Saxo Morningstar High Dividend USD Q4 2020 commentary

| Instruments traded | Stocks |

| Asset classes | Global equities (excluding emerging markets) |

| Investment style | High quality stocks offering attractive dividends |

| Dividend Yield | 4.4% |

| Quarterly return | 15.7% (net of fees) |

| Annualised volatility (since inception) | 19.7% |

Market overview

Who would have thought we’d be here, in early 2021, with peak global COVID-19 cases, a terribly weak economy, and near-record high markets. For humanity, we are gladly waving goodbye to 2020, but for markets we have endured a period of surprising benefit. Global stocks, corporate bonds, real estate, gold, commodities, and even bitcoin have all moved forward and delivered positive performance.

In this regard, the final three months of 2020 was a strong one by historical standards—which did have some substantive developments. It is a clear case of market participants looking over the horizon, with the vaccine rollouts combining with a perception of greater political stability. The wave of “good news” comes with many fascinating and constructive sub plots. One of the most interesting happened in the fourth quarter of 2020, where small-cap value stocks bucked a multi-year trend to join the winner’s list. This was partly marked by President-elect Biden’s victory (the so-called blue wave) but is also a vision for life after lockdowns—with the reopening of the economy considered a positive for economically-sensitive and cyclical stocks. Company defaults and bankruptcies also remain low globally, defying the doomsayers, supported by record stimulus and the cheapest borrowing rates ever seen. This last point cannot be underplayed, with corporate bond spreads tightening to the lowest levels in history, perhaps reflecting expectations that a return to economic normality is still a long way off on the horizon.

Here are some of the fourth-quarter and full-year 2020 highlights:

- Global stocks rose meaningfully in the fourth quarter, finishing 2020 with healthy overall returns given the circumstances. At year-end, the U.S. market had rallied as much as 70% from March lows.

- Dividend stocks bounced back strongly in the fourth quarter but lagged the broader market for the year. Likewise, emerging-markets stocks outperformed developed markets during the fourth quarter.

- Despite a fourth-quarter rally, energy stocks were the worst-performing sector for the fourth consecutive year. At the other end, consumer cyclical and technology stocks soared.

- Small-value stocks topped the Morningstar Style Box in the fourth quarter, but value stocks still trail growth stocks by massive margins for longer time frames.

- Among fixed income, interest-rate-sensitive bonds were one of the rare assets to fall in the fourth quarter. Meanwhile, riskier high-yield and emerging-markets bond categories performed the best.

- Inflation hedges, such as inflation-protected securities and gold, all had a strong 2020 while safe-haven currencies suffered.

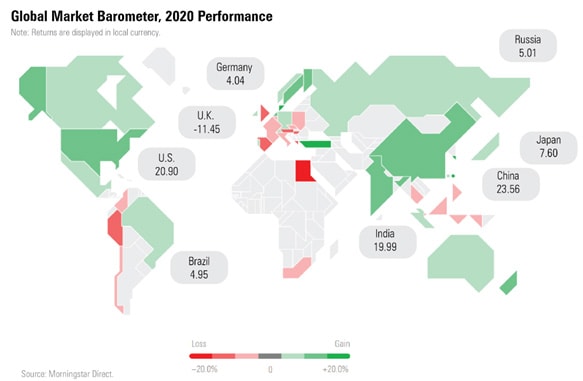

Exhibit 1: The breadth of the strong equity performance has been noteworthy, with the fourth quarter rally pulling most global markets into positive territory.

Portfolio performance (net of fees)

| Oct | -3.1% |

| Nov | 14.6% |

| Dec | 4.0% |

| 2020 | -4.5% |

| Since inception (July 2018) | 7.6% |

Top 10 portfolio holdings (as of 31/12/2020)

37.25% of total portfolio

| Name | Weight (%) |

| Broadcom Inc | 4.19 |

| Maxim Integrated Products Inc | 4.16 |

| Hubbell Inc | 3.86 |

| Commonwealth Bank of Australia | 3.71 |

| International Business Machines Corp | 3.67 |

| AT&T Inc | 3.60 |

| British American Tobacco PLC | 3.55 |

| Sanofi SA | 3.52 |

| Philip Morris International Inc | 3.51 |

| AbbVie Inc | 3.48 |

Top Performers (Below performance figures are total return Q4 USD):

Samsung Electronics Co Ltd GDR. Share price went up 44% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value.

Samsung Electronics is a diversified electronics conglomerate that manufactures and sells a wide range of products, including smartphones, semiconductor chips, printers, home appliances, medical equipment, and telecom network equipment. About 56% of its profit is generated from semiconductor business, and a further 30%-35% is generated from its mobile handset business, although these percentages vary with the fortunes of each of these businesses. It is the largest smartphone and television manufacturer in the world, which helps provide a base demand for its component businesses, such as memory chips and displays, and is also the largest manufacturer of these globally.

MPLX LP Partnership Units. Share price went up 41.9% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value.

MPLX is a partnership that owns both pipelines and gathering and processing assets with extensive holdings in the Appalachian region. The asset base is made up of pipeline assets dropped down from Marathon Petroleum, its sponsor, and gathering and processing assets from MarkWest, which it acquired in 2015. MPLX also acquired Andeavor Logistics in July 2019.

Commonwealth Bank of Australia. Share price went up 39% in Q4 and according to Morningstar proprietary analysis, the stock trades at a premium to fair value. Despite the high share price, the investment management team’s view of Commonwealth Bank of Australia is positive and this is based on the bank's robust balance sheet, dominant market positions, strong profitability, organic capital generation, sound loan book and high returns on equity.

Commonwealth Bank is Australia's second-oldest and largest bank with operations spanning Australia, New Zealand, and Asia. Its core business is the provision of retail, business, and institutional banking services. It is also a major fund manager, but a gradual exit from wealth management is ongoing. Commonwealth Bank operates the largest financial services distribution network in the country. The strategy, which has been stable and successful, emphasises a well-managed, diversified business model, strong balance sheet, stable financial platform, and conservative underwriting.

HSBC Holdings PLC. Share price went up 35% in Q4 from down 20.2% in Q3. According to Morningstar proprietary analysis, the stock trades at a discount to fair value.

London-based HSBC is one of the largest banks in the world with 40 million customers worldwide. It operates across 64 countries globally. Key regions include Asia, Europe, the Middle East and North Africa, and North America. The two largest markets for the bank are the United Kingdom and Hong Kong. The bank offers retail, commercial and institutional banking, global banking and markets, wealth management, and private banking.

ING Groep NV. Share price went up 31.6% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value.The merger of the Dutch postal bank and NN Insurance in 1991 created ING. Through a series of further acquisitions ING build up a global footprint. The 2008 financial crisis forced ING to seek government support--a precondition of which--was that ING should separate its banking and insurance activities, which saw ING revert to being solely a bank. ING has market-leading banking operations in the Netherlands and Belgium, and a range of digital banks across Europe and Australia. Its global wholesale banking operation is primarily focused on lending.

Worst Performers:

- General Mills Inc. Share price went down 3.84% in Q4 and according to Morningstar proprietary analysis, the stock trades at a premium to fair value. The investment management team’s view is that although the share is fully valued, positive momentum continues for General Mills.

General Mills is a leading global packaged food company that produces snacks, cereal, convenient meals, yogurt, dough, baking mixes and ingredients, pet food, and superpremium ice cream. Its largest brands are Nature Valley, Cheerios, Old El Paso, Yoplait, Pillsbury, Betty Crocker, Blue Buffalo, and Haagen-Dazs. In fiscal 2020, 76% of its revenue was derived from the United States, although the company also operates in Canada, Europe, Australia, Asia, and Latin America. While most of General Mills' products are sold through retail stores to consumers, the company also sells products into the food-service channel and the commercial baking industry.

- Sanofi SA. Share price went down 3.77% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value.

Sanofi develops and markets drugs with a concentration in oncology, immunology, cardiovascular disease, diabetes, and vaccines. However, the company's decision in late 2019 to pull back from the cardio-metabolic area will likely reduce the firm's footprint in this large therapeutic area. The company offers a diverse array of drugs with its highest revenue generator, Lantus, representing just under 10% of total sales. About 30% of total revenue comes from the United States and 25% from Europe. Emerging markets represent the majority of the remainder of revenue.

Among the many pivotal readouts expected across the pipeline in 2021, the baculovirus COVID-19 vaccine holds promise, with mid-stage data expected by year-end, which could support a phase 3 start.

- Intel Corp. Share price went down 3.15% in Q4. 2021 is set to be arduous for Intel as competitive threats loom amid manufacturing woes. As a result, the investment team has lowered its fair value estimate though, according to Morningstar proprietary analysis, the stock still trades at a discount to fair value.

Intel is one of the world's largest chipmakers. It designs and manufactures microprocessors for the global personal computer and data center markets. Intel pioneered the x86 architecture for microprocessors. It was the prime proponent of Moore's law for advances in semiconductor manufacturing, though the firm has recently faced manufacturing delays. While Intel's server processor business has benefited from the shift to the cloud, the firm has also been expanding into new adjacencies as the personal computer market has declined. These include areas such as the Internet of Things, memory, artificial intelligence, and automotive. Intel has been active on the merger and acquisitions front, acquiring Altera, Mobileye, Movidius, and Habana Labs in order to assist its efforts in non-PC arenas.

- Shaw Communications Inc Class B. Share price went down 2.33% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value.

Shaw Communications is a cable company in western Canada, serving as one of the biggest providers of Internet, television, and landline telephone services in British Columbia, Alberta, Saskatchewan, Manitoba, and northern Ontario. In fiscal 2019, 80% of Shaw's total revenue resulted from this wireline business. Shaw is also now a national wireless service provider after acquiring Wind Mobile in 2016. Shaw has upgraded Wind's network, undertaken an aggressive pricing strategy, and significantly enhanced its spectrum holdings. As a smaller carrier, Shaw has favored bidding status in spectrum auctions, giving it a further boost in enhancing its wireless network. At the 2019 auction, Shaw added significant amounts of 600 MHz spectrum to the 700 MHz spectrum it is currently deploying.

- Roche Holding AG. Share price went up 2.41% in Q4 and according to Morningstar proprietary analysis, the stock trades at a discount to fair value. The investment team is bullish on COVID-19 treatment REGN and thus maintaining Roche fair value estimate.

Roche is a Swiss biopharmaceutical and diagnostic company. The firm's best-selling pharmaceutical products include a variety of oncology therapies from acquired partner Genentech, and its diagnostics group was bolstered by the acquisition of Ventana in 2008. Oncology products account for 60% of pharmaceutical sales, and professional diagnostics for more than half of diagnostic-related sales.

Outlook

With the big tail risks supposedly now behind us, many households continue to invest in earnest. In this regard, we seem to live in a two-pronged household dynamic, where a meaningful portion of white-collar households are saving more than ever (due to a lack of spending), while many others are finding it very tough.

Looking to the future, investors must consider the risks they cannot see, or at least those they have not given weight to. For example, inflation and how we will ever unwind the record debt binge of 2020 could have untold consequences. Yet, above all else, investors need to weigh the valuations they are paying, as we have seen extreme divergences that presents both an opportunity and a risk.

As Warren Buffett once said, “Only when the tide goes out do you discover who's been swimming naked”. We remain confident that our positions are in the best interests of our clients—acknowledging tomorrow’s challenges and working towards a prosperous 2021 with good financial decision making.