Quarterly Outlook

Q3 Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Global Macro Strategist

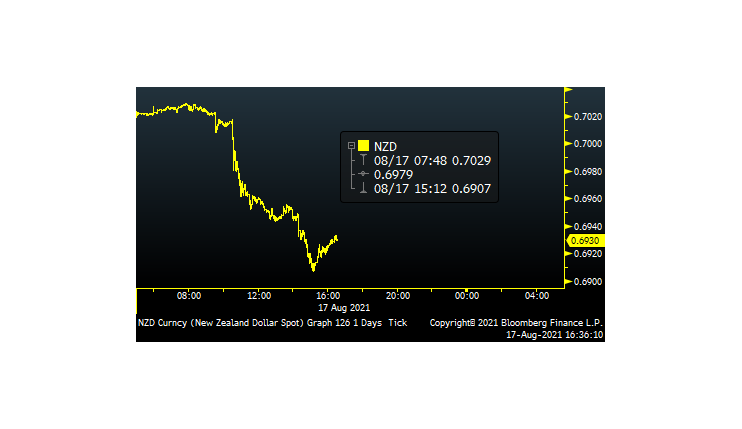

Summary: This Macro Dragon Strike piece was sent yest, yet still very pivotal given RBNZ expected rate hike decision to 0.50% from 0.25%, which would make them the first G10 central bank to hike. For a lot of currency traders its been a tough year, and being long kiwi crosses looked (until the Covid case & shutdown news on Tue) like one of the few signals in an ocean of noise. We could be in for some binary moves in NZDUSD, NZDJPY & AUDNZD based on both RBNZ decision, outlook & of course NZ government on the covid front.

-

-

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy