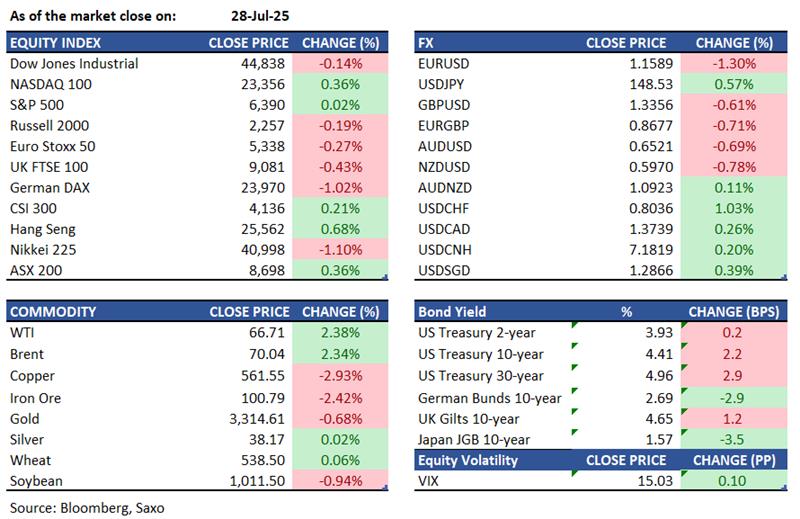

Key points:

- Macro: US and China to resume trade talks

- Equities:US markets at record highs ahead of key earnings

- FX: USD rose above 98; EUR dropped below 1.16 despite deal

- Commodities: US Copper falls as Chile Seeks Tariff Relief

- Fixed income: Focus in Asia as Japan, Australia, and Singapore plan debt auctions

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- The U.S. and China will resume trade talks today after top officials met in Stockholm on Monday, discussing disputes and extending their trade truce by three months. U.S. Treasury Chief Scott Bessent and China's Vice Premier He Lifeng led the negotiations. With an August 12 deadline looming, a lasting tariff agreement is needed to prevent major global supply chain disruptions and the reintroduction of triple-digit U.S. tariffs.

- CBI's UK retail sales gauge rose to -34 in July 2025 from June's -46, missing expectations of -26. Despite the improvement, retail sales volumes declined for the tenth month due to rising prices and economic uncertainty affecting consumer spending.

- The Dallas Fed’s Texas manufacturing index improved to 0.9 in July from -12.7 in June, showing stability after declines. Production surged to a three-year high, with orders, capacity use, and shipments turning positive. Manufacturers' outlook brightened and hiring increased, along with a sharp rise in work hours.

- Trump stated he will announce pharma tariffs soon and will address pharma issues with the UK, affirming he won't use tariffs to block the UK.

Equities:

- US - US stocks were little changed on Monday as investors digested a new US-EU trade agreement and looked ahead to a busy week filled with earnings reports and key economic data. S&P 500 finished slightly higher at record levels, the Nasdaq 100 added 0.3% to extend its record close, while the Dow slipped 64 points. Despite easing trade tensions, market sentiment remained cautious due to continued uncertainty over the broader economic impact of tariffs. Energy stocks led sector gains, with Exxon Mobil up 1% and Chevron advancing 0.9%, while materials lagged with the steepest losses. Attention now shifts to earnings from major tech giants—Meta, Microsoft, Apple, and Amazon—as well as the Federal Reserve's policy meeting on Wednesday, where investors will be watching closely for any hints of a potential rate cut in September.

- EU - Frankfurt's DAX 40 rose nearly 1% to 24,420 on Monday, nearing its all-time high of 24,639, following a major US-EU trade agreement that aims to ease transatlantic tensions. The deal imposes a base 15% tariff on most EU exports, including automobiles and pharmaceuticals, while steel and aluminum still face 50% tariffs beyond quotas. Aerospace components and certain raw materials are duty-free. The EU will buy $750 billion in US energy and military equipment. Despite ongoing challenges from tariffs, automakers like Porsche (+3.3%) saw their stocks rally, along with Mercedes-Benz (+2%), Volkswagen (+1.9%), and BMW (+1%).

- HK - Hong Kong shares rose 0.8% to 25,590 on Monday morning, recovering from earlier losses. The rebound was driven by news of a US-EU trade deal imposing a 15% tariff, half the previously threatened rate, alongside a potential three-month extension of the US-China tariff truce. Traders are also anticipating the Politburo meeting to outline economic plans for the year. Gains were limited by data showing China's industrial profits dropped 1.8% YoY in H1 2025. Attention shifts to upcoming Hong Kong trade data and the Fed's rate decision this week. AIA Group (+5.4%), HKEX (+2.8%), and CK Hutchison (+1.6%) saw notable gains.

Earnings this week:

- Tuesday: Procter & Gamble (PG), UnitedHealth (UNH), Boeing (BA), UPS (UPS), Starbucks (SBUX), Visa (V)

- Wednesday: Meta (META), Microsoft (MSFT), Ford (F), Qualcomm (QCOM), Altria (MO), Airbus (AIR)

- Thursday: Apple (AAPL), Amazon (AMZN), Reddit (RDDT), AbbVie (ABBV), Merck (MRK), Coinbase (COIN), Comcast (CMCSA)

- Friday: Chevron (CVX), Exxon (XOM)

FX:

- Dollar index surged past 98.00, bolstered by a US-EU trade agreement and upcoming trade discussions with China.

- Despite the EU-US deal, the EUR weakened below 1.1600 against USD as Germany warned of economic challenges from tariffs and France pushed for the EU to retaliate against the US.

- GBP fell below 1.3400 against the strong USD, with little new from UK PM Starmet's meeting with President Trump.

- JPY also weakened, with USDJPY exceeding 148.00 due to the dollar's rally and widening yield differentials.

- Economic Calendar - UK BoE Consumer Credit, US Goods Trade Balance, US JOLTs Job openings, US CB Consumer Confidence

Commodities:

- Oil prices rose over 2% after Trump called for Russia to quickly broker a truce with Ukraine or face economic sanctions, sparking concerns over OPEC+ supply disruptions. WTI was around $67 a barrel, with Brent near $70. Trump set a new 10-12 day deadline for a ceasefire, warning of "secondary sanctions," shortening the initial 50-day period.

- Copper prices on New York's Comex fell after Chile's Finance Minister Mario Marcel announced plans to seek an exemption from a proposed US tariff. The metal dropped as much as 6.2% to $5.4265 per pound. The US imports about half of its copper from Chile, the largest supplier.

- Gold remained down as the dollar rose sharply following a US-EU tariff deal, shifting focus to US-China trade prospects. Bullion traded near $3,312 an ounce after a 0.7% dip.

Fixed income:

- Treasuries ended with small losses, with yields rising up to 3 basis points for longer maturities following mixed results in the week's first two coupon auctions. Focus shifted early due to a US-EU trade accord, alongside the Dallas Fed's manufacturing gauge amid anticipation for a Fed rate decision and July employment data. The 2-year auction saw strong demand with a lower yield, while the 5-year had weaker demand. Supply is a key focus in Asia, with Japan, Australia, and Singapore set to auction debt.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.