Balanced ETF portfolios USD Q4 2022 commentary

| Asset classes | Stocks (developed and emerging equity), bonds, non-traditional |

| Instruments | ETFs |

| Investment style | Macro, diversified investment focus |

| Quarterly return (net of fees) | |

| Defensive | 1.94% |

| Moderate | 4.44% |

| Aggressive | 5.15% |

Market overview

After a short period of respite from market falls in October and November, December proved to be another disappointing month for asset returns. This rounded off an extremely challenging year across markets with equities posting their worst annual return since 2008, and global government bonds experiencing their first bear market in 70 years. Typically, government bonds provide a cushion to investors in uncertain environments. This did not prove to be the case in 2022 as higher and more persistent inflation led to central banks to raise rates further than had been expected coming into the year. The resulting rise in yields across sovereign and credit markets led to the worst performance in a generation.

Commodity markets were one of the very few areas to generate positive returns over the year as the tragic war in Ukraine caused energy and food prices to rise. However, energy markets gave back some of these price gains in the final quarter of the year in response to signs of a much milder winter in Europe in addition to measures that were introduced to reduce demand, thereby keeping gas storage levels relatively high. One of the main features of 2022 was the sizeable outperformance of “value” oriented equity sectors relative to more interest rate sensitive “growth” sectors. This remained a theme over the final quarter in aggregate.

In addition to the negative impact of higher interest rates, growth stocks, particularly in the technology sector, had become increasingly expensive in terms of their valuations coming into 2022. Asian equities performed notably well in the final quarter driven by some easing of Covid control measures in China. The rebound in Asian equities late in the year was in sharp contrast to the moves seen in the preceding three quarters of the year where these assets had been one of the most severe areas of decline.

Despite a weaker finish to the year, the US dollar proved to be a bright spot for investors in 2022. It benefited from its traditional “safe haven” status in addition to the rising rate environment in the US. In contrast, Pound Sterling declined over the course of the year, alongside UK government bonds given investor risk aversion and the extreme levels of uncertainty created by the autumn mini budget proposals.

Portfolio performance

| Returns net of fees | Defensive | Moderate | Aggressive |

| October | -0.7% | 1.9% | 3% |

| November | 3.2% | 4.0% | 4.4% |

| December | -0.5% | -1.5% | -2.2% |

| Since inception (Feb 2017) | 5% | 22% | 33% |

The multi-asset portfolios produced positive absolute returns in the last quarter of 2022. In relative terms, they underperformed their respective benchmarks in Q4, but still outperformed for the full year. Major asset classes rose over the quarter despite some correction in December. Within equities, selective allocation in developed markets generated positive return.The underweight in emerging markets was closed in December as China’s relaxation of Covid-zero policy provided positive long-term catalyst.

Within fixed income, exposure to long-term treasuries hurt performance as the Fed maintained its hawkish rhetoric. Within alternatives, exposure to gold also supported performance alongside global recessionary fears.

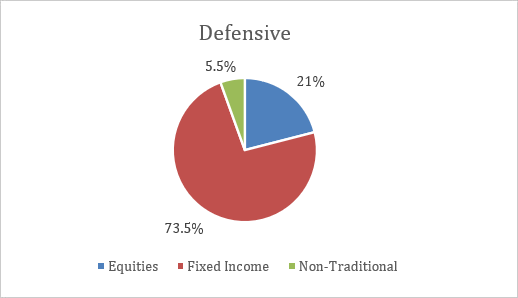

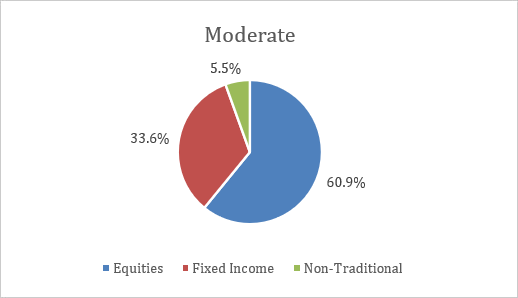

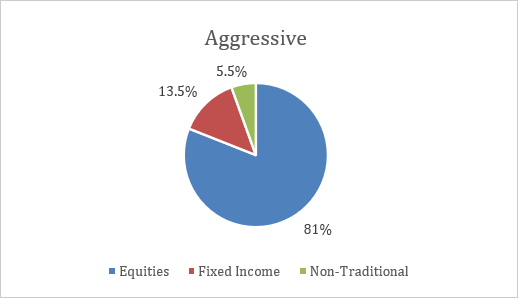

Portfolio allocation (as of 2 December 2022)