Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

Summary: Alibaba’s US-listed shares fell roughly 27% in a month, then rallied about 11% on 8 July as a DOJ settlement and a court order eased two legal overhangs. With implied volatility elevated and the August and September expiries falling on opposite sides of a catalyst cluster, this article maps a bullish call diagonal, a range-bound iron condor and a bearish put spread to that calendar, and shows why the choice of expiry does most of the work.

When two option expiries straddle the same catalysts, the expiry you choose can matter more than the direction you pick.

BABA (Alibaba Group Holding’s US-listed ADR) closed at $108.97 on 8 July 2026, up around 11% on the session (Source: Saxo platform, 8 July 2026 close). That bounce followed a bruising stretch: the shares had fallen roughly 27% over the prior month and touched a low near $94.81 on 26 June 2026 (Source: Saxo platform). Two developments drove the rebound – a $600 million non-prosecution settlement with the US Department of Justice, which turned an open-ended legal risk into a defined cost, and a California federal judge’s order temporarily suspending a Department of Defense lobbying ban tied to Alibaba’s June inclusion on the Pentagon’s “1260H” list of alleged Chinese military companies (Source: Morningstar, 6 July 2026). A trial hearing on that designation, which Alibaba denies and is contesting, is set for the week of 31 August 2026.

At-the-money implied volatility sits near 48% for both the August and September expiries, roughly two-thirds up its 52-week range (Source: Saxo option chain, 8 July 2026 close). In our view that is elevated but not extreme – enough to make premium selling defensible and naked long premium expensive. For traders weighing the setup, the question is whether the risk and reward justify a defined-risk position, and if so, which expiry to use.

That last point is the crux. Alibaba is expected to report earnings on 28 August 2026, before the market open, with the trial hearing the week after. The 21 August monthly expiry lands before both events; the 18 September monthly captures both. Two chains, similar implied volatility, but only one holds a scheduled binary event. Each structure below is chosen with that split in mind.

BABA (NYSE ADR) weekly and daily charts. The 8 July 2026 close near $109 follows a steep decline and a sharp rebound. Levels shown will differ at the time of reading. Source: SaxoTrader

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

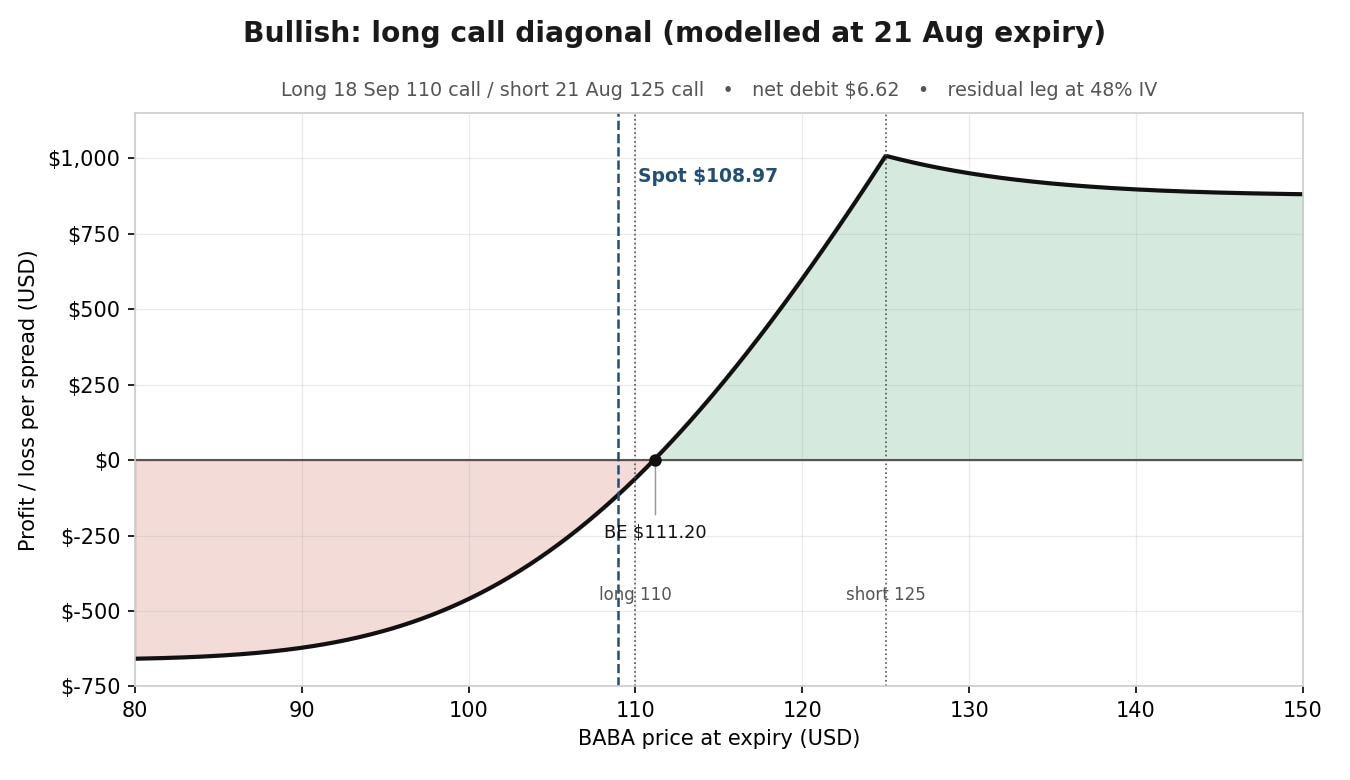

Suppose a trader thinks the legal reprieve sticks and Alibaba’s cloud and AI narrative carries the stock higher into the autumn. The reflex is to buy a call, but with implied volatility near 48% and calls bid after the pop, that is an expensive way to be right – a straight long call can still lose if the move falls short of what is already priced.

A long call diagonal expresses the same view while putting the calendar to work: it buys time where the catalysts live and sells time where they do not.

The long September 110 call carries the upside exposure and holds through both the earnings print and the trial hearing; the short August 125 call sells the eventless expiry to reduce the cost of that exposure. All strikes and premiums are illustrative and indicative only, priced from the 8 July close (Source: Saxo option chain).

Strategy insight – the calendar is doing the financing. This structure may benefit if BABA drifts higher into the August expiry, as the short front-month call decays faster than the long back-month call; the risk is that a sharp rally above $125 before 21 August brings early-assignment and capped-gain problems, with the maximum loss the debit paid plus whatever the September leg is then worth. Because one leg outlives the other, the profit and break-even are model-dependent, shifting with the September leg’s implied volatility and time value – the figures above are estimates, not fixed outcomes. The position is also net long vega: a broad drop in implied volatility could hurt the September call even if the direction is right.

Modelled profit and loss for the long call diagonal at the 21 August expiry, assuming 48% implied volatility on the residual September leg. Model-dependent. Illustrative only – not a trade recommendation. Source: Saxo

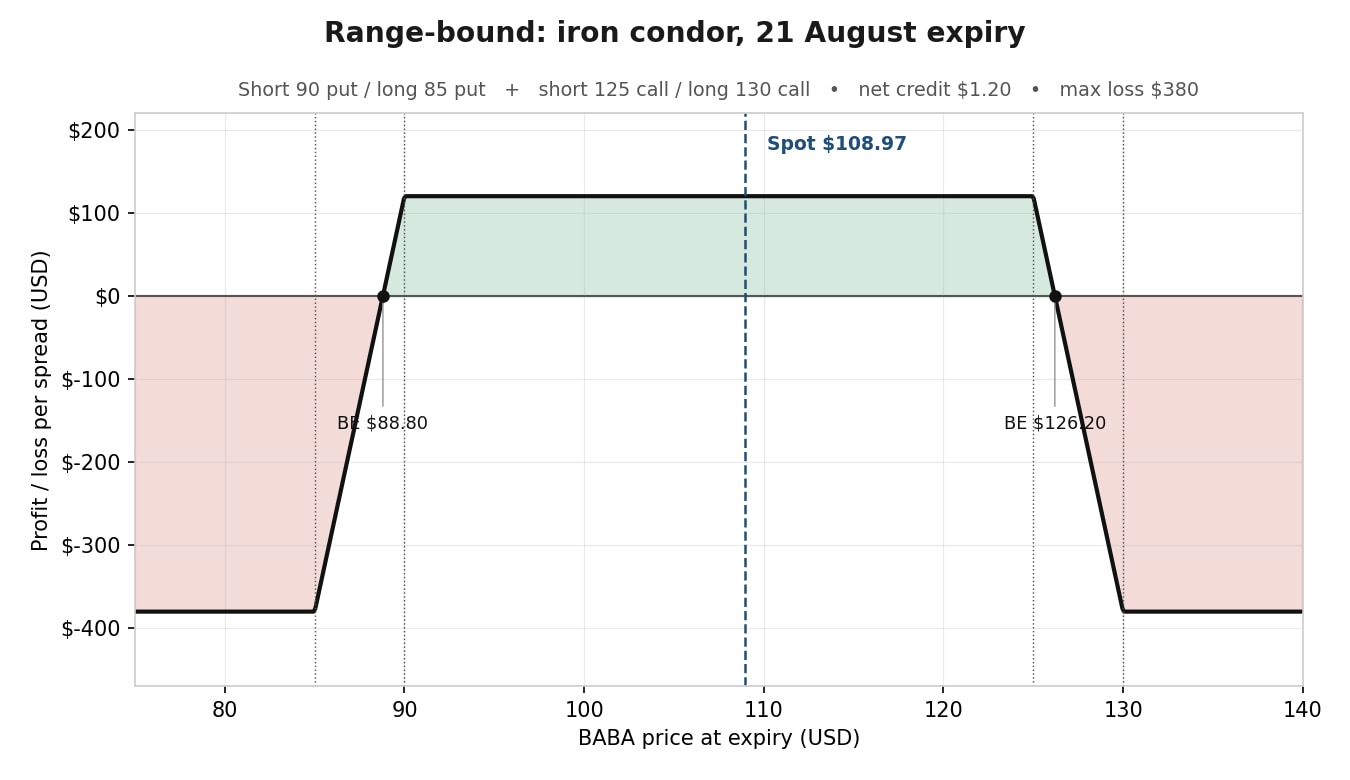

Now suppose a trader expects the noise to fade and Alibaba to consolidate through August, with no scheduled catalyst before the 21 August expiry. This is where the calendar split earns its keep: an iron condor in the August chain sells elevated premium into the one expiry that holds no earnings and no hearing.

The two short strikes define the range the trader wants Alibaba to hold, roughly $90 to $125. The two long strikes cap the damage if it does not: the maximum loss at expiry is the wing width minus the net credit, not the sum of both wings. The strikes are $5 apart because that is the listed increment near the money on this name (Source: Saxo option chain).

Strategy insight – you are selling the quiet expiry on purpose. The condor may benefit if BABA stays between the short strikes through 21 August, letting all four legs decay; the risk is that a surprise headline pushes the stock through either short strike before expiry, building the loss toward the $380 maximum. Holding the same structure in the September chain would collect more premium, but it would straddle the earnings date and the hearing – trading the range view for exposure to exactly the events this structure is built to avoid.

Iron condor profit and loss at the 21 August expiry. Maximum loss is the wing width minus the credit. Illustrative only – not a trade recommendation. Source: Saxo

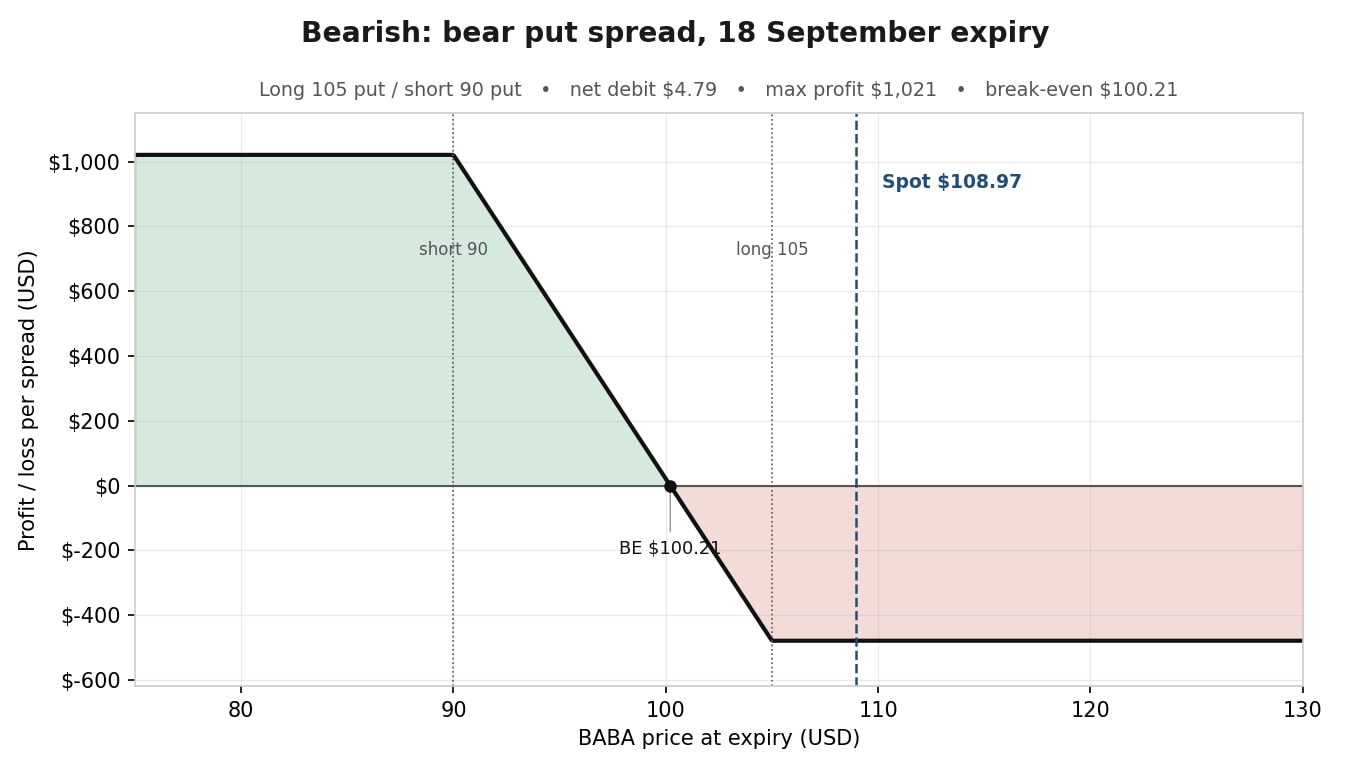

Finally, suppose a trader reads the rebound as a relief rally on a temporary reprieve, with the 1260H designation unresolved and China’s e-commerce demand soft – Daiwa cut its price target to $175 after weak “6.18” shopping-festival spending, while keeping a Buy rating (Source: Daiwa via financial media, June 2026). A retest of the late-June low near $95 is the thesis. Buying a put outright is costly with volatility this high, so a bear put spread offsets part of that cost and defines the risk, while the September expiry buys exposure across both the earnings print and the trial hearing.

The long 105 put provides the downside exposure; the short 90 put reduces the entry cost in exchange for capping the gain below $90. Traders should price the structure from the September chain directly rather than assuming the August implied move applies unchanged (Source: Saxo option chain, 8 July 2026 close).

Strategy insight – the short leg pays for conviction. The spread may benefit if Alibaba falls back toward its June low by 18 September; the risk is that the stock holds above $105, leaving the maximum loss at the $479 debit paid. Selling the 90 put is a deliberate trade-off: it lowers the cost and the break-even distance, but forfeits any gain if the sell-off runs well past $90.

Bear put spread profit and loss at the 18 September expiry, with maximum profit if BABA closes at or below $90. Illustrative only – not a trade recommendation. Source: Saxo

Assignment risk note: Because BABA options are American-style, the short legs in the condor and the short call in the diagonal can be assigned before expiry if they move into the money – particularly close to expiration or around any ex-dividend date. Traders should monitor short options and understand the platform’s assignment process before entering the trade.

See Saxo pricing for costs and applicable charges: https://www.home.saxo/rates-and-conditions/pricing-overview

Three views, three structures, one common thread: the expiry did much of the work. The diagonal borrows from the quiet August expiry to fund exposure across the September catalysts. The condor sells that same August window as its entire edge. The bear put spread reaches into September to own the events the condor avoids. Same underlying, same elevated volatility, very different trades – separated mostly by where the earnings date and the hearing fall relative to expiration.

That is the transferable lesson. When a cluster of catalysts sits between two expiries, the calendar is not a detail to settle after picking a direction; it is part of the thesis. Options let a trader express not just what they expect from Alibaba, but when – and, just as usefully, when they would rather not be exposed at all.

Nothing here is a forecast. Implied volatility can stay elevated or collapse, the earnings date may shift, and the legal picture can turn on a single ruling. Options are a framework for structuring that uncertainty with defined risk, not a way to predict the outcome. Options carry a high risk of rapid loss and are not suitable for every investor.

| More from the author |

|---|

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy