Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

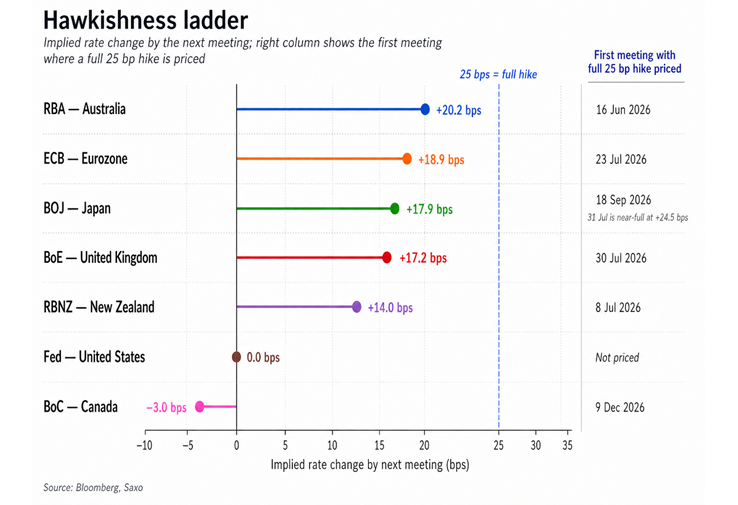

The Bank of Japan’s latest decision may look like a hold on the surface, but the message beneath it was more important: even one of the world’s most cautious central banks is becoming less comfortable waiting when energy-driven inflation risks are rising. The BOJ kept its policy rate unchanged at 0.75%, but the vote split was the real signal. The decision passed by a 6–3 majority, compared with an 8–1 split at the previous meeting, meaning two more policymakers shifted into the rate-hike camp. That growing dissent suggests the debate inside the BOJ is moving from whether inflation is sustainable enough to justify tightening, to how long the central bank can afford to wait as imported inflation risks rise. The hawkish dissent reflected rising concern that inflation pressures from the Middle East conflict and higher energy costs are becoming harder to ignore. That matters well beyond Japan. The Middle East conflict and disruption risk around the Strait of Hormuz have created a difficult policy mix: higher imported costs, weaker growth, and more volatile inflation expectations. For central banks, that is the worst kind of shock. It is not a clean demand boom where tighter policy clearly cools activity. It is a supply shock, where higher energy and raw material costs hurt households and companies even as they push inflation higher. But the BOJ’s hawkish tilt suggests policymakers may still feel forced to act. Inflation shows up in the data faster than growth weakness does. That means central banks may fight the inflation battle in front of them before they get enough evidence of the growth damage behind it. The key read-through is not that every central bank will suddenly hike. It is that the bar for dovishness has risen. The BOJ’s hawkish hold now sits within a broader global repricing of central-bank risk. The chart below shows how much tightening markets are pricing by each central bank’s next meeting, and when a full 25bp hike is first implied. Australia stands out as the most hawkish near-term case, with around 20bp priced by the RBA’s next meeting and a full hike priced by June. The BOJ, ECB and Bank of England are not far behind, with roughly 17–19bp priced by their next meetings and a full hike priced by July or September. The RBNZ also shows meaningful July hike risk, while Canada looks more delayed, with a full hike only priced by December. The Fed remains the clear outlier: markets are not pricing renewed tightening, reinforcing the idea that global policy expectations are no longer moving as one block. The common thread is clear: central banks may still worry about growth, but they are becoming less willing to look through inflation shocks. In a world of disrupted energy supply, higher transport costs and more fragile inflation expectations, policymakers may prefer to move too early on inflation rather than too late. For markets, that means the old “growth scare equals rate cuts” playbook may not work as cleanly. If inflation concerns dominate first, short-end yields can stay under pressure, rate-cut hopes can be delayed, and equities may struggle to find relief from central banks even as the growth outlook softens. The key message is not just about Japan. It is about the global policy reaction function. If energy costs remain elevated, central banks may find it harder to talk about rate cuts, even if growth risks are building. That could keep pressure on short-end bonds, where pricing is most sensitive to policy expectations. It could also weigh on equities, especially: Long-duration growth stocks that depend heavily on lower discount rates Companies with limited pricing power and greater exposure to margin pressure Sectors where valuations assume stable inflation, falling yields and benign financing conditions The BOJ’s situation is especially striking because Japan has historically moved cautiously. If even the BOJ is being pushed toward a tighter stance, investors may need to take seriously the risk that the global central-bank put is weaker than markets assume. For stocks, the danger is twofold. Higher energy and input costs can squeeze margins, especially for companies with weak pricing power. Higher policy-sensitive yields can pressure valuations, particularly in long-duration growth stocks. This does not mean equities need to fall sharply from here. Markets can still look through geopolitical shocks if investors believe there is an eventual off-ramp. But the BOJ’s message makes the “benign shock” narrative harder to sustain. If inflation expectations rise and central banks lean hawkish into slowing growth, the equity market faces a tougher mix. The BOJ’s hawkish hold is a warning shot. The Middle East shock is no longer just a geopolitical risk for markets; it is becoming a central-bank risk. If inflation pressure arrives before growth weakness becomes undeniable, policymakers may tighten or stay restrictive for longer than markets expect. That keeps upward pressure on short-end yields, complicates the case for equities, and makes the next round of global central-bank meetings more important than usual. The uncomfortable message from Tokyo is simple: in a stagflationary shock, central banks may not come to the market’s rescue as quickly as investors hope. The BOJ is exposing the central-bank dilemma

The BOJ is not alone: the hawkish bias is spreading

Why this matters for global markets

Equities: the risk is not just earnings, but multiples

Bottom line

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy