Quarterly Outlook

Q3 Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Global Macro Strategist

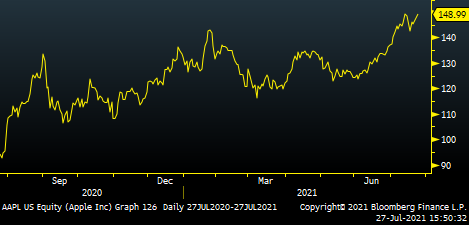

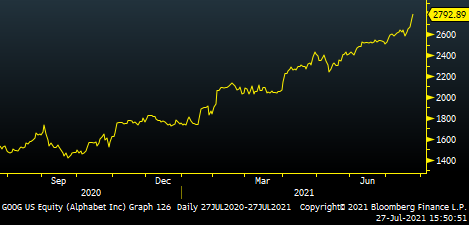

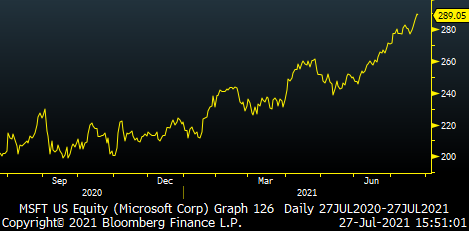

Summary: Earnings Watch aims to highlight some of the key names that are in heavy rotation on investors' & traders' radars. We check in on Apple, Microsoft & Google (Alphabet).

-

-

Who would have thought that after years of Bill Gates topping the Billionaire Charts as Numero Uno, today finds him at the #4 slot yet with an ATH of wealth of $151B. The 3-2-1 top slots go to Bernaud Arnault $175B, Elon Musk $180B, Jeff Bezos $212B.

Microsoft is one of the few companies that can boast being part of the +$2 trillion dollar club (Along with Apple) & at a fwd P/E of 35x could be considered pricey. Yet as per a quip from our equity strategist, the name was also expensive back in the 80s... so this could be an example of company where you get what you pay for.

-

Start-to-End = Gratitude + Integrity + Vision + Tenacity. Process > Outcome. Sizing > Idea.

This is the way

KVP

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy