Quarterly Outlook

Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Global Macro Strategist

Summary: Macro Dragon = Cross-Asset Quasi-Daily Views that could cover anything from tactical positioning, to long-term thematic investments, key events & inflection points in the markets, all with the objective of consistent wealth creation overtime.

-The Fed is likely to be a wash, with the press conference focused on tapering structure & whether it’s still a 2021 affair (hint it will be clearer for the Fed post knowing where we sit on the $3.5T infra bill).

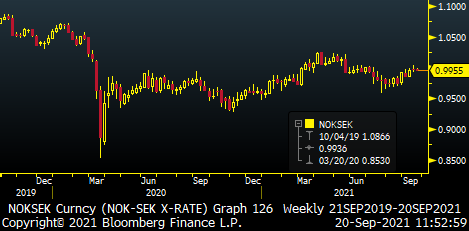

-Norges bank should be up for what the RBNZ could not, set the bell-curve by being the first G10 central bank to hike rates. KVP still loving the long NOKSEK 0.9969 +0.17% close last wk, continuing to set higher highs. The ‘easy’ move is to 1.03/1.04. We were 1.05/6 lvls pre Covid & the thesis is simply NO > SW in hawkishness & inflation.

For context in Dec 2019 Norway has inflation at 1.4% & Norges bank rate was at 0.0%. Today Norway’s inflation is at +3.4% & the Norges bank rate is at 0.0%. Also the Norwegian’s funded their covid-shock from their sovereign wealth fund, they did not play the debt/leverage game, so no tapering shuffle here. Plus it’s a structural proxy play to energy & the world re-opening.

-To KVP, Turkey’s CBRT as always has tail-risk to a cut, despite rampant inflation, Core readings came in better than expected. And some comments from the central bank governor (the 3rd in sub 3yrs & an Erdogan man), may suggest that they could be looking to ease in 4Q from the current 19.0%

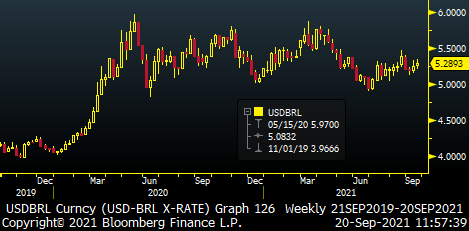

-In Brazil, the BCB should continue their hiking regime to 6.38%e 5.25%p, as inflation is still rampant at +9.7% & elections are due next year. Recent econ data from Retail Sales, to economic activity to industrial production have beat strongly. PMIs for Aug are firmly above 50 at 55.1a 54.4p for services & 53.6a 56.7p for mfg. The 2Q GDP figure was a downside surprise QoQ -0.1%a 0.2%e 1.2%p, YoY 12.4%a 12.7%e 1.0%p. Its worth noting BCB’s year-end forecast for GDP +5.2%, CPI +7.2%, Policy Rate +7.45% (+220bp from the current 5.25%).

The stunning thing – to KVP at least – is despite all these rate hikes, the real has only gained +0.86% in total returns against the USD & last year was the worst performing EM currency vs. the USD at c. -22%. Is this a situation where we only see the BRL appreciate when the banking is cutting, as money floods into the Brazilian bond market? Not sure… need to go back to the drawing board on this puppy.

-

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP

Q3 Macro Outlook: Less chaos, and hopefully a bit more clarity

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy