Key points:

- Macro: Israel-Lebanon ceases fire confirmed by Netanyahu

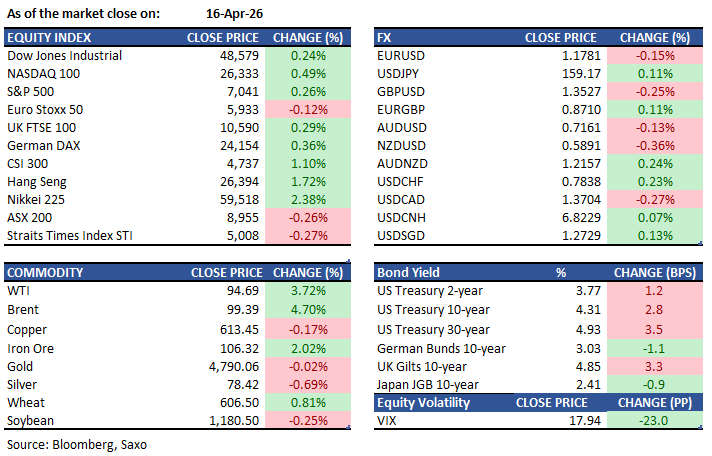

- Equities: S&P 500 closes at new high of 7,041; Netflix drops 8% after missing earning

- FX: Dollar edges higher as AUD surges to multi‑year highs

- Commodities: Brent eased toward $98 after nearly a 5% gain

- Fixed income: Foreign US Treasury holdings hit record $9.49t, biggest rise in a year

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- Tehran has reportedly agreed to abandon nuclear weapons, provide “free oil,” and reopen the Strait of Hormuz, though this is unconfirmed. Trump announced a 10-day Israel–Lebanon ceasefire, confirmed by Netanyahu. The strait remains effectively shut by US–Iran blockades, and IMF’s Fatih Birol warned restoring much of the disrupted oil and gas output could take up to two years.

- US industrial production fell 0.5% m/m in March 2026, the biggest drop since September 2024 and below expectations for a 0.1% rise. Manufacturing output slipped 0.1%, mining fell 1.2%, and utilities declined 2.3%. Capacity utilization dropped to 75.7%, 3.7 points below its long-run average.

- The Philadelphia Fed Manufacturing Index climbed to 26.7 in April 2026 from 18.1, the highest since January 2025 and far above expectations for 10. Shipments rose to 34.0 and new orders to 33.0, while employment fell to -5.1. Prices paid jumped to 59.3 and prices received to 33.5, both well above long-run averages. Firms still expect growth over the next six months, though most future indicators have eased.

- US initial jobless claims fell to 207K in the week ended April 11, 2026, from a revised 218K, below the 215K forecast and the biggest weekly drop since February, pointing to limited layoffs. The 4‑week average ticked up to 209.75K, while continuing claims rose 31K to 1.818M in the week ended April 4.

- March ECB minutes said the Middle East war has significantly increased uncertainty, with upside risks to inflation and downside risks to growth, but inflation is still expected to stabilize around 2% over the medium term. Policymakers kept rates unchanged and stressed a flexible, meeting-by-meeting approach without pre-committing to a rate path.

- BoE Governor Andrew Bailey warned of a major global energy shock that will push inflation higher but said policymakers will not rush to raise interest rates in response.

Equities:

- US: US stocks climbed to new records on Thursday with the Nasdaq rising 0.4% to 24,102.7 and the S&P 500 climbing 0.3% to 7,041.3, both notching record closing highs for a second consecutive day. The Nasdaq extended its winning streak to 12 days in a row. The Dow Jones Industrial Average added 0.2% to 48,578.7. Microsoft's stock rose 13.3% over four days, making for its best four-day stretch since 2020. AMD rose 7.8% to a record high. Netflix shares plummeted more than 8% in after-hours trading after reporting quarterly revenue of $12.25 billion and announcing co-founder Reed Hastings will step down as chairman in June.

- EU: European stocks advanced on hopes the US and Iran will resume negotiations to end the war. The Stoxx Europe 600 Index gained, boosted by cyclical sectors like autos and construction, as well as technology. Germany's DAX ended Thursday's session 0.36% higher at 24,154.47, buoyed by increasing optimism over a potential end to the war in Iran. The FTSE 100 rallied 0.29% to close at 10,589.99 after UK GDP data showed better-than-expected economic growth in February. Barry Callebaut shares plunged as much as 16% after the Swiss chocolate maker warned of a profit hit and lowered guidance for the year.

- Asia: Asian equity markets marched higher on Thursday as traders reviewed major economic reports from China and prospects for peace in the Middle East. Japan's Nikkei 225 surged 2.4% to 59,518.34, closing at a record high and erasing its losses from the Iran war. Hong Kong's Hang Seng Index gained 446.94 points, or 1.7%, to close at 26,394.26, while the Hang Seng China Enterprises Index added 2.1%. South Korea's Kospi Index rose 2.2% to 6,226.05, with Samsung Electronics contributing the most to the index gain. Taiwan's market capitalization rose to $4.14 trillion, overtaking the UK to become the world's seventh largest stock market, fuelled by soaring demand for AI chips after TSMC reported quarterly profit that rose 58% to NT $572.5b, beating expectations.

Earnings this week:

FX:

- USD climbed on Thursday, up for the first time in nine days after falling 1.9% in the past eight trading sessions, with the Bloomberg Dollar Spot Index rising less than 0.1%.

- AUD increased to its strongest level in years against the greenback and JPY, rising to as high as 0.7197 USD, a level not seen since June 2022, and gaining to 114.15 JPY, its strongest against the JPY since September 1990.

- EUR rose to a six-week high against the dollar, erasing its losses since the US launched its war against Iran, with the common currency rising as much as 0.4% to 1.1806.

- The yuan extended gains both onshore and offshore, with USDCNH falling to close at 6.8334, down four days in a row to the lowest since March 2023, while USDCNY dropped to close at 6.8360.

- NOK and CAD were up on the day amid oil price gains. USDNOK trading around 9.3586 and USDCAD near 1.3700.

Commodities:

- Oil prices remained elevated with speculation rising that higher oil prices will become the new normal even after the Iran war ends, as OPEC production plunged by the most in at least two decades in March on damage to Middle East infrastructure. Brent eased toward $98 a barrel after nearly a 5% jump on Thursday, while WTI hovered around $93.

- Gold and silver prices jumped on the announcement of a ceasefire between the US and Iran, with front month Comex gold for April rising nearly 2% to $4,749.50 an ounce, while silver futures were up 7%.

- Copper edged lower as traders eyed the prospect of peace negotiations between the US and Iran, though Chinese buyers are coming back to the copper market, putting prices on course for fresh records according to analysts.

Fixed income:

- Treasury yields reversed course and rose as US indicators surprised on the upside and markets clung to talks of a possible extension of the US-Iran ceasefire, with the 10-year yield rising 0.029 percentage point to 4.308% and the 30-year yield rising 0.039 percentage point to 4.929%.

- Foreign holdings of US Treasuries climbed by the most in a year in February, hitting a new record high of $9.49 trillion, led by gains in the Canadian and Saudi stockpiles.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.

Key points:

- Macro: Israel-Lebanon ceases fire confirmed by Netanyahu

- Equities: S&P 500 closes at new high of 7,041; Robinhood +10% on margin rule change

- FX: Dollar edges higher as AUD surges to multi‑year highs

- Commodities: Brent eased toward $98 after nearly a 5% gain

- Fixed income: Foreign US Treasury holdings hit record $9.49t, biggest rise in a year

------------------------------------------------------------------

<Table with Source>

Disclaimer: Past performance does not indicate future performance.

Macro:

- Tehran has reportedly agreed to abandon nuclear weapons, provide “free oil,” and reopen the Strait of Hormuz, though this is unconfirmed. Trump announced a 10-day Israel–Lebanon ceasefire, confirmed by Netanyahu. The strait remains effectively shut by US–Iran blockades, and IMF’s Fatih Birol warned restoring much of the disrupted oil and gas output could take up to two years.

- US industrial production fell 0.5% m/m in March 2026, the biggest drop since September 2024 and below expectations for a 0.1% rise. Manufacturing output slipped 0.1%, mining fell 1.2%, and utilities declined 2.3%. Capacity utilization dropped to 75.7%, 3.7 points below its long-run average.

- The Philadelphia Fed Manufacturing Index climbed to 26.7 in April 2026 from 18.1, the highest since January 2025 and far above expectations for 10. Shipments rose to 34.0 and new orders to 33.0, while employment fell to -5.1. Prices paid jumped to 59.3 and prices received to 33.5, both well above long-run averages. Firms still expect growth over the next six months, though most future indicators have eased.

- US initial jobless claims fell to 207K in the week ended April 11, 2026, from a revised 218K, below the 215K forecast and the biggest weekly drop since February, pointing to limited layoffs. The 4‑week average ticked up to 209.75K, while continuing claims rose 31K to 1.818M in the week ended April 4.

- March ECB minutes said the Middle East war has significantly increased uncertainty, with upside risks to inflation and downside risks to growth, but inflation is still expected to stabilize around 2% over the medium term. Policymakers kept rates unchanged and stressed a flexible, meeting-by-meeting approach without pre-committing to a rate path.

- BoE Governor Andrew Bailey warned of a major global energy shock that will push inflation higher but said policymakers will not rush to raise interest rates in response.

Equities:

- US: US stocks pushed to new highs on Wednesday as the S&P 500 rose 0.8% to 7,022.95, closing above the 7,000 mark for the first time and notching a fresh record. The Nasdaq Composite continued its streak with big gains from Microsoft and Tesla, while the Dow Jones Industrial Average fell 0.2%. In after-hours trading, QuidelOrtho shares sank 23% after announcing preliminary first quarter results. Robinhood Markets saw trading volume surge 324% of its 20-day average with the stock rising 10%, while Charles Schwab shares fell in premarket trading despite beating earnings estimates with adjusted EPS of $1.43.Netflix fell 9% after missing earnings estimates and reported Q2 revenue forecast that fell short of expectations.

- EU: European stocks advanced on hopes the US and Iran will resume negotiations to end the war. The Stoxx Europe 600 Index gained, boosted by cyclical sectors like autos and construction, as well as technology. Germany's DAX ended Thursday's session 0.36% higher at 24,154.47, buoyed by increasing optimism over a potential end to the war in Iran. The FTSE 100 rallied 0.29% to close at 10,589.99 after UK GDP data showed better-than-expected economic growth in February. Barry Callebaut shares plunged as much as 16% after the Swiss chocolate maker warned of a profit hit and lowered guidance for the year.

- Asia: Asian equity markets marched higher on Thursday as traders reviewed major economic reports from China and prospects for peace in the Middle East. Japan's Nikkei 225 surged 2.4% to 59,518.34, closing at a record high and erasing its losses from the Iran war. Hong Kong's Hang Seng Index gained 446.94 points, or 1.7%, to close at 26,394.26, while the Hang Seng China Enterprises Index added 2.1%. South Korea's Kospi Index rose 2.2% to 6,226.05, with Samsung Electronics contributing the most to the index gain. Taiwan's market capitalization rose to $4.14 trillion, overtaking the UK to become the world's seventh largest stock market, fueled by soaring demand for AI chips after TSMC reported quarterly profit that rose 58% to NT $572.5b, beating expectations.

Earnings this week:

FX:

- USD climbed on Thursday, up for the first time in nine days after falling 1.9% in the past eight trading sessions, with the Bloomberg Dollar Spot Index rising less than 0.1%.

- AUD increased to its strongest level in years against the greenback and JPY, rising to as high as 0.7197 USD, a level not seen since June 2022, and gaining to 114.15 JPY, its strongest against theJPY since September 1990.

- EUR rose to a six-week high against the dollar, erasing its losses since the US launched its war against Iran, with the common currency rising as much as 0.4% to 1.1806.

- The yuan extended gains both onshore and offshore, with USDCNH falling to close at 6.8334, down four days in a row to the lowest since March 2023, while USDCNY dropped to close at 6.8360.

- NOKand CADwere up on the day amid oil price gains. USDNOK trading around 9.3586 and USDCAD near 1.3700.

Commodities:

- Oil prices remained elevated with speculation rising that higher oil prices will become the new normal even after the Iran war ends, as OPEC production plunged by the most in at least two decades in March on damage to Middle East infrastructure. Brent eased toward $98 a barrel after nearly a 5% jump on Thursday, while WTI hovered around $93.

- Gold and silver prices jumped on the announcement of a ceasefire between the US and Iran, with front month Comex gold for April rising nearly 2% to $4,749.50 an ounce, while silver futures were up 7%.

- Copper edged lower as traders eyed the prospect of peace negotiations between the US and Iran, though Chinese buyers are coming back to the copper market, putting prices on course for fresh records according to analysts.

Fixed income:

- Treasury yields reversed course and rose as US indicators surprised on the upside and markets clung to talks of a possible extension of the US-Iran ceasefire, with the 10-year yield rising 0.029 percentage point to 4.308% and the 30-year yield rising 0.039 percentage point to 4.929%.

- Foreign holdings of US Treasuries climbed by the most in a year in February, hitting a new record high of $9.49 trillion, led by gains in the Canadian and Saudi stockpiles.

For a global look at markets – go to Inspiration.

This content is marketing content and should not be considered investment advice. Trading financial instruments carries risks and historic performance is not a guarantee for future performance.

The instrument(s) mentioned in this content may be issued by a partner, from which Saxo receives promotion, payment or retrocessions. While Saxo receives compensation from these partnerships, all content is conducted with the intention of providing clients with valuable options and information.