(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon WK #39: Heavy Central Banks WK Ahead, From the Fed to the BCB to Norges Bank... plus the Asia Sell-Off continues

Top of Mind…

- TGIM & welcome to WK #39…

- Hope everyone had a brilliant wkd in the case of Japan – back in on Tue - & China – back in on Wed – enjoy the long wkd + well deserved downtime.

- We covered a lot of what is Top of Mind in last wk’s Macro Dragon #38: US Inflation, US Infra Bill Discussions & US Debt Ceiling are key for the pre-FOMC wk ahead

- So not going to rehash what we covered around the Infra-bill, as well as potential tail-risks to getting the full $3.5T or a big fat $0, as those were all covered last wk. For now the most important thing from a Market’s risk on or risk-off into year end, is around the US Infra Bill – with Sun Sep 26 being the key deadline.

- For WK #39 – whilst we will also have flash PMIs across the board this wk, there are really only two additional key things that are front & center for KVP.

- ONE - Central Bank Rate Decisions: Super busy central bank docket, that should likely see a wash from the Fed meeting (miss in core last wk 4.0%a 4.2%e 4.3%p, headline was 5.3%a/e 5.4%p, plus epic miss in NFPs at the start of the month 235k a 725k e 1053k r) will give Snowflake Powell all the imaginary wiggle room he needs to dodge tapering. Yes would be a surprise to KVP if they used this Sep 22 mtg to signal the start – think they are waiting to see where things fall on the Infra bill.

- A few additional thoughts on some of the banks meeting this wk which will see rate decisions out of: Indonesia, USA 0.25% e/p, Brazil +6.25% e +5.25%p, Switzerland -0.75% e/p, Norway +0.25%e 0.00%e, Philippines 2.00% e/p, United Kingdom 0.10%e/p, Turkey 19.00% e/p, South Africa 3.50%e/p

-The Fed is likely to be a wash, with the press conference focused on tapering structure & whether it’s still a 2021 affair (hint it will be clearer for the Fed post knowing where we sit on the $3.5T infra bill).

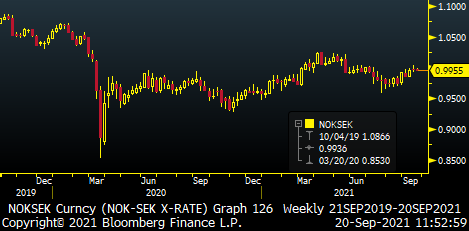

-Norges bank should be up for what the RBNZ could not, set the bell-curve by being the first G10 central bank to hike rates. KVP still loving the long NOKSEK 0.9969 +0.17% close last wk, continuing to set higher highs. The ‘easy’ move is to 1.03/1.04. We were 1.05/6 lvls pre Covid & the thesis is simply NO > SW in hawkishness & inflation.

For context in Dec 2019 Norway has inflation at 1.4% & Norges bank rate was at 0.0%. Today Norway’s inflation is at +3.4% & the Norges bank rate is at 0.0%. Also the Norwegian’s funded their covid-shock from their sovereign wealth fund, they did not play the debt/leverage game, so no tapering shuffle here. Plus it’s a structural proxy play to energy & the world re-opening.

-To KVP, Turkey’s CBRT as always has tail-risk to a cut, despite rampant inflation, Core readings came in better than expected. And some comments from the central bank governor (the 3rd in sub 3yrs & an Erdogan man), may suggest that they could be looking to ease in 4Q from the current 19.0%

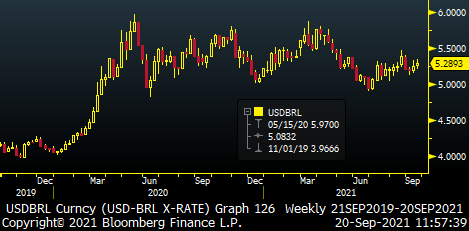

-In Brazil, the BCB should continue their hiking regime to 6.38%e 5.25%p, as inflation is still rampant at +9.7% & elections are due next year. Recent econ data from Retail Sales, to economic activity to industrial production have beat strongly. PMIs for Aug are firmly above 50 at 55.1a 54.4p for services & 53.6a 56.7p for mfg. The 2Q GDP figure was a downside surprise QoQ -0.1%a 0.2%e 1.2%p, YoY 12.4%a 12.7%e 1.0%p. Its worth noting BCB’s year-end forecast for GDP +5.2%, CPI +7.2%, Policy Rate +7.45% (+220bp from the current 5.25%).

The stunning thing – to KVP at least – is despite all these rate hikes, the real has only gained +0.86% in total returns against the USD & last year was the worst performing EM currency vs. the USD at c. -22%. Is this a situation where we only see the BRL appreciate when the banking is cutting, as money floods into the Brazilian bond market? Not sure… need to go back to the drawing board on this puppy.

- Two – Asia Risk Off, from selective China tech liquidation to cross-sector liquidations: We are starting off the new wk with continued sell-off in Asia equities, more particularly HK equity names. With the HSI currently down over -3.3% at 24100, making new lows in the process. Whilst we have been used to see predominantly China Tech names & selective names such as Evergrande being in the hot seat over the last few months.

- Last wk was pivotal from the context of that selective sector & name specific liquidation, now seems to have spilled across everything. The charts & price action are noting significant reversals in the bank & property names.

- And the Macau names in particular has a spectacular sell-off last wk, as gambling in Macau (the one legal place to do so in China) has now also come under regulatory review. Sands China was down -43% last wk to close at HK$ 15.06

- Even blue chip pure plays & darlings such as AIA Group (1299) that focuses on life insurance in the vastly unpenetrated Asia Pacific dropped c. -8% last wk to HK$ 88.10

- Front & center we have the goliath in the room that is Evergrande, the huge headwind of a known unknown – whereby the market needs to find out how all that debt, leverage & obligations will be dealt with. Today should mark some expected default of bank loans from the company.

- HK being open whilst the mainland does not get back in until Wed, is likely only exacerbating the sell-off situation. When it rains it pours & for now, it keeps pouring.

- KVP continues to just focus on the price action, as the narrative, headlines & end-game on regulatory strategy are still anyone’s guess for now. If there is one clear takeaway from all of this, bottoming out is a process & the trade construction is always superior to the investment thesis (i.e. selectively taking time to build up one’s exposure, in case one is wrong-footed on timing).

- At these 24000 lvls the Heng Seng is down -23% from the Feb highs of 26,480 & would need to fall another c. 12% to equal the 21,139 lows set during the 1Q21 covid-sell-off. You know the price action is pretty dire, when you are looking at the Covid-Sell off lows!

- At this point given the sentiment, price action & what seems to be continued wk-in & wk-out of increasing uncertainty, fundamentals are clearly out the window, we are oversold. Yet the only thing that can turn this market in the short-term is a policy response from the government. Otherwise the Macro Dragon’s thesis that 6-12M from now, one of the most obvious things to do was to buy the dip in China equities, is looking super questionable.

- The house view as from Peter Garny continues to advocate caution & avoid stance for now on China Equities. He’s been dead right so far.

- Oh & if you are looking for a few outliers in CH names, Weibo – the sole China Tech bull that mysteriously operates in a vacuum – is still +24% YTD whilst Mengniu Dairy is +7% YTD.

-

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP