Outrageous Predictions

Révolution Verte en Suisse : un projet de CHF 30 milliards d’ici 2050

Katrin Wagner

Head of Investment Content Switzerland

la Suisse se lance dans une révolution énergétique de CHF 30 milliards d'ici 2050, rivalisant avec l...

AI enthusiasm remains high, but bubble concerns are growing. U.S. tech valuations are elevated, with the S&P 500 Info Tech sector trading near 30× forward P/E (Bloomberg data, Nov 2025). The rally has narrowed, driven by a handful of mega-cap stocks.

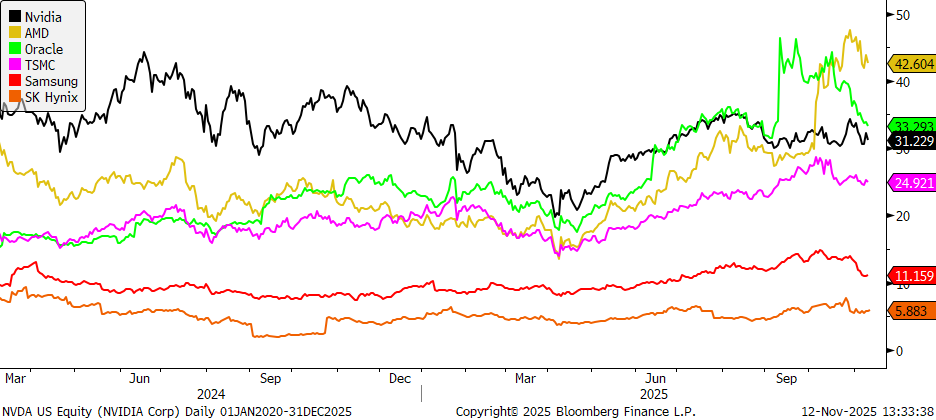

Meanwhile, the physical build-out of AI infrastructure — chips, servers, data centres — continues at full speed, and much of that is happening in Asia.

If the U.S. is selling the AI dream, Asia is building the machinery.

According to company filings, Asia accounts for around 70% of leading-edge chipmaking capacity (TSMC ~71 %), 90% of high-bandwidth memory (SK Hynix + Samsung), and nearly all advanced packaging.

As investors shift focus from “who builds the smartest AI” to “who supplies the tools,” Asia’s enablers may represent the value side of the AI trade.

While U.S. firms remain the innovation leaders, several risks are emerging:

Together, they form the “throughput stack” that converts AI investment into computing capacity. In our view, Asia sits on the capex inflow, not the outflow. Its factories continue running regardless of which U.S. platform wins the software race.

Asia’s semiconductor clusters already have the power, land, and skilled labour to scale. Recent projects, such as TSMC’s new fab in Kumamoto, Korea’s Yongin semiconductor cluster, and the planned doubling of CoWoS packaging capacity, show how investment and policy are working together to accelerate scaling. Unlike the U.S., where data-centre growth faces grid bottlenecks, Asia’s expansion, despite its own challenges, remains more capital-efficient and faster to execute.

As per Bloomberg data, forward multiples for Asia’s technology markets are:

This provides an earnings anchor and relative value buffer, though not immunity.

These developments suggest that Asia’s players are evolving from suppliers to strategic control points in the global AI value chain.

In our view, Asia’s enablers offer cheaper, more earnings-linked exposure to the AI build-out, despite still sharing global cycle risk.

Chart 1: 12-month forward P/E multiples

Source: Bloomberg

As U.S. tech faces higher costs and stretched valuations, we believe Asia offers a cheaper, more earnings-anchored route into the same megatrend.

Note: The author holds no positions in the securities mentioned.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy