Outrageous Predictions

Switzerland's Green Revolution: CHF 30 Billion Initiative by 2050

Katrin Wagner

Head of Investment Content Switzerland

Switzerland launches a CHF 30 billion energy revolution by 2050, rivaling Lindt & Sprüngli's market ...

Key points:

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

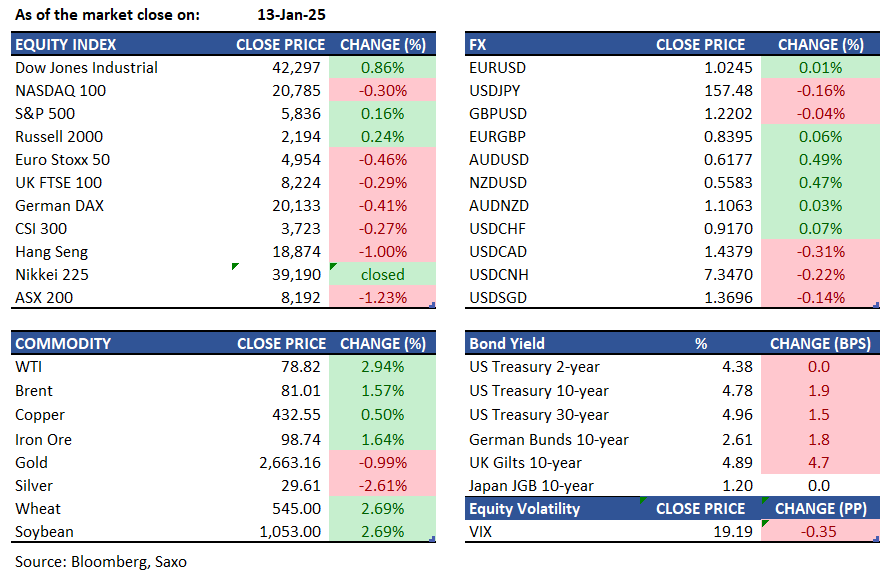

Macro:

Equities:

FX:

Commodities:

Fixed income:

For a global look at markets – go to Inspiration.

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy