Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

Smaller companies in the US (called “small-caps”) have started to shine again. Investors believe the US central bank (the Fed) will start cutting interest rates soon. Lower rates usually help smaller, more local businesses because they borrow more and are sensitive to financing costs.

Recession concerns also look contained for now, which historically supports small-caps because they tend to do better when economic conditions remain supported.

Small-caps also look cheaper than big companies like Apple or Microsoft. If the economy stabilizes and borrowing costs fall, small companies could see a bigger rebound than the giants that already had their rally.

When people talk about “small-caps” in the US, they often mean the Russell 2000 index. This index tracks 2,000 of the smaller companies listed in the US stock market. Unlike the S&P 500, which covers the biggest and most established firms, the Russell 2000 gives a picture of how Main Street businesses are doing.

Because these companies are smaller, they tend to:

Investors often use the Russell 2000 as a barometer of the US economy beyond the big tech names and household brands.

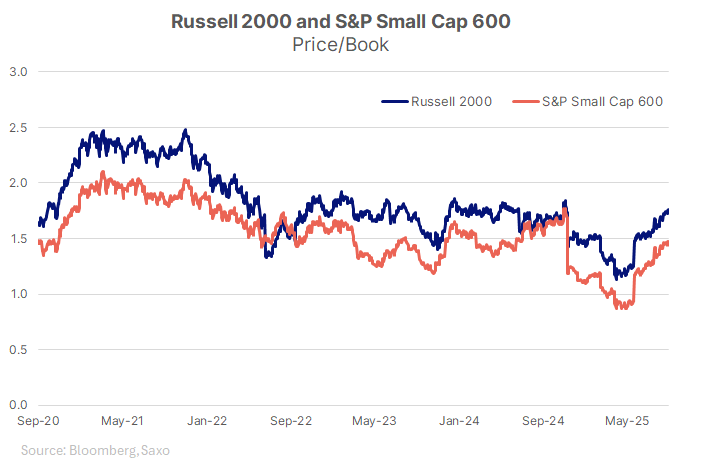

While the Russell 2000 is the most widely known small-cap index, it has a problem: many of its companies are not profitable. Almost half lose money. That makes it risky to buy the entire index blindly.

A useful alternative is the S&P SmallCap 600, another index of smaller US companies. The key difference: it only includes businesses that are already profitable. This simple filter makes it a better-quality small-cap benchmark.

So, in comparison:

Bottom line: The S&P 600 focuses on the stronger small-caps, while the Russell 2000 covers all small-caps—good and bad.

Here are the key metrics comparing Russell 2000 (RTY) and S&P 600 (SML) since 1994 (when S&P 600 was launched) and over the last 5 years:

These patterns highlight a key point: small-caps usually do better when interest rates are falling, credit conditions are easier, and the economic momentum is supported. They tend to lag when borrowing costs are high or when investors crowd into mega-cap tech.

While the setup looks more constructive for small-caps, there are risks that could challenge the outlook:

Small-caps are interesting, but not indiscriminately. The Fed’s next move will define the path: a measured cut cycle favors quality small-caps, while broad beta only pays off if easing accelerates.

The lesson for investors from history is clear: small-caps can work, but selectivity – profitability, valuation discipline, and balance-sheet strength – matters more than simply buying the whole basket.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy