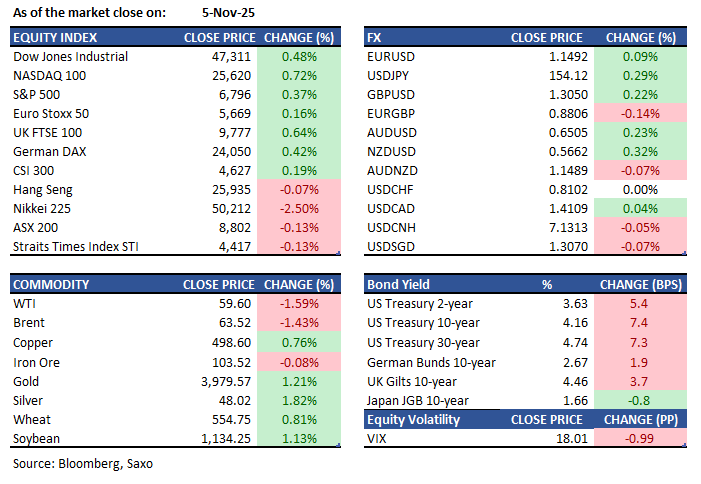

Key points:

- Macro: ADP and ISM Services reported hotter than expected

- Equities: US equities rebound; DBS exceeded profit estimates while UOB profits slump

- FX: USD flat despite strong jobs and service data; JPY weakens with USDJPY at 154

- Commodities: WTI fell below $60; gold held under $4,000

- Fixed income: Treasuries down; 10–30y yields +7bp as ADP and ISM trim Dec cut odds

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- Zohran Mamdani will be the first Muslim and South Asian mayor, and the youngest in a century. President Trump, who threatened to cut funding if Mamdani won, attacks him as a "communist." Mamdani pledges to confront "authoritarian Trump" and advocate for affordability.

- US private businesses added 42K jobs, rebounding from September's 29K job cuts and surpassing the 25K forecast. The service sector gained 33K jobs, mostly in trade/transportation/utilities (47K), education/health services (26K), and financial activities (11K), while losses continued in professional/business services (-15K), information (-17K), and leisure/hospitality (-6K). The goods sector added 9K jobs, though manufacturing shed 3K jobs. Annual pay growth was flat at 4.5% for job-stayers and 6.7% for job-changers, indicating balanced supply and demand.

- In September 2025, Japan's nominal wages rose 1.9% year-on-year, up from August's 1.5%, but below the 3.4% increase in consumer prices. Real wages fell 1.4%, marking the ninth consecutive decline. Bank of Japan Governor Kazuo Ueda highlighted the 2026 wage outlook's importance for policy decisions, while PM Sanae Takaichi expressed caution on rate hikes, noting the need for sustainable inflation backed by strong wage growth.

- The ISM Services PMI rose to 52.4 in October 2025 from 50 in September, beating forecasts. This marks the strongest sector growth since February, with business activity (54.3) and new orders (56.2) improving. Employment contraction (48.2) signals economic uncertainty, while the federal shutdown impacts business activity. The order backlog fell (40.8), as companies manage orders well. Price pressures increased (70) due to tariffs.

- US household debt reached a record $18.59 trillion in Q3 2025, up $197 billion. Mortgages increased by $137 billion, credit card debt by $24 billion, HELOC by $11 billion, and student loans by $15 billion, while auto loans stayed at $1.66 trillion. Mortgage originations hit $512 billion. Donghoon Lee from the New York Fed noted moderate debt growth and stable delinquencies, reflecting housing market resilience.

- Japan's nominal wages rose 1.9% year-on-year in September 2025, up from 1.5% in August, but lagged behind a 3.4% increase in consumer prices. Real wages fell 1.4%, marking the ninth consecutive decline. Bank of Japan Governor Kazuo Ueda emphasized the importance of the 2026 wage outlook for policy decisions, while PM Sanae Takaichi indicated caution on rate hikes, stressing the need for sustainable inflation supported by strong wage growth.

Equities:

- US - S&P 500 rose 0.4%, the Nasdaq gained 0.8%, and the Dow Jones increased by 270 points, following the Supreme Court's skeptical questioning of the Trump tariff case which eased tariff risk. Market optimism was boosted by solid ADP private payrolls, showing a 42,000 job gain, and the ISM services index hitting an eight-month high. Big tech and communication stocks led the rebound, with Alphabet up 2.4%, Meta up 1.4%, Broadcom up 1.8%, and Tesla up 2.7%. However, Palantir fell 1.5%, and Super Micro Computer dropped 12.2% on a weak outlook. McDonald’s missed earnings estimates but saw same-store sales rise 3.6%. U.S. sales grew 2.4% due to higher average checks. Qualcomm’s sales and profit forecasts beat expectations, yet shares fell over 2% after hours as a US tax change produced a $3.12bn net loss; it expects to use the alternative minimum tax, implying a steady 13–14% rate over time. The outlook points to strong high‑end Android demand and growing traction in automotive, PC and data‑centre chips.

- EU - European stocks edged higher on Wednesday, following a recovery in North American markets driven by speculative interest in AI gains. The Eurozone's STOXX 50 gained 0.2%, reaching 5,670, while the STOXX 600 climbed 0.3% to 572. Industrial and automotive sectors led the advances, with Schneider Electric and Wolters Kluwer rising between 1.5% and 2%. BMW saw a nearly 7% jump, boosting shares of Mercedes Benz, Volkswagen, and Stellantis by 2% to 4%, after reporting better margins despite tariff challenges in Q3. However, ASML slipped 1% due to negative earnings guidance from AMD and Super Micro Computer, and Novo Nordisk dropped 3.5% after lowering its growth forecast for its Ozempic diabetes and obesity drugs.

- HK - HSI decreased by 17 points, or 0.1%, to 25,935, following Wall Street's fall on valuation concerns. Tech and property shares led the dip amid anticipation of upcoming Chinese data. A survey indicated China's services sector growth slowed in October. Losses eased after Premier Li Qiang forecast economic growth and Beijing suspended tariffs on U.S. goods starting Nov. 10. Decliners included Chery (-3.7%), Xpeng (-1.4%), Li Auto (-0.6%), Prada (-3.3%), SenseTime (-3.1%), and Sunny Optical Tech. (-2.2%).

- SG - DBS reported Q3 net income of S$2.95 billion, exceeding expectations, driven by a 31% surge in wealth management fees. Total income rose 3.1%, with increased market trading income and reduced credit allowances, despite a narrowed net interest margin of 1.96%. UOB's Q3 net profit dropped 72% to S$443 million, below the S$1.34 billion consensus. The decline was due to pre-emptive allowances, an 8% fall in net interest income, margin reduction to 1.82%, and lower non-interest income amidst higher costs.

Earnings this week:

Thursday

Asia: Recruit, Suzuki Motor, DBS

Outside Asia: Warner Bros. Discovery, DraftKings, Block, Moderna, Airbnb

Friday

Asia: Mitsubishi Heavy Industries, OCBC, Honda, Macquarie, Fujikura

Outside Asia: Constellation Energy, KKR

FX:

- Dollar Index fluctuated due to profit-taking after a strong rally spurred by positive US data. The ADP report exceeded expectations, and the ISM Services Prices Paid hit a three-year high amid tariff impacts. The Supreme Court's review of Trump's tariffs remains crucial. The DXY closed at 100.17.

- JPY lost some haven status, with the USDJPY bouncing to 154.01 from 152.97 after Japan's currency diplomat flagged volatility concerns.

- CAD and CHF dipped, though CAD's drop was cushioned by PMI data swinging to expansion at 50.5 from 46.3. Conversely, NZD, AUD, and GBP advanced amid improved risk sentiment in equities.

- The Riksbank held its rate steady at 1.75%, pointing to weak labor markets but hinting at potential recovery, leaving EURSEK unchanged.

Commodities:

- Oil steadied after a two‑day slide as the EIA confirmed the largest US crude build since July, with WTI below $60 and Brent under $64 on Wednesday after a 2.4% two‑session drop, while a 5.2m‑barrel stock rise—slightly below industry estimates—and product draws tempered the bearish tone.

- Gold steadied after its biggest gain in about a week as traders weighed the US rate outlook following ADP data, with bullion just above $3,970 an ounce after Wednesday’s 1.2% rise. ADP showed private payrolls up 42,000 after two monthly declines—modest enough to suggest cooling labour demand while easing fears of a sharper deterioration.

Fixed income:

- Treasuries fell with 10–30y yields about 7bp higher as strong ADP and an upside ISM Services print trimmed December Fed cut odds, supply worries rose after the quarterly refunding flagged eventual auction increases, and odds grew that the Supreme Court will strike down Trump‑era tariffs, potentially eroding fiscal improvement. New Zealand’s curve steepened on anticipated sovereign supply, including linkers and long tenors, while today’s BoE meeting looks eventful for gilts, with the rally likely to extend.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.