Quarterly Outlook

Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Global Macro Strategist

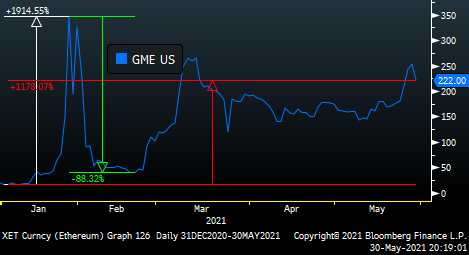

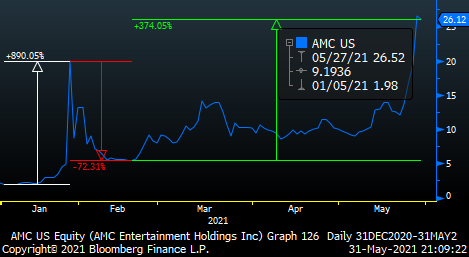

Summary: In the latest Macro Dragon Reflections think piece, KVP takes a look at the Jan-Feb short-squeeze that grew from a WSB forum on Reddit & seems to be picking up again.

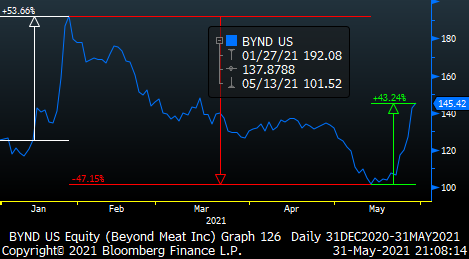

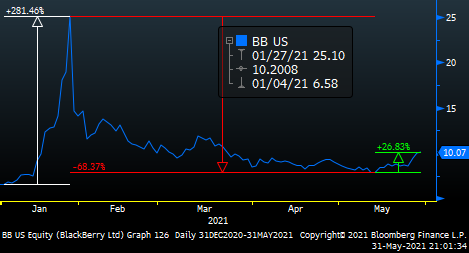

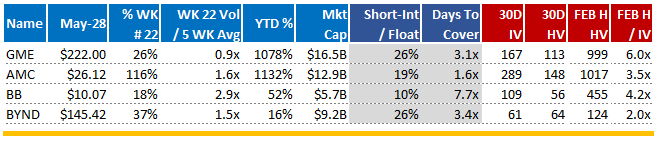

He delves into the concept of THE HIVE, whether BYND $145.42 or AMC $26.12 or BB $10.07 is the next GME $222.00, whilst comparing some of the recent moves we saw last wk with earlier in the year. AMC finished last wk up +112% (at one point it was up +200%)) & is now +1132% YTD. BYND clocked last wk at +37%, with GME & BB at the back with +26% & +18%.

1. BYND could potentially become a HIVE stock [what PM wants to walk into the CIO room & explain a short squeeze post what happened to Melvin], was never part of the original thesis… but cult stock like tesla or tencent was always the potential icing on the cake.

2. At $145 BYND is c. -40% from its ATH of c. $240 which it hit in the summer of 2019. Earlier this year during the WSB|RB Squeeze it got to $221 by the end of Jan, finding a 3wk run of +51% (so far we are on a 2wk run of +38% - yet worth noting growth has been killed over last few wks, so likely also a mean-reversion element on growth > value performance wise)

3. According to Bloomberg there is a 26% short interest on its float (which granted is c. 3.4x days to cover).

4. They continue to make JV & new partnerships, from Pepsi to inroads in China, etc.

5. Oatley [OTLY] another sustainable alternative play - focused on alternative dairy - recently listed & has a market cap of $14bn, is a much older company & clocked +$420m in rev in 2020 (granted +100% growth) – main point here is not substitution, but the investment theme is growing which will continue to attract a narrative & story, which leads to further capital from investors.

-

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP

Q3 Macro Outlook: Less chaos, and hopefully a bit more clarity

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy