Outrageous Predictions

Révolution Verte en Suisse : un projet de CHF 30 milliards d’ici 2050

Katrin Wagner

Head of Investment Content Switzerland

la Suisse se lance dans une révolution énergétique de CHF 30 milliards d'ici 2050, rivalisant avec l...

AI is becoming a supply-chain story, not just a US mega-cap story. The next phase of the AI buildout depends on the physical infrastructure behind it: chips, memory, advanced packaging, semiconductor equipment, precision manufacturing, power and data centres.

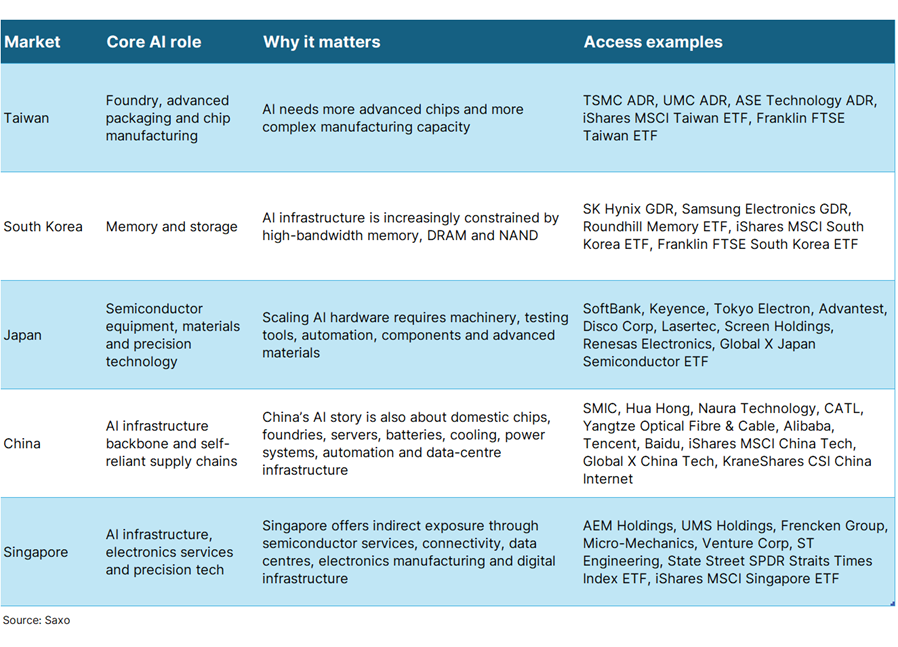

Asia sits across the key hardware bottlenecks. Taiwan brings foundry and chip manufacturing strength, South Korea leads in memory and storage, Japan provides semiconductor equipment and precision technology, China is building a self-reliant AI infrastructure stack, and Singapore offers exposure to electronics services, connectivity and data-centre infrastructure.

The opportunity comes with real risks. Asia’s AI supply-chain role is compelling, but it is also exposed to geopolitics, export controls, memory cyclicality, currency swings, energy costs and the possibility that AI capex becomes more selective after a strong investment cycle.

Asian stocks cannot escape short-term volatility from Middle East-related headlines. Higher oil prices, shipping disruption risks and geopolitical shocks still matter, especially for energy-importing economies. But for now, the bigger force in markets appears to be FOMO around AI, not war angst.

The reason is simple: AI is no longer just a US megacap software story. It is increasingly a hardware, memory, manufacturing and infrastructure story — and that brings Asia directly into the centre of investor portfolios.

The clearest signal is coming from North Asia’s AI hardware triangle. Taiwan brings the foundry layer, with export orders surging 65.9% year-on-year in March to a record USD 91.12 billion, the fastest pace in more than 16 years, driven by demand for AI and technology products. South Korea brings the memory layer, where Samsung Electronics and SK Hynix sit at the centre of the high-bandwidth memory supply chain powering AI accelerators. Japan brings the precision layer, from semiconductor equipment and advanced materials to robotics, factory automation and electronic components.

That is not a soft signal. It is a reminder that every new AI model, data centre and cloud upgrade needs physical infrastructure behind it. The market has noticed too: foreign flows have been gravitating toward the region’s “tech haves,” especially Taiwan, South Korea and Japan, as investors look beyond the US software layer and toward the hardware backbone of AI.

In other words, Asia is no longer just a region investors buy when global growth is improving. It is becoming a supply-chain exposure to the AI capex cycle.

For investors, the supply chain matters because AI does not scale on software alone. Every model upgrade, cloud deployment and enterprise AI rollout requires more compute, more memory, more advanced packaging, more power and more precision manufacturing. The companies and markets that provide these inputs may not always own the customer relationship, but they often control the bottlenecks that determine how quickly AI can be built and deployed.

That is why the AI trade is broadening beyond the US. The US remains dominant in chip design, cloud platforms, software and AI applications. But the physical layer of AI is deeply rooted in Asia. Taiwan is central to advanced foundry capacity. South Korea is critical in memory, especially high-bandwidth memory used in AI accelerators. Japan is essential in semiconductor equipment, advanced materials, electronic components and factory automation. China is building a more self-reliant AI infrastructure stack, while Singapore offers exposure to electronics services, connectivity, data centres and precision engineering.

This creates a different way to think about AI exposure. Investors who only own the US-facing layer may have exposure to the companies monetising AI, but less exposure to the companies enabling AI capacity to expand. In an AI cycle increasingly defined by scarcity — of chips, memory, equipment, energy and skilled manufacturing capacity — the supply chain becomes more than a back-office detail. It becomes part of the investment case.

The key is to think in countries and themes, not just individual stocks.

Taiwan is the most direct expression of Asia’s advanced chip manufacturing role. It sits at the centre of the global foundry ecosystem, with exposure to wafer fabrication, advanced packaging, testing and outsourced semiconductor assembly.

The investment case is tied to the idea that AI demand will continue to require more advanced chips and more complex manufacturing capacity. As chips become more powerful, the value does not sit only in design. It also sits in the ability to manufacture at scale, package chips efficiently and manage increasingly complex supply chains.

The main risk is concentration. Taiwan exposure can quickly become heavily dependent on semiconductors and a small number of dominant companies. It also carries geopolitical sensitivity and export-control risk.

Korea’s AI role is less about owning the front-end AI application and more about supplying the memory backbone that allows AI systems to function. AI infrastructure is increasingly constrained not just by GPUs, but by high-bandwidth memory, DRAM and NAND.

This makes Korea one of the most important markets for investors watching the AI hardware cycle. If AI models continue to become larger, faster and more data-intensive, the demand for memory bandwidth should remain a critical part of the supply chain.

The key risk is cyclicality. Memory markets can move from shortage to oversupply quickly. Strong AI-related demand may support high-end memory such as HBM, but broader DRAM and NAND cycles can still be volatile.

Japan is the quieter but highly important AI infrastructure market. It is less about hyperscale AI apps and more about the machinery, materials and precision tools needed to manufacture advanced chips.

Japan brings exposure to semiconductor equipment, testing tools, factory automation, precision machinery, electronic components, sensors, power systems and advanced materials. These are not always the most visible parts of the AI story, but they are essential to scaling chip production and improving manufacturing yields.

This makes Japan a different kind of AI play: less about owning the headline chip winner, and more about owning the industrial base that helps the AI supply chain scale.

The risk is that Japan’s AI exposure is more indirect and can be affected by the broader industrial cycle, yen volatility and capex spending trends across global semiconductor manufacturers.

China’s AI story is not only about chatbots, cloud platforms or consumer apps. It is also about the physical backbone needed to build a more self-reliant AI ecosystem — domestic chips, foundries, servers, power systems, batteries, cooling, industrial automation and data-centre infrastructure.

The long-term theme is strategic self-sufficiency. Export controls and geopolitical tensions have made China’s AI buildout more focused on domestic substitutes, local supply chains and infrastructure independence. That creates opportunities across hardware, cloud, internet platforms, optical fibre, batteries and industrial technology.

The risks are also different. China exposure carries policy uncertainty, US-China restrictions, domestic demand weakness, regulatory risk and potential volatility around technology sanctions.

Singapore’s AI exposure is not about frontier AI models. It is more about the infrastructure behind the theme: semiconductor services, precision engineering, electronics manufacturing, connectivity, data centres and digital infrastructure.

This makes Singapore a more defensive and infrastructure-linked way to think about the AI supply chain. It may not offer the same direct exposure as Taiwan’s foundry ecosystem or Korea’s memory leadership, but it can capture parts of the regional manufacturing and infrastructure network that support AI deployment.

Singapore also matters because it is a regional hub for capital, data, logistics and corporate activity. As AI demand increases the need for secure connectivity, reliable infrastructure and advanced electronics services, Singapore-listed names can provide selective exposure beyond the usual banks and REITs narrative.

The risk is that Singapore’s AI exposure is often indirect and company-specific. Investors should distinguish between genuine AI supply-chain exposure and broader market exposure that may be driven more by banks, property or domestic macro factors.

For investors, Asia exposure can serve three roles in an AI-age portfolio.

First, it can provide supply-chain diversification. Many investors already own US tech leaders, but the companies enabling those leaders often sit in Asia. Owning only the US-facing layer of AI may miss important parts of the value chain.

Second, Asia can offer currency and regional diversification. Foreign inflows into Taiwan and South Korea can support not just equities, but also regional currencies when the AI cycle is strong. That said, this can reverse quickly when risk appetite fades or oil prices spike.

Third, Asia can help investors move from a broad AI narrative to a more granular one. Instead of simply owning “AI,” investors can think in layers: chips, memory, equipment, power, cooling, data centres, software and applications.

That is where the opportunity, and the risk, lies.

The AI-Asia story is compelling, but it is not risk-free.

1. Geopolitical risk remains central. Taiwan is strategically important but geopolitically sensitive. Investors should not treat the valuation premium as purely about earnings growth.

2. Oil shocks can hurt Asia. Many Asian economies are energy importers. Middle East-related disruptions can pressure inflation, currencies and margins.

3. Concentration risk is rising. Taiwan exposure often means heavy TSMC exposure. Korea exposure often means Samsung and SK Hynix. Thematic ETFs can look diversified but still rely on a few names.

4. AI capex could disappoint. If cloud companies slow spending, delay data-centre projects or face margin pressure, the hardware supply chain can reprice quickly.

5. Memory remains cyclical. HBM demand is strong, but traditional memory markets have a history of boom-bust cycles.

6. Currency moves matter. JPY, KRW and TWD movements can amplify or reduce returns for foreign investors.

Investors looking at Asia in the AI age should watch a broader set of signals, because this is no longer just a single-stock or single-country story:

AI capex guidance from US megacap tech over the next few quarters. This will help confirm whether cloud, model and data-centre spending remains strong enough to support Asia’s hardware supply chain.

Guidance from Asia’s key AI hardware players. TSMC, Samsung Electronics, SK Hynix, Tokyo Electron, Advantest, Disco and other regional leaders can provide read-throughs on chips, memory, equipment demand and order visibility.

Memory pricing and HBM supply trends. These are crucial for assessing whether Korea’s AI memory cycle remains supported, or whether parts of the market are moving toward oversupply risk.

Semiconductor equipment orders and capex plans. This will show whether chipmakers are still expanding capacity, which matters for Japan’s precision equipment and materials ecosystem.

Foreign flows into Taiwan, Korea and Japan. Continued inflows would suggest global investors are still chasing Asia’s AI hardware leaders; a reversal could signal profit-taking or concern that expectations have moved too far.

China’s policy push toward AI self-reliance. Export controls, domestic chip ambitions and government support for strategic technology will remain important drivers for China’s AI infrastructure story.

Singapore’s data-centre, connectivity and precision-tech activity. These signals can help investors assess whether Singapore’s AI exposure is broadening beyond the usual banks and REITs narrative.

Oil prices, energy costs and Middle East headlines. AI is highly energy-intensive, and higher power costs can slow the buildout if they make data-centre economics less attractive or force governments to ration grid capacity. For Asia, the risk is twofold: higher oil and gas prices can pressure margins and currencies in energy-importing economies, while rising electricity demand can make power availability a bigger constraint for AI infrastructure. That does not break the AI story, but it can make the capex cycle more selective and raise the premium on markets and companies with reliable, scalable energy access.

Asia exposure is becoming harder to ignore in AI-age portfolios.

The US may still own much of the AI software narrative. But Asia owns a large part of the physical AI supply chain — chips, memory, equipment, components, automation and infrastructure.

That means investors may need to rethink Asia not as a generic emerging-market allocation, but as a more targeted exposure to the infrastructure behind AI. The opportunity is real, but so are the risks: concentration, geopolitics, oil shocks, valuation and the possibility that AI capex expectations have moved too far, too fast.

In this market, the better question may not be whether investors should chase AI. It is whether their AI exposure is too narrow.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy