Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Broadcom has emerged as one of the most important “behind-the-scenes” players in the AI revolution. The company’s latest partnership with OpenAI, co-developing a new AI chip slated for 2026, cements its role as a critical supplier of the infrastructure that powers artificial intelligence.

For investors, the takeaway is clear: Broadcom is not just riding the AI wave, it is shaping the rails on which it runs.

Broadcom confirmed a new multi-billion-dollar AI customer order, which was later reported to be OpenAI.

OpenAI will co-develop a custom AI accelerator with Broadcom, with mass production expected in 2026. The contract is estimated at around $10 billion, making it one of the largest bespoke chip partnerships in the AI industry.

OpenAI’s decision to design its own chips with Broadcom is more than a headline. It signals two key shifts:

For investors, this provides multi-year revenue visibility and validates Broadcom’s role as a critical enabler of the AI ecosystem.

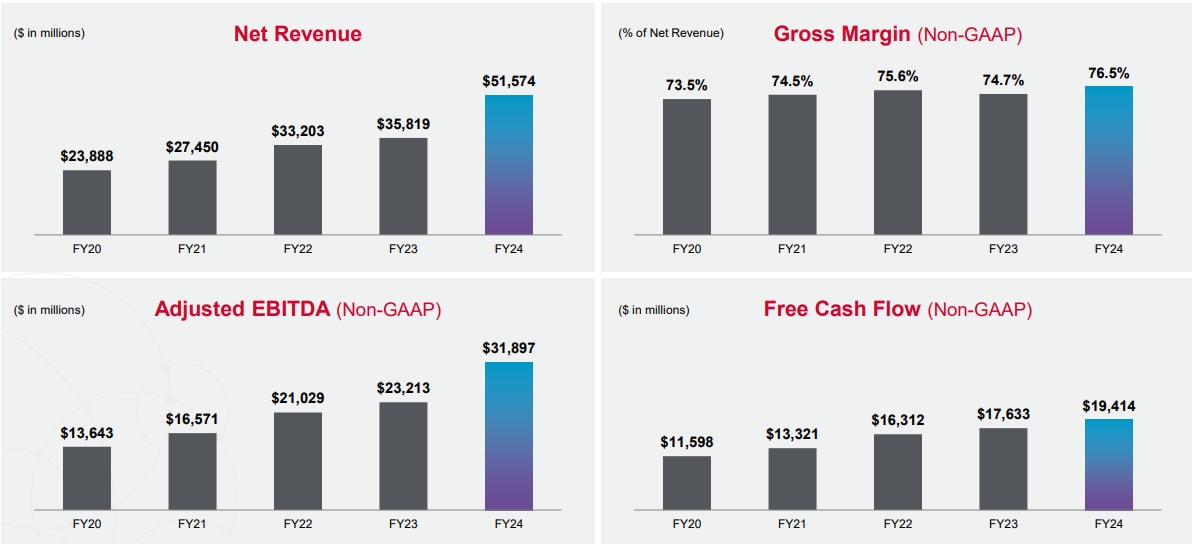

Broadcom’s latest quarterly results highlight how much AI is already reshaping its business:

CEO Hock Tan pointed to strength in custom AI accelerators, networking, and VMware, underscoring the company’s diversified AI positioning.

Looking ahead, Broadcom expects further growth in Q4 FY2025:

This guidance shows AI is becoming an increasingly dominant driver of the company’s overall top line.

Unlike rivals focused only on hardware, Broadcom is also expanding into AI infrastructure software, building a cohesive ecosystem that strengthens client retention and upsell opportunities.

Broadcom’s positioning is unique because it touches multiple layers of the AI stack:

This “multi-pronged” approach makes Broadcom less dependent on any single client, model, or trend.

Broadcom’s ability to deliver end-to-end solutions, from silicon to software, is becoming a key differentiator in a market where integration matters most.

No investment story is without challenges:

Broadcom is evolving into a picks-and-shovels leader of the AI economy. Unlike pure AI model companies, it profits from the infrastructure demands of the entire ecosystem—training chips, networking, and enterprise software.

For investors, Broadcom offers:

The risks are real, but the structural trend of rising AI infrastructure spending gives Broadcom an enviable positioning.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy