Quarterly Outlook

Equity outlook: The high cost of global fragmentation for US portfolios

Charu Chanana

Chief Investment Strategist

Global Macro Strategist

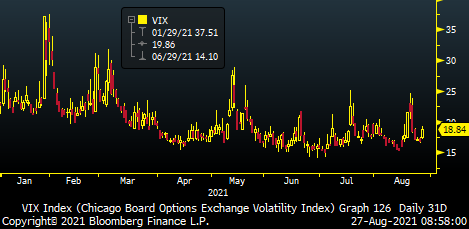

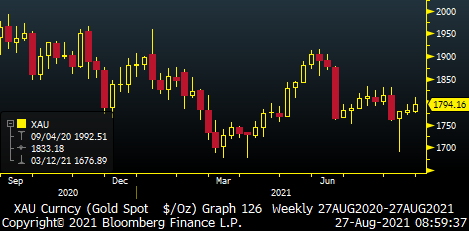

Summary: Macro Dragon Reflections - In the latest reflections think piece, KVP takes a look at a few potential pathways & scenarios around the Fed's Jackson Hole event. Including the base case consensus scenario of a conservative & docile Powell, alongside the more interesting tail-side risks to the upside, as well as downside. Which pathways may see the VIX 18.84 jump by +50% to 30, or Gold $1795 crater lower by $100 to retest the recent $1690 lows. Plus there is also a pathway that could set us up for the S&P 500 rising +12% to finish the year above 5,000.

This week's symposium could offer hints on how the Federal Reserve is looking to start tapering its bond purchase programme. But it is unlikely Fed Chair Jerome Powell will give much details on exact taper timing and composition. There is still a debate among officials regarding the macroeconomic impact of the Delta variant and how it could temporarily postpone the start of the taper. Our baseline is that taper could start from November onwards if the pandemic situation evolves favourably in the United States.

-

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Head of Fixed Income Strategy