Outrageous Predictions

A Fortune 500 company names an AI model as CEO

Charu Chanana

Chief Investment Strategist

Can AI be trusted to take over in the boardroom? With the right algorithms and balanced human oversi...

Singapore is emerging as a bright spot on the regional map as global investors look for stability and resilience. Several factors are working in its favour:

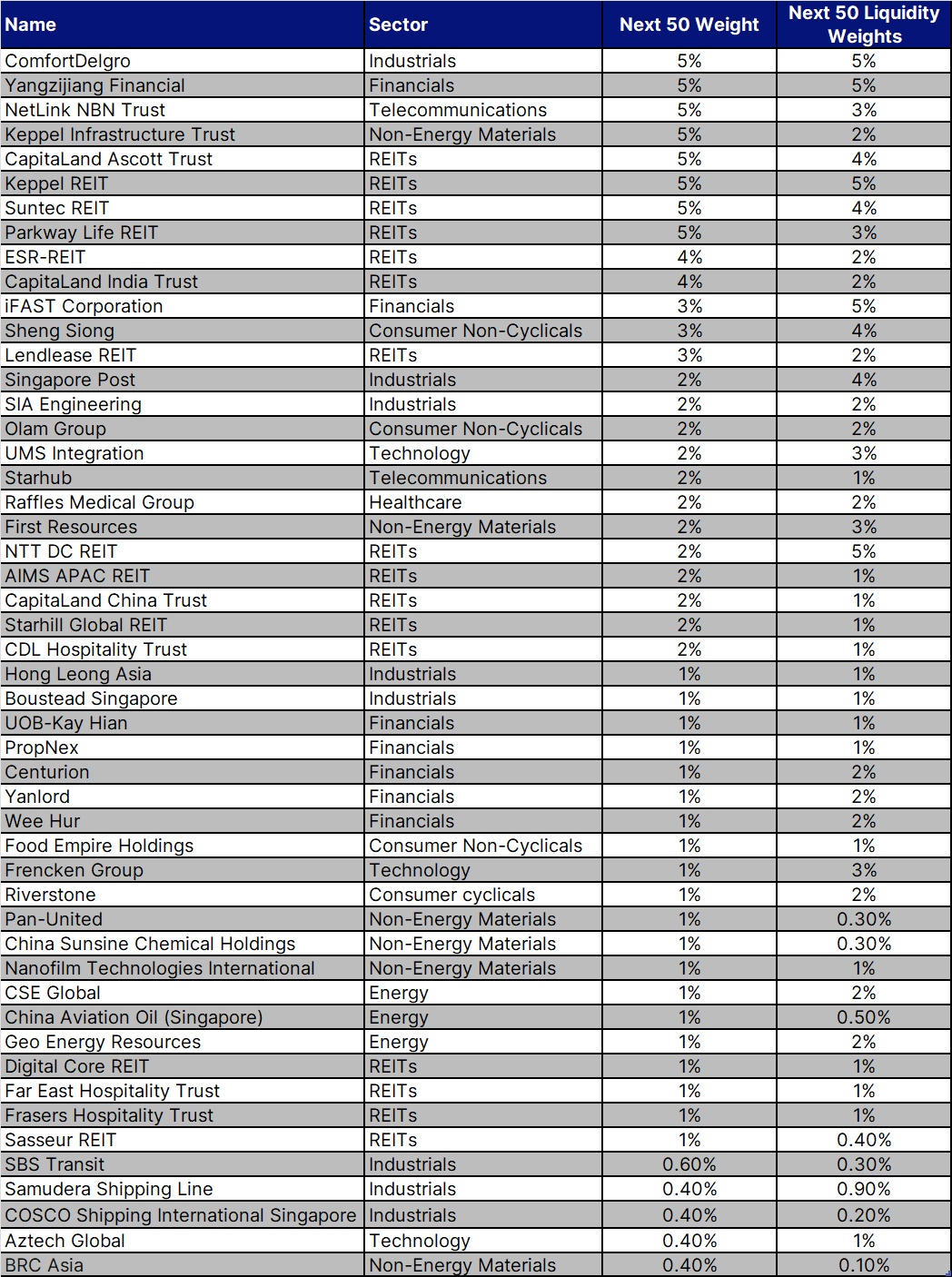

This is the context in which the iEdge Singapore Next 50 indices were launched, providing a systematic way to track mid- and large-cap names just outside the Straits Times Index (STI).

For too long, the spotlight has been on large-cap names in the STI. The Next 50 offers a systematic way to tap into mid-to large-cap names that may become tomorrow’s blue chips.

The design encourages fund managers to allocate capital beyond the same dozen or two stocks, helping deepen liquidity and attention across a wider base.

Almost half of the index by weight is allocated to REITs (≈ 45%) under the cap-weighted version, and about one-third in the liquidity version. This is a double-edged feature: REITs provide steadier cash flows, especially in a benign interest rate environment, but also may introduce correlation and sector bias.

For Saxo’s Singapore REITs stocks shortlist, click here: Singapore REITs

While the indices create opportunities, they are not without caveats:

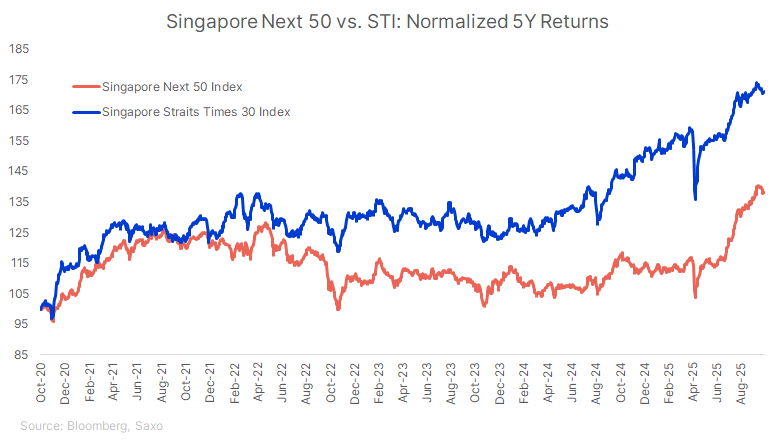

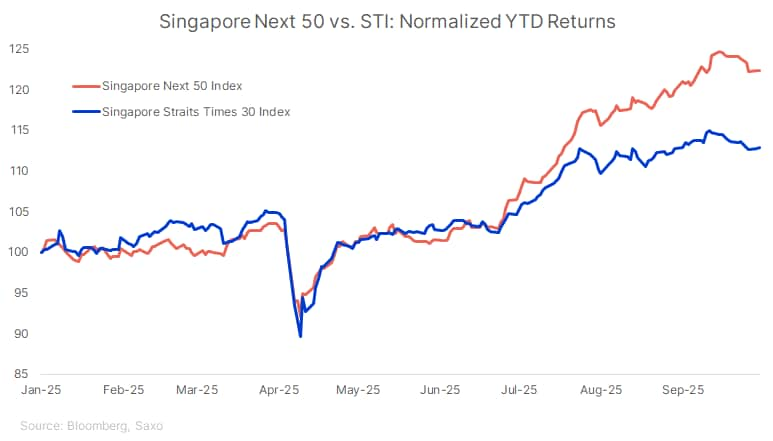

The iEdge Singapore Next 50 signals a broadening of the Singapore equity story. With performance already outpacing the STI this year and potential ETF launches on the horizon, the Next 50 could become a key barometer for Singapore’s mid-cap growth story.

It offers opportunities to look beyond the banks and telcos that dominate the STI — but risks, especially from concentration and liquidity, remain. The launch of passive products will be critical in shaping whether this index attracts wider adoption in the years ahead.

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Chief Investment Strategist