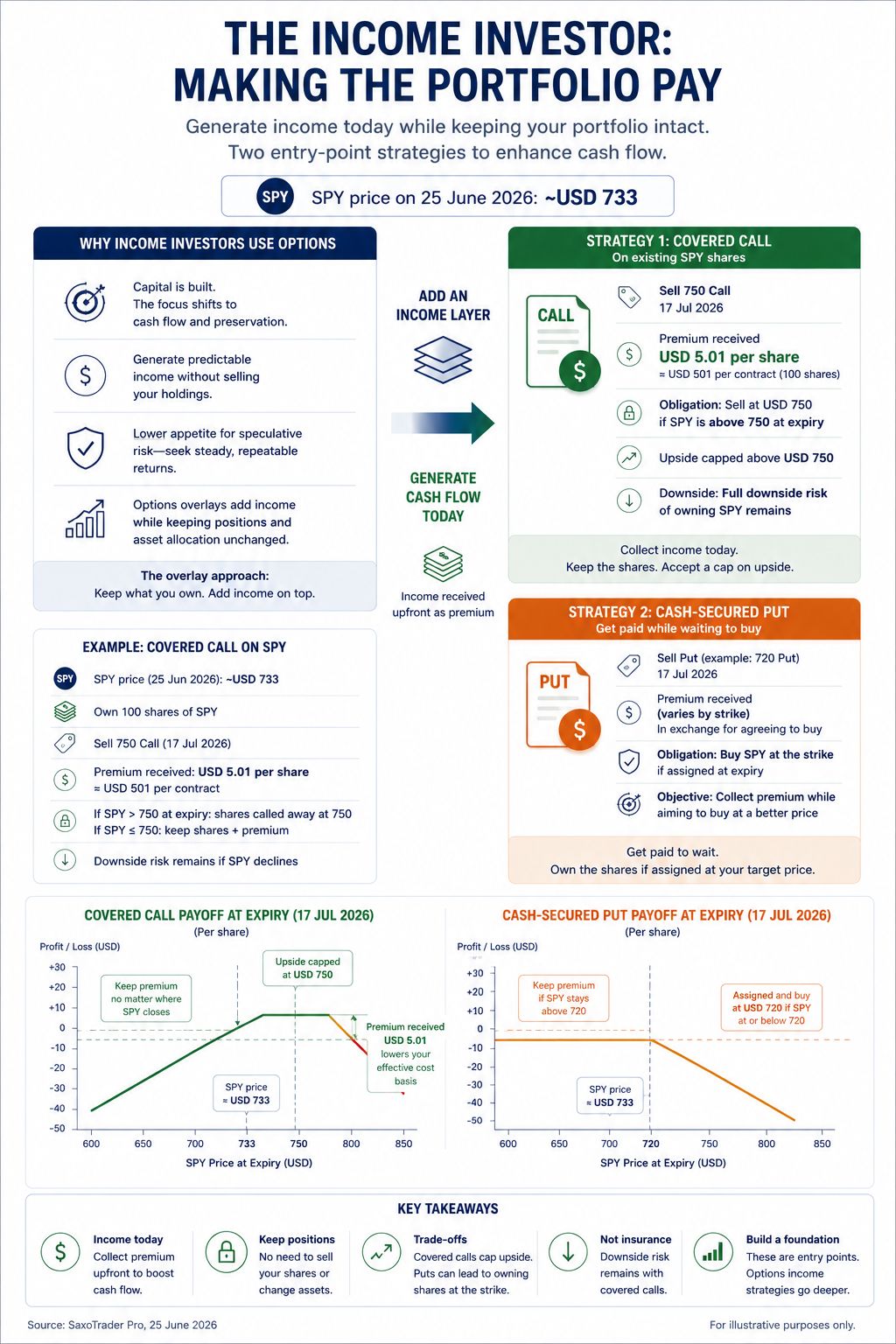

An investor approaching retirement faces a different problem. Capital is there. The question is how to make it work. Dividends matter. Predictable cash flow matters. The appetite for speculative positions is lower.

For this investor, the overlay approach is the natural entry point. Positions stay in place. Options are placed on top of them to generate additional premium without requiring any change to what is owned.

A covered call on an existing SPY holding – selling the right for someone else to buy the shares at a fixed price by a specific date – generates income immediately. The 750 strike call expiring 17 July 2026 was quoted at approximately USD 5.01 per share – USD 501 per contract (Source: SaxoTrader Pro, 25 June 2026). In exchange for that premium, the investor agrees to sell at USD 750 if SPY is above that level at expiry. The investor retains the full downside risk of holding the shares – the premium received provides a partial offset to the cost basis, but does not protect against a significant decline in the ETF’s price.

A cash-secured put on a stock or ETF the investor is willing to own works similarly: premium is collected while waiting to enter a position at a better price. Neither strategy requires selling the underlying or changing the asset class.

Income investor: covered call on SPY, 750 strike, 17 July 2026 expiry – USD 501 premium per contract collected; cash-secured put for income while waiting to buy at a target price. Source: Saxo, 25 June 2026. For illustrative purposes only.

Covered calls and cash-secured puts are the entry point. Options offer considerably more income approaches beyond these two – progressively more sophisticated, progressively more demanding. The investor who starts here is building a foundation, not arriving at a destination.

Growth, protection, and income are three distinct objectives – and options serve each one differently. Replacing stock with calls suits an investor prioritising capital efficiency over dividends. Protective puts and collars suit an investor whose priority is keeping what they have built. Overlays suit an investor who wants income without disrupting existing positions.

None of these works passively. All three require more engagement than holding a stock or ETF. But for investors who know which problem they are trying to solve, the range of tools available goes well beyond what stocks and bonds alone can offer.

The author does not hold positions in any of the instruments mentioned in this article.

This content is marketing material and should not be regarded as investment advice. Trading financial instruments carries risks and historic performance is not a guarantee of future results.

The Author is permitted to wait at least 24 hours from the time of the publication before they trade the instruments themselves.

The instrument(s) referenced in this content may be issued by a partner, from whom Saxo receives promotional fees, payment or retrocessions. While Saxo may receive compensation from these partnerships, all content is created with the aim of providing clients with valuable information and options.

This content will not be changed or subject to review after publication.

| More from the author |

|---|

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy