EM currency outlook: Trump tariffs A global trade war is the last thing EM economies need, many of which rely on exports of both raw and finished goods and foreign-derived capital flows as drivers of growth. From here, market conditions will remain tense as we await two things. First, whether Trump’s mind can be changed as Republican leaders and his own advisers scramble to change his mind, and second, if not, the response from major US trade partners, Chinese and otherwise, to Trump’s latest move.

Will countries respond in strong terms and try to force the US to back down as was the case when Bush junior tried to enact similar tariffs some 15 years ago, or will they fear that the US mood has changed and merely pick their battles and hope that an eventual new occupant in the White House after 2020 will see a change of tune? China’s response will be the most important, for obvious reasons as the largest exporter into the US economy. The latest volatility will prove a mere dress rehearsal if we lurch into a negative spiral of protectionism measures and countermeasures. If Trump has a sudden change of heart, on the other hand, risk appetite could stabilise quickly.

The trade war/protectionism risk was our chief of the three major risks to the EM outlook we have identified in previous weeks. The other two were pressures from rising US yields and EU existential risks. On the latter of these two, over the weekend, the strong German SPD party vote in favour of renewing the GroKo (grand coalition between the Merkel led CDU/CSU and SPD) was the most immediate obvious relief for global markets as it moves the EU closer to addressing the need for structural reform and keeps the political situation stable in the EU’s largest economy. More worrisome was the very strong result for populist parties in the Italian election, though the immediate fallout is far from clear and could lead to a very drawn out attempt to discover if a workable minority government can be formed. This probably means that this source of general market uncertainty can fade for now, even if it will inevitably arise again much farther down the road.

As for rising US yields, these are still a strong concern from here, but the market has shifted gears a bit on the sudden introduction of the Trump protectionist threat, and US yields have eased back lower after the Fed’s Powell sounded a bit more reassuring in his second round of testimony and on the recent bout of weak risk appetite.

Otherwise, we note that the Chinese yuan appreciation has been halted dead in its tracks, providing a strong headwind for any further appreciation of Asian EM currencies as long as this remains the case. The Indonesian rupiah is at a new low for the cycle as the weakest link in Asia at the moment.

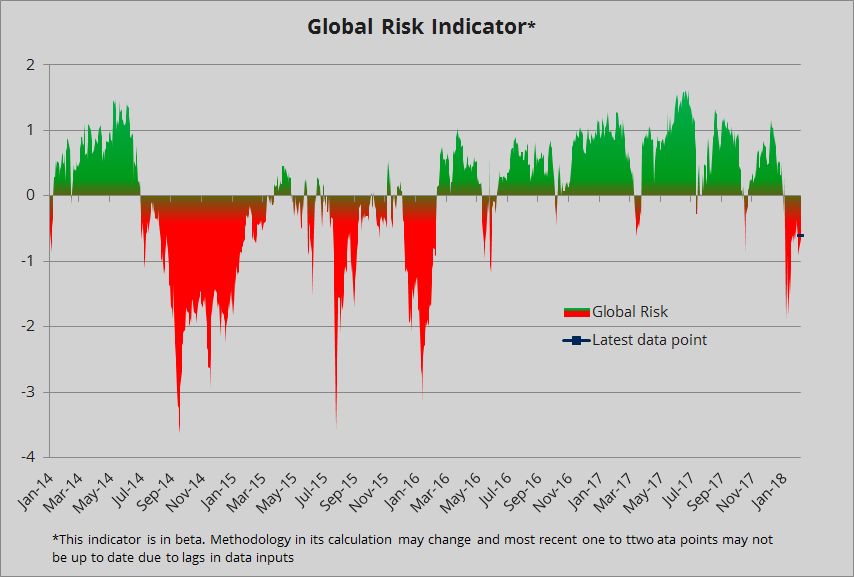

Chart: Global Risk Index The chart below is a Global Risk indicator which offers a perspective on the short-term level of risk appetite relative to the longer-term backdrop. The comeback in risk we noted last week has yielded to fresh volatility, with emerging market spreads back near the highs for the recent cycle, even if those highs don’t represent a major escalation of fear (November of last year saw a larger spike, for example). The chief drivers of negativity remain general asset market volatility and credit, with EM playing a role as well merely because spreads have risen above moving averages. So the coast is far from clear for EM, although longer-term investors will find valuations have eased from recent extremes in most cases.

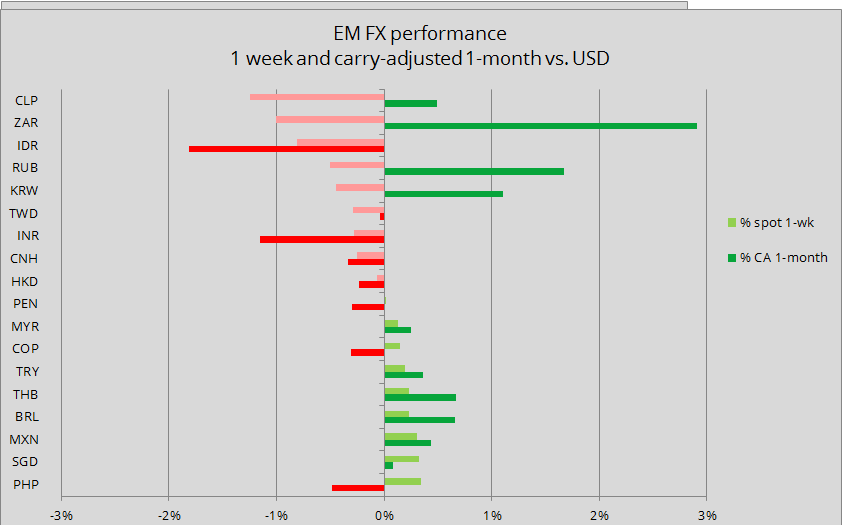

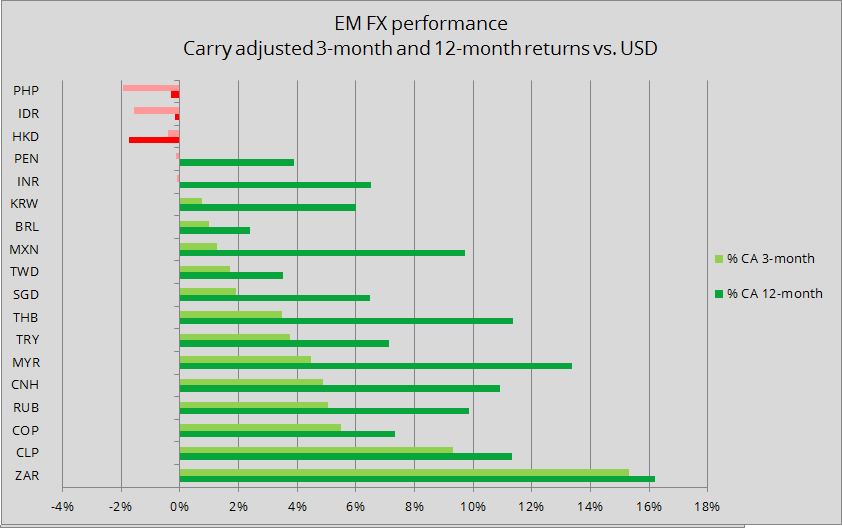

EM currency performance: Recent and longer term, carry adjusted

Chart: the weekly spot and 1-month carry-adjusted EM FX returns vs. USD. The snapshot on Tuesday of this week was actually far better than Monday, but still, the performance for EM over the last week and month has seen a number of shifts into the red. Note that the weakest short-term performers, particularly the South African rand (ZAR), are the currencies that have been performing the best until recently. This is a classic sign of hot money position squaring. Also, the most commodity-leverage economies were likewise among the heaviest losers over the last week, like the Russian ruble (RUB) and Chilean peso (CLP), the latter almost a proxy for the expectations of the copper price.

Chart: 3-month and 12-month carry-adjusted EM FX returns vs. USD. It is useful to consider the longer-term EM currency performance versus the short-term weakness, as most EM currencies are stronger versus the USD over the longer-term time frames, thanks to carry and the prior weak USD regime.

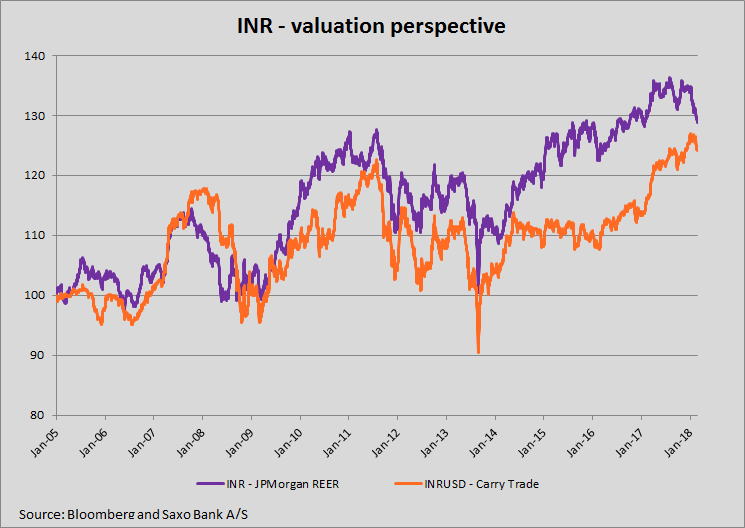

Spotlight currency this week: INR (Indian rupee) – A long-term upside, short-term bad price?

Spotlight currency this week: INR (Indian rupee) – A long-term upside, short-term bad price? This week we highlight the Indian rupee, a currency that was a solid performer in 2017 but has been a laggard over the past few months, slipping to an almost unchanged performance versus the USD in carry-adjusted terms over the past three months. We can explain away much of the recent weak performance of INR as a mere product of a dulled appetite for riskier global assets in the wake of all of the market turmoil since late January. But what are the prospects from here? The Indian currency was a very strong performer in 2017 and many have touted the country as “the next China” as there is tremendous upside potential for growth.

On the plus side, India has a large (in absolute if not percentage terms) and highly educated upper middle class and elite, tremendous upside growth potential from urbanisation, and a government committed to reform, as it seeks to reduce red tape and reform the tax code. India has also emerged from a traumatic demonetisation scheme aimed at reducing the gray economy. Nearly everything is pointing in the right general direction for the longer term, though challenges remain.

Despite that long-term potential, the current INR level does not look attractive given a set of challenges for the country from here. First and perhaps foremost is simple valuation – in CPI adjusted terms (as we show below), the rupee is only a few percent from its all-time high, some 30% stronger from the base of several years ago. India is a net consumer with a large trade deficit, and a strong currency has encouraged even wider deficits, with the trade deficit almost doubling from the lows of early 2016 – much of that on the rise in oil prices as India imports nearly all of its supplies. The current account deficit has worsened, though was still a modest -1.4% in 2017.

On the policy side, the central bank rate has been steady at 6.00% for some time, but real interest rates have fallen sharply as inflation has rebounded strong from mid-2017 lows. The Reserve Bank of India has made a few hawkish noises as it is a bit more wary on inflation – but a higher policy rate won’t necessarily support the currency. And a steep rise in longer-term rates represent an economic headwind for the economy. The latest PMIs for February were not encouraging, with the Services PMI dipping below 50 for the first time in several months.

Chart: INRUSD carry trade versus the JP Morgan Broad Effective Exchange Rate (CPI adjusted – and inverted) A longer-term chart of the carry adjusted performance of INR vs. the USD together with the JP Morgan Broad CPI-adjusted Real Effective Exchange Rate for INR. Both are indexed to 100 at the beginning of 2005. The REER shows that the INR remains richly valued relative to its historic range.

But perhaps most problematic for the growth outlook from here is the country’s banking system, which has one of the world’s largest portfolios of non-performing assets as a percentage of national GDP, mostly concentrated in public sector banks that provide 70% of India’s banking. These banks are widely recognised as a mess and a cleanup effort has been long underway. But over the last month, an enormous scandal has rocked Punjab National Bank, one of the public sector lenders.

The widespread scandal had many actors and showed collusion by bank employees auditors and bad billionaire actors in the private sector. Given the kind of reckless lending activities that the huge bad asset portfolios and this scandal lay bare, the risk points to tighter credit from these public banks, both as new rules for lending activity take increasing effect and on possible self-regulation to avoid new negative scrutiny. As well, India has announced a budget that is projected to generate a deficit of 3.5% of India’s GDP for next year, but does not include some of the bank cleanup efforts above, so is effectively even larger – and could get larger still if the Modi-led government is tempted to increase spending into the early 2019 elections.

India has a spectacular long run potential if it is able to continue to upgrade infrastructure and from the kind of productivity increases that come from urbanising a still shockingly rural population base (the World Bank estimated 2016 urban population at 33%). Shortly put, the long-term potential for India offers great promise, but the short-term entry point from a currency perspective doesn’t look attractive at this time.