Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

Summary: Policymakers are taking yet another dip in the 'pretend-and-extend' punchbowl as both monopolies and central banks snap up assets across the board. No market trades freely, price discovery is zero, and it is time to get long inflation.

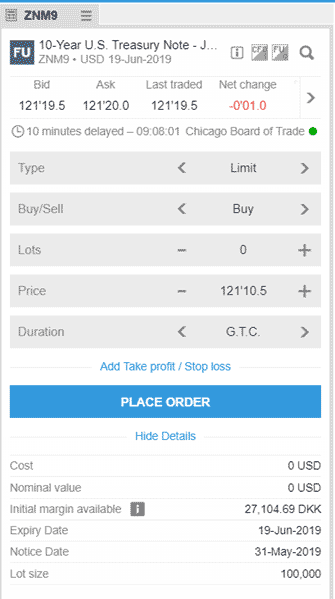

Instrument: 10-year US Futures

Price Target: not specified

Market Price: spot 121 19.5/32

Entry: spot 121 19.5/32

Stop: 122 28/32 on the close

Target: 118 ½

Time Horizon: long term

For those of you who are inclined to learn from history, I implore you to read Paul Volcker's book 'Keeping At It', noting particularly the chapters on how he and then-Treasury Secretary Connally took the US out of the Bretton Woods agreement with the policy at the time being: controls, tariffs (on Germany), devaluing the dollar and trying to ditch the trade deal in place with Canada!

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist