Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Singapore banks have been among the clearest winners of the higher-rate cycle. For several years, higher interest rates helped lift net interest margins, profitability and capital returns. Investors could almost think of DBS, UOB and OCBC as different versions of the same trade: strong balance sheets, attractive dividends and steady exposure to Singapore’s financial strength.

That phase is changing.

The latest earnings show that the old playbook — higher rates equal stronger bank profits — is no longer enough. Net interest margins are under pressure as benchmark rates soften, loan growth remains modest, and the macro backdrop is becoming more complicated because of oil-price volatility, geopolitical risks and uneven regional growth.

The good news is that this is not a weakness story. Singapore banks remain resilient. But it is becoming a more selective story. The question for investors is no longer simply whether Singapore banks are attractive. It is which bank best fits the role they want in a portfolio.

The most obvious message from the results is that the peak-rate boost is fading. DBS, UOB and OCBC are all seeing some pressure from lower interest rates or narrower margins. That does not break the bank thesis, but it changes what investors should focus on.

During the rising-rate cycle, higher margins were the simple sector-wide tailwind. Now, banks will need to defend returns through a broader earnings mix. That puts more weight on fee income, wealth management, treasury customer activity, cost control and asset quality.

In other words, the sector is moving from a rate story to an execution story.

The clearest differentiator this quarter was wealth management.

DBS still has the deepest and most established wealth platform. Its record income and strong capital return show that the franchise remains difficult to beat. For investors, DBS continues to look like the quality leader — but because it is already viewed that way, expectations are also higher.

OCBC showed the strongest improvement in wealth momentum. Its wealth management fees rose sharply, helping offset margin pressure and driving a better-than-expected earnings result. The planned acquisition of HSBC’s wealth and premier banking portfolio in Indonesia also gives OCBC a more visible regional wealth-growth angle.

UOB has the ambition, but the market may want more evidence. Its ASEAN network gives it a strong long-term platform, and management has a clear target to grow wealth income over time. But this quarter’s softer overall fee income means investors may wait for stronger delivery before assigning a higher growth premium.

The key point: all three banks are talking about wealth, but they are not in the same position. DBS has scale, OCBC has momentum, and UOB has potential.

Singapore banks remain attractive to many investors because of dividends and capital returns. DBS stands out most clearly here, with its strong dividend and capital return profile continuing to support the investment case.

But dividend yield alone is not enough. If margins keep compressing, investors will want to know whether capital returns are backed by sustainable earnings growth. That means fee income and wealth growth matter even more.

A high payout can support a stock, but a stronger earnings mix can sustain it.

There is no sign of a broad credit problem in the latest results. That is important. Singapore banks still look well-capitalised and disciplined.

But investors should not ignore the macro risks. Higher oil prices, geopolitical uncertainty and slower regional trade can all affect loan demand, borrower stress and provisioning needs. OCBC’s higher allowances are a reminder that banks are preparing for a less predictable environment.

For now, asset quality is not the problem. But it is the risk to watch if the macro backdrop worsens.

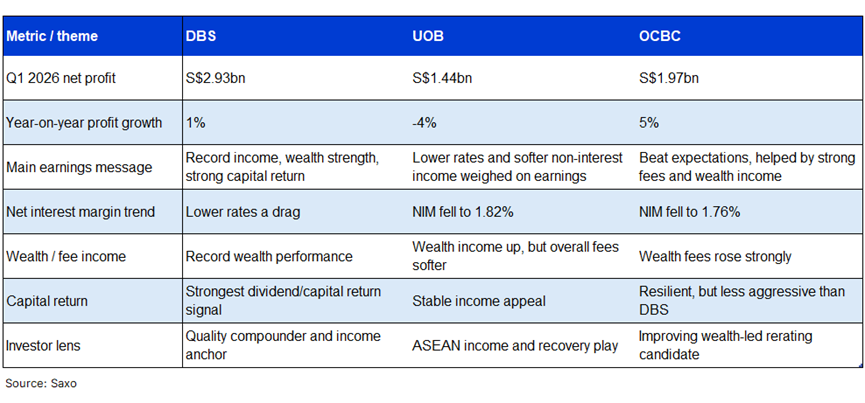

DBS remains the benchmark among the three Singapore banks. Its Q1 net profit rose 1% year-on-year to S$2.93 billion, while total income reached a record level. That matters because it shows DBS is still able to defend profitability even as the rate tailwind becomes less powerful.

The strength of DBS lies in its scale, wealth franchise, treasury customer activity and capital return profile. It continues to look like the most complete banking franchise in Singapore. For income-focused investors, the dividend and capital return story remains a major attraction.

The risk is that DBS is already treated as the best-in-class name. That leaves less room for disappointment. If earnings growth becomes more modest, investors may become more sensitive to valuation and ask whether the premium remains justified.

Investor lens: DBS remains the quality and income anchor, but the stock needs continued proof that wealth and fee income can offset margin pressure.

OCBC delivered the strongest positive surprise this quarter. Net profit rose 5% year-on-year to S$1.97 billion, helped by strong non-interest income and a sharp rise in wealth management fees.

This is important because OCBC has often been viewed as the more conservative Singapore bank. The latest results suggest that its wealth engine is gaining momentum, and that could make the stock more interesting in a market that is looking beyond NIM.

The Indonesia wealth acquisition adds another layer to the story. It strengthens OCBC’s regional wealth platform and gives it exposure to a market with long-term affluence growth. That said, integration and execution will matter.

The main caveat is provisions. Higher allowances may simply be prudent risk management in a more uncertain world, but investors should watch whether they remain precautionary or become a sign of rising credit stress.

Investor lens: OCBC looks like the strongest improvement story this quarter, with wealth momentum helping close some of the perception gap with DBS.

UOB’s quarter was more subdued. Net profit fell 4% year-on-year to S$1.44 billion, with lower rates, softer net interest income, weaker fees and lower trading income weighing on results.

This does not make UOB a weak bank. It remains profitable, well-capitalised and strategically positioned across ASEAN. Its regional footprint gives investors exposure to Southeast Asia’s long-term growth, rising wealth and cross-border trade flows.

But the latest results show that the market may need more evidence before rewarding UOB with a stronger rerating. Its wealth ambition is credible, but execution needs to become more visible. Compared with DBS and OCBC, UOB currently looks more like a steady ASEAN income story than a near-term earnings acceleration story.

Investor lens: UOB may appeal to investors willing to wait for ASEAN and wealth execution, but it needs stronger fee and earnings momentum to close the gap with peers.

A simpler way to think about the three banks is to start with the investor’s objective:

The simplest framing: DBS offers quality, OCBC offers improvement, and UOB offers ASEAN optionality.

Singapore banks remain resilient, but the investment case is becoming more selective.

The sector is no longer just a simple high-rate beneficiary. The next phase will depend on which banks can protect returns through wealth management, fee income, disciplined capital returns and strong asset quality.

DBS remains the quality leader. OCBC has the strongest improvement story from this earnings round. UOB remains a solid ASEAN franchise, but it needs more proof of acceleration.

The Singapore bank trade is not over. It is just becoming more demanding. And in a market where easy tailwinds are fading, that differentiation may be exactly what investors should welcome.

Investors who want to go beyond comparing the three banks may also find these useful:

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy